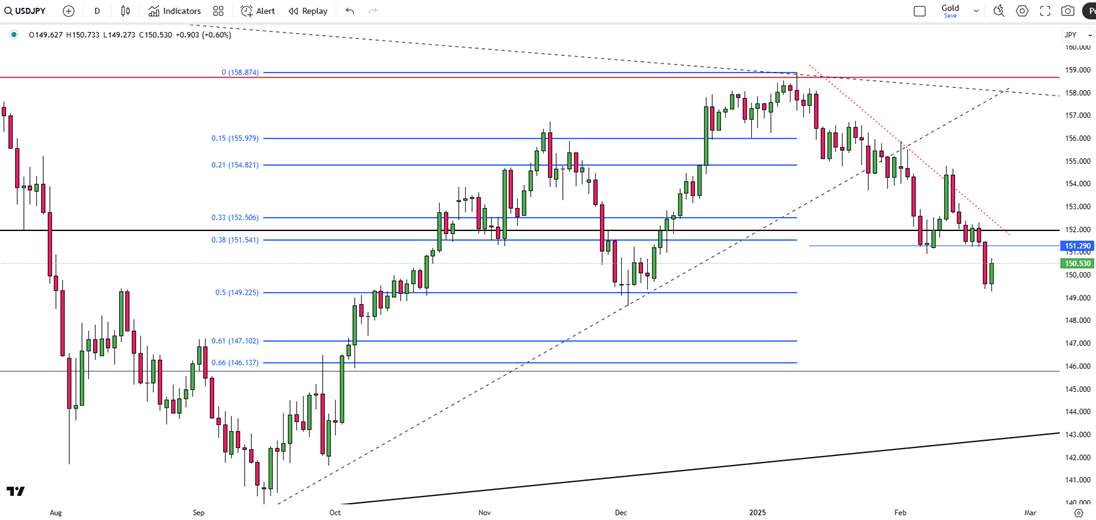

The euro held steady near 1.0500 ahead of key PMI data, while the yen weakened past 150 despite rising inflation and BOJ’s hawkish stance.

