The US dollar strengthened against the euro as the US economy outperformed, leading to fewer expected Fed rate cuts.

The yen weakened despite intervention, while gold held steady amid geopolitical tensions and central bank demand. The GBP/USD pair fell sharply due to risk-off sentiment and fewer expected US rate cuts. Silver benefited from a pause in rising bond yields.

| Time | Cur. | Event | Forecast | Previous |

| 15:00 | USD | ISM Manufacturing Employment (Dec) | | 48.1 |

| 15:00 | USD | ISM Manufacturing PMI (Dec) | 48.3 | 48.4 |

| 15:00 | USD | ISM Manufacturing Prices (Dec) | 52 | 50.3 |

| 16:00 | EUR | ECB's Lane Speaks | | |

| 18:00 | USD | Atlanta Fed GDPNow (Q4) | 2.60% | 2.60% |

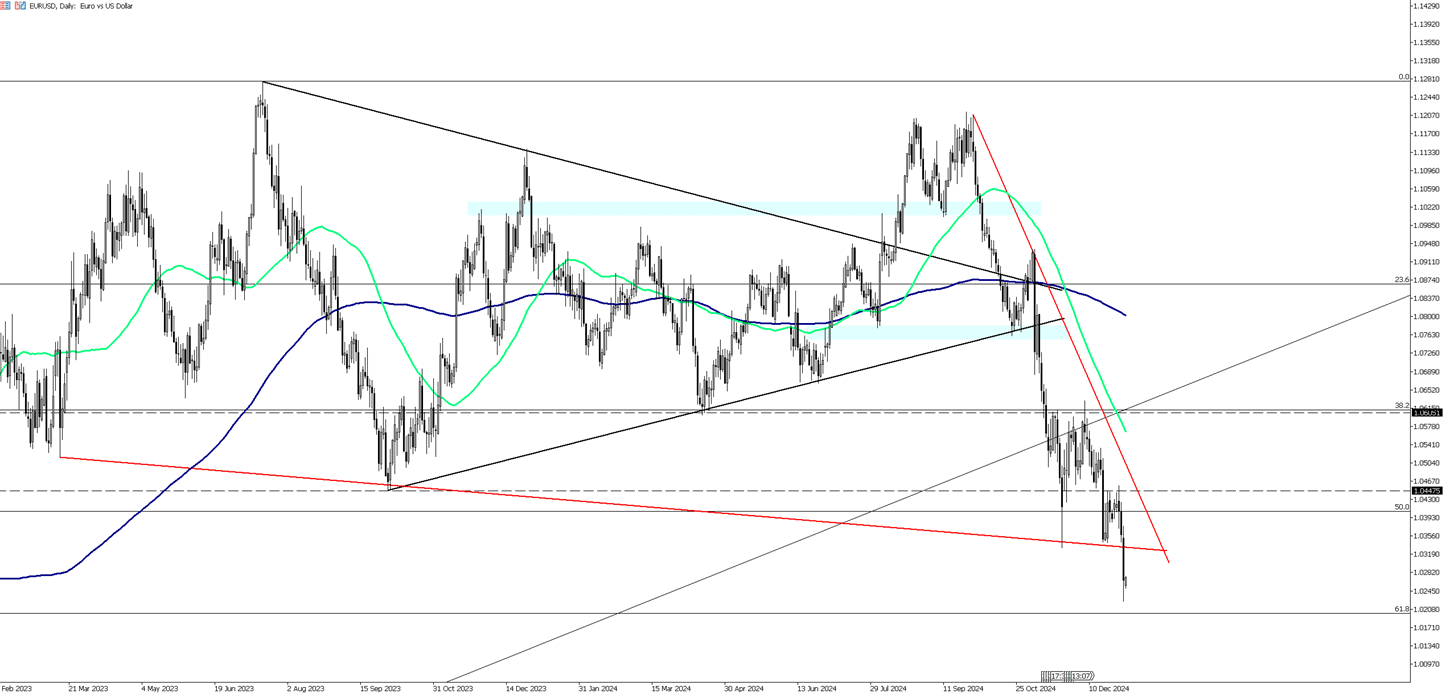

The EUR/USD pair is trading at around 1.0237 on Friday morning. The dollar index remains above 109, holding near its highest levels in two years, as investors bet on the strength of the U.S. economy and fewer rate cuts from the Federal Reserve this year. The U.S. economy continues to show resilience, positioning it to outperform other global economies in the short term.