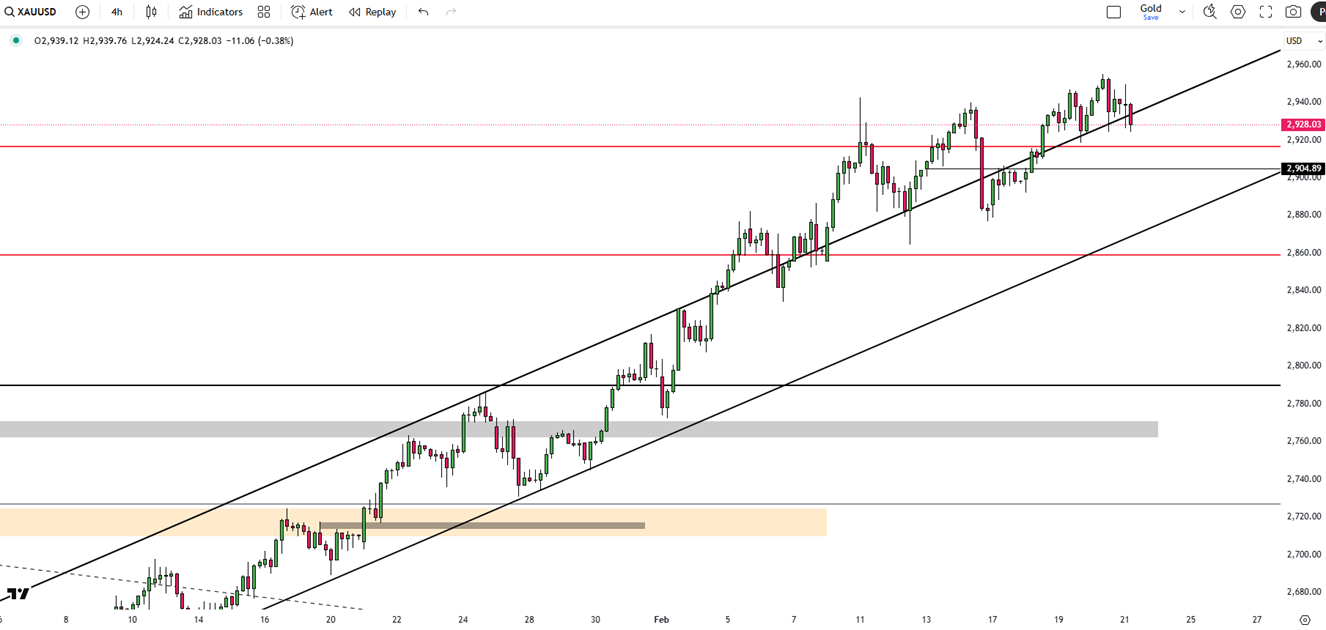

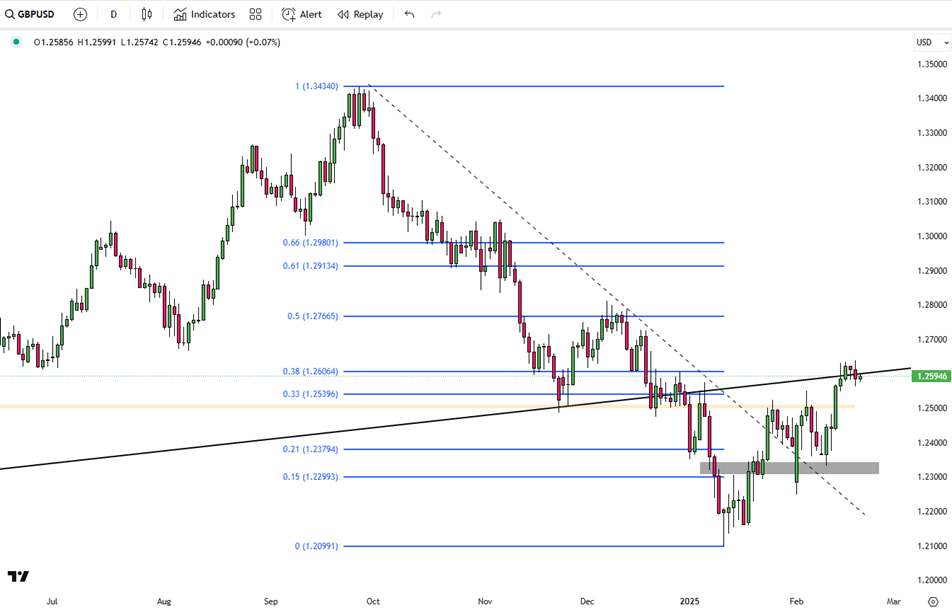

Gold stayed near record highs as trade war fears and geopolitical tensions supported safe-haven demand. The British pound remained firm above 1.2600, driven by expectations of strong UK retail sales. Silver rebounded toward $33 per ounce as markets assessed Fed policy and escalating trade risks.

| Time | Cur. | Event | Forecast | Previous |

| 10:00 | GBP | Core Retail Sales (YoY) (Jan) | 0.5% | 2.9% |

| 10:00 | GBP | Retail Sales (MoM) (Jan) | 0.4% | -0.3% |

| 12:30 | GBP | Composite PMI (Feb) | 50.5 | 50.6 |

| 12:30 | GBP | Manufacturing PMI (Feb) | 48.5 | 48.3 |

| 12:30 | GBP | Services PMI (Feb) | 50.8 | 50.8 |

| 17:45 | USD | US Manufacturing PMI (Feb) | 51.3 | 51.2 |

| 17:45 | USD | US Services PMI (Feb) | 53.0 | 52.9 |

| 18:00 | USD | US Existing Home Sales (Jan) | 4.12M | 4.24M |

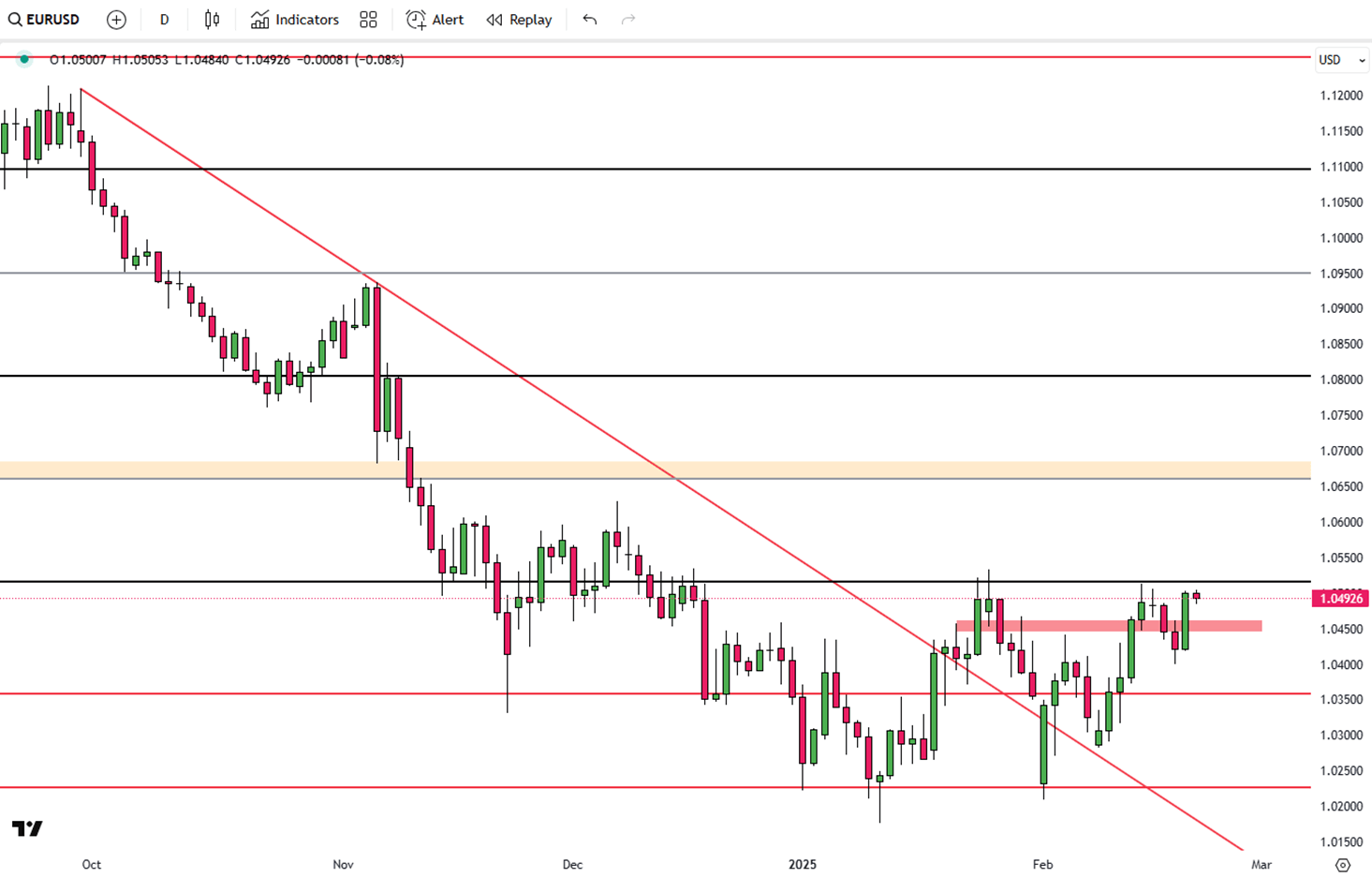

EUR/USD remains steady near 1.0500 in late US trading on Thursday, though Trump's tariff threats could pressure the Euro. Markets now focus on Friday’s advanced HCOB Manufacturing and Services PMIs for Germany and the Eurozone.