The Fed has indicated a more cautious approach to policy easing in 2025 due to ongoing inflation concerns. Current projections suggest only two quarter-point rate cuts this year, significantly lower than the 100 basis points expected in September. Additionally, uncertainties surrounding the incoming Trump administration made investors look forward to Friday’s ISM Manufacturing Index and comments from Fed officials for further economic insights.

From a technical perspective, the first resistance level is at 1.0360, with further resistance levels at 1.0460 and 1.0520 if the price breaks above. On the downside, the initial support is at 1.0250, followed by additional support levels at 1.0220 and 1.0150.

| R1: 1.0360 | S1: 1.0250 |

| R2: 1.0460 | S2: 1.0220 |

| R3: 1.0520 | S3: 1.0150 |

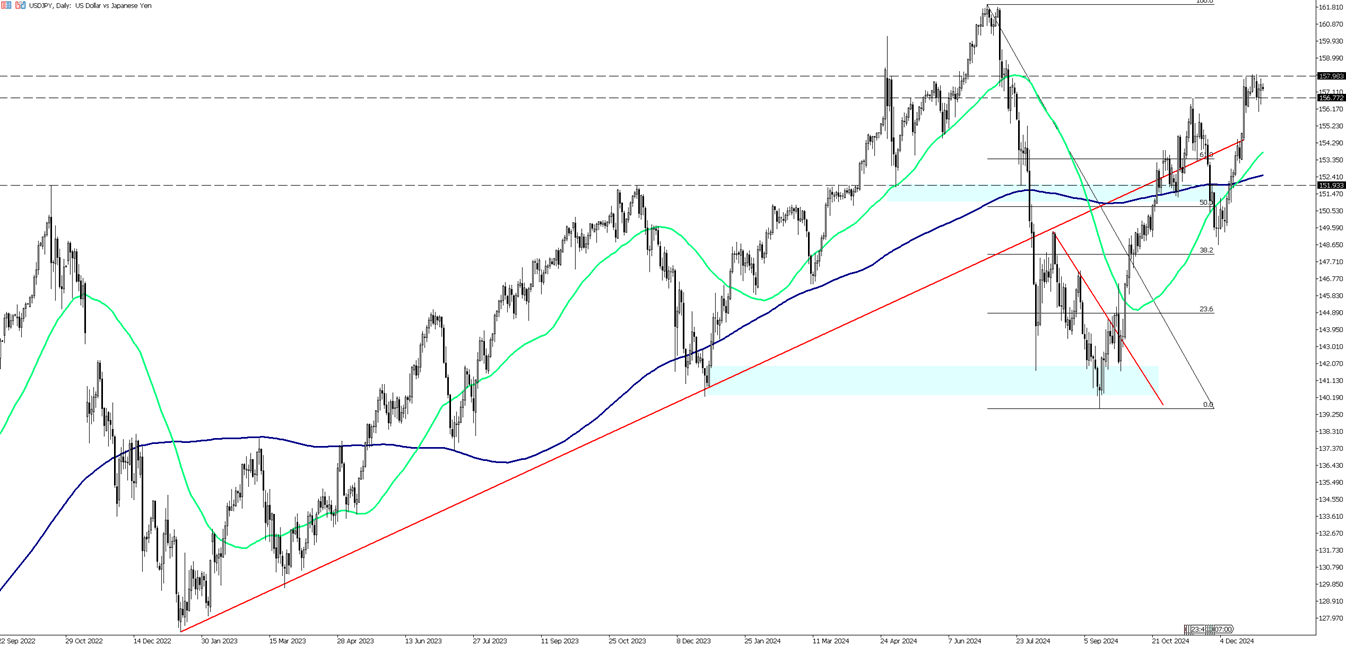

The USD/JPY pair traded lower, near 157.30, during Friday’s Asian session. Japanese officials' verbal intervention supported the Japanese yen (JPY). However, uncertainty surrounding the Bank of Japan's (BoJ) policy outlook could limit further gains for the JPY. Japanese markets are closed for the rest of the week, and traders are preparing for the release of the US ISM Manufacturing PMI for December later on Friday.

Last week, Japan's Finance Minister, Katsunobu Kato, reiterated concerns about the weakening yen, warning that appropriate measures would be taken to address excessive currency fluctuations. For the coming week, the BoJ will release its quarterly report on regional economic conditions, which is expected to provide an update on whether wage increases are becoming more widespread across Japan. This report could offer valuable insights ahead of the BoJ’s policy meeting on January 24.

Meanwhile, speculation that the Federal Reserve will cut interest rates more cautiously in 2025, coupled with optimism about the US economy, could support the US dollar (USD). The Fed has signaled a more measured approach to rate reductions as inflation remains above its 2% target, and the economy remains strong. Additionally, the policies of Trump are expected to stimulate growth and potentially drive inflation, which could slow the pace of future rate cuts by the Fed.

The key resistance level appears to be 158.30, with a break above it potentially targeting 160.00 and 161.00. On the downside, 154.90 is the first major support, followed by 153.40 and 152.40 if the price moves lower.

| R1: 158.30 | S1: 154.90 |

| R2: 160.00 | S2: 153.40 |

| R3: 161.00 | S3: 152.40 |

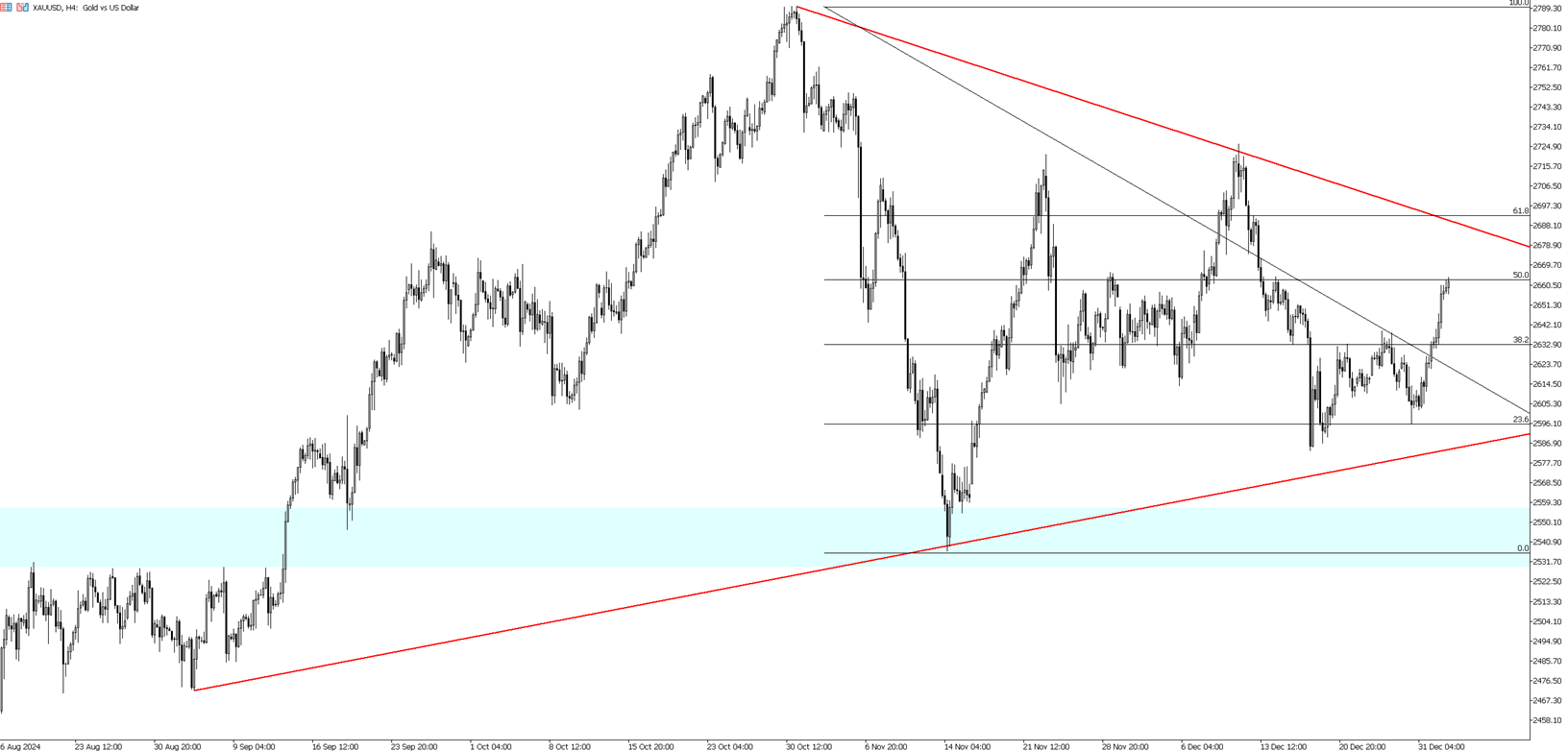

Gold held steady around $2,660 per ounce on Friday, set to finish the week with gains, driven by safe-haven demand and expectations for ongoing central bank gold purchases. Geopolitical tensions continued to support the yellow metal, especially after Russia's drone strike on Kyiv and Israel's airstrike on Gaza City. A recent World Gold Council survey also indicated that major central banks are likely to increase gold purchases in the coming year.

On the economic front, U.S. jobless claims fell to an eight-month low in the last week of 2024, reflecting the strength of the labor market. The Federal Reserve's cautious stance on rate cuts, due to the strong economy and job market, has reduced the appeal of non-yielding gold. Meanwhile, investors continue to evaluate the potential impact of a second Trump presidency and China's efforts to stimulate growth.

Technically, the first resistance level will be 2665 level. In case of this level’s breach, the next levels to watch would be 2695 and 2725. On the downside 2640 will be the first support level. 2605 and 2575 are the next levels to monitor if the first support level is breached.

| R1: 2665 | S1: 2640 |

| R2: 2695 | S2: 2605 |

| R3: 2725 | S3: 2575 |

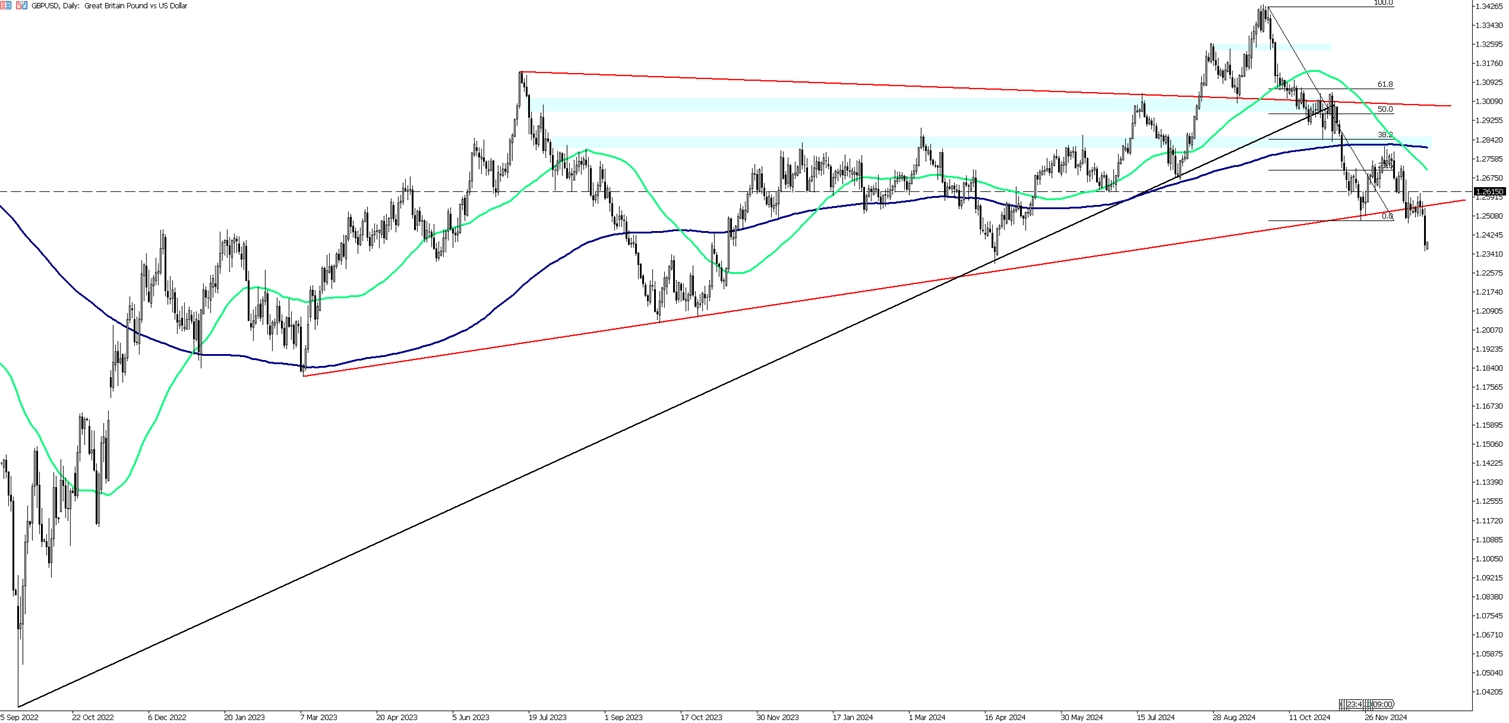

GBP/USD is trading around 1.2390, dropping over 1% at the start of the new trading season and breaking below the 1.2400 level for the first time in nearly ten months. Market volumes remain low following the midweek New Year's holiday, with prevailing sentiment leaning towards a risk-off stance. Economic data from the UK is light for the rest of the first week of 2025, leaving traders focused on the upcoming US Purchasing Managers Index (PMI) figures set to be released on Friday. Also scheduled for release are the UK Money Supply and Mortgage Approvals data, though these low-impact figures are unlikely to significantly move the markets.

The US ISM Manufacturing PMI for December is expected to show a slight decline, printing at 48.4, matching the preliminary reading. Although there is a minor uptick from the previous month, US businesses still hold a cautious outlook for the first quarter of 2025 as domestic demand weakens.

For GBP/USD traders, the key focus will be the interest rate differential for the first half of 2025. The Federal Reserve is now expected to implement fewer rate cuts than originally anticipated, with the central bank projecting only two 25-basis-point cuts throughout the year, as outlined in its December Summary of Economic Projections (SEP).

The first resistance level for the pair will be 1.2480. In case of this level's breach, the next levels to watch would be 1.2570 and 1.2600. On the downside 1.2350 will be the first support level. 1.2300 and 1.2265 are the next levels to monitor if the first support level is breached.

| R1: 1.2480 | S1: 1.2350 |

| R2: 1.2570 | S2: 1.2300 |

| R3: 1.2600 | S3: 1.2265 |

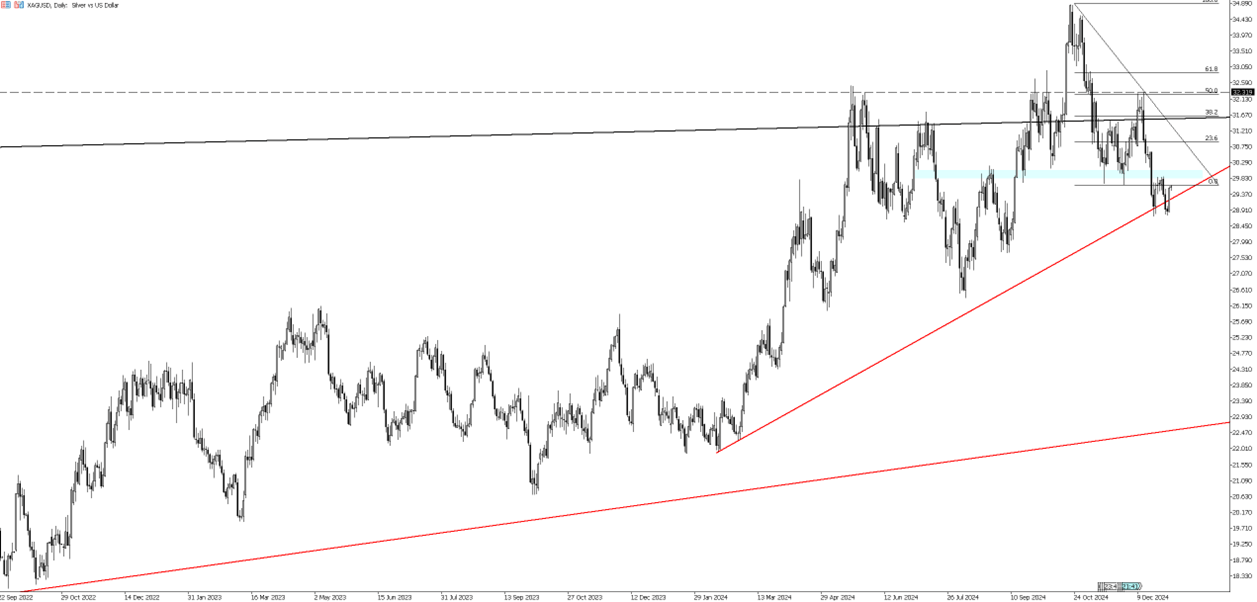

Silver is trading around $29.60, benefiting from a pause in the rally of US bond yields, which had surged more than 10% over the past month. The 10-year US Treasury yields have now dropped to approximately 4.55%. Lower