US jobless claims for the week ending February 15 rose to 219K, slightly above the expected 215K but unlikely to impact the Fed’s policy stance. Meanwhile, Trump announced new tariffs set to take effect within a month, expanding duties to include cars, semiconductors, pharmaceuticals, lumber, and forest products, raising trade concerns that may weigh on the Euro.

Expectations of ECB rate cuts also add downside pressure, with analysts predicting 25 basis point reductions at each meeting until mid-2025, potentially lowering the deposit rate to 2.0%.

Key resistance is at 1.0515, followed by 1.0600 and 1.0650. Support stands at 1.0350, with further levels at 1.0275 and 1.0220.

| R1: 1.0515 | S1: 1.0350 |

| R2: 1.0600 | S2: 1.0275 |

| R3: 1.0650 | S3: 1.0220 |

The Japanese yen weakened past 150 per dollar on Friday, pulling back from 11-week highs despite inflation data supporting a hawkish BOJ stance. Core inflation rose to 3.2% in January from 3%, exceeding forecasts, while headline inflation jumped to 4%, the highest in two years. BOJ Governor Kazuo Ueda stated that rising interest rates could benefit financial institutions long-term and reaffirmed the central bank’s readiness to act if markets become volatile. BOJ board member Takata also hinted at potential policy adjustments if economic conditions evolve as expected.

Key resistance is at 154.90, with further levels at 156.00 and 157.00. Support stands at 149.20, followed by 147.10 and 145.80.

| R1: 154.90 | S1: 149.20 |

| R2: 156.00 | S2: 147.10 |

| R3: 157.00 | S3: 145.80 |

Gold hovered near $2,940 per ounce, close to its record high of $2,950, and was set for an eighth weekly gain as global uncertainties fueled safe-haven demand. President Trump’s new tariffs on lumber, cars, semiconductors, and pharmaceuticals escalated trade tensions, while reports suggested he may withdraw US support for Ukraine in talks with Russia, raising geopolitical risks. US Treasury Secretary Scott Bessent dismissed speculation about revaluing bullion reserves, and Swiss customs data revealed gold exports to the US hit a 13-year high in January.

Key resistance stands at $2,949, with further levels at $2,975 and $3,000. Support is at $2,880, followed by $2,830 and $2,760.

| R1: 2949 | S1: 2880 |

| R2: 2975 | S2: 2830 |

| R3: 3000 | S3: 2760 |

The British Pound (GBP) strengthens against the US Dollar (USD), surpassing the 1.2600 mark on Thursday, as traders look ahead to the upcoming UK Retail Sales data. At the same time, a weaker US jobs report puts pressure on the US Dollar.

The first resistance level for the pair will be 1.2670. In the event of this level's breach, the next levels to watch would be 1.2720 and 1.2766. On the downside 1.2340 will be the first support level. 1.2265 and 1.2100 are the next levels to monitor if the first support level is breached.

| R1: 1.2670 | S1: 1.2340 |

| R2: 1.2720 | S2: 1.2265 |

| R3: 1.2766 | S3: 1.2100 |

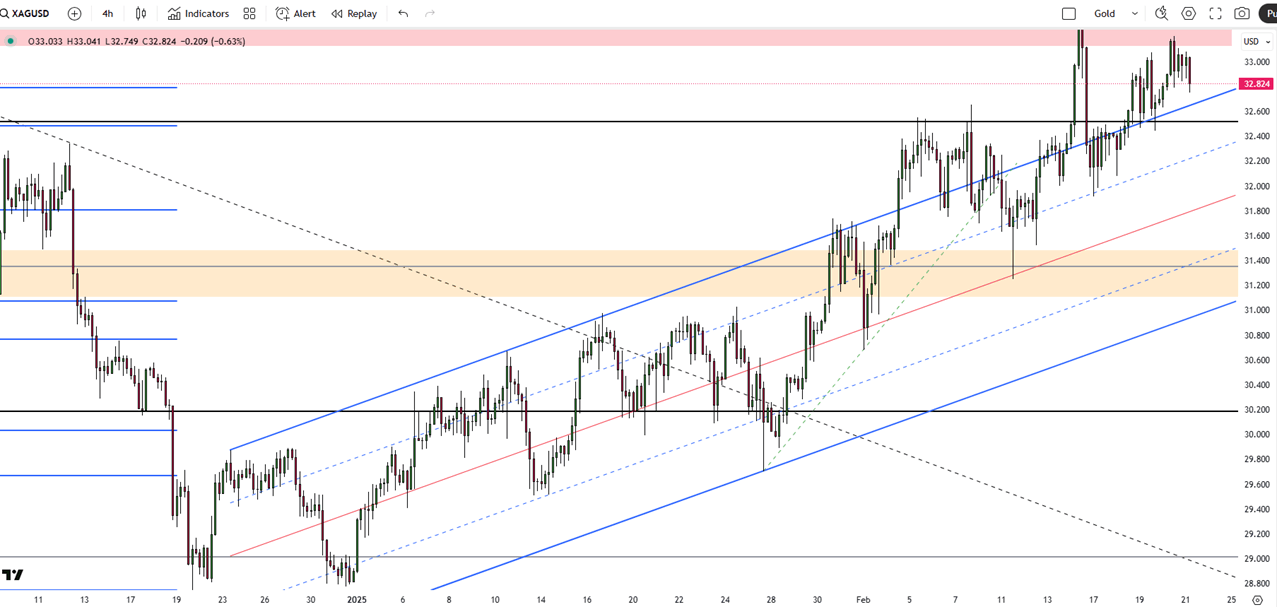

Silver climbed toward $33 per ounce on Thursday, rebounding from the previous session’s losses as trade and geopolitical risks fueled safe-haven demand. President Trump’s plan for 25% tariffs on automobiles, semiconductors, and pharmaceuticals reignited trade war fears, while his remarks calling Ukraine’s President Zelenskiy a dictator added to market uncertainty amid ongoing peace talks with Russia. Meanwhile, Fed officials signaled in January that more inflation progress is needed before considering rate cuts, with concerns over the economic impact of new tariffs.

Key resistance stands at 33.15, with further levels at 33.80 and 34.50. Support is at 31.40, followed by 30.90 and 30.20.

| R1: 33.15 | S1: 31.40 |

| R2: 33.80 | S2: 30.90 |

| R3: 34.50 | S3: 30.20 |

After Khamenei: Who Will Lead Iran Next?

After Khamenei: Who Will Lead Iran Next?Following the death of Supreme Leader Ali Khamenei, Iran has entered a pivotal transition phase. Senior officials in Tehran are acting swiftly to uphold the existing structure of the Islamic Republic, prioritizing continuity to head off potential internal instability. Despite these efforts, the sudden leadership vacuum has sparked intense political and military maneuvering behind the scenes.

Detail") March Starts With Geopolitical Turmoil (2-6 March)

March Starts With Geopolitical Turmoil (2-6 March)Global markets began the week in a state of high alert following coordinated US and Israeli strikes on Iran over the weekend, which resulted in the death of Supreme Leader Ayatollah Ali Khamenei.

Detail Geopolitical Shock Triggers Risk-Off Move (03.02.2026)President Trump stated that operations against Iran could last up to four weeks, though he added that developments are proceeding as planned and could wrap up sooner.

Then Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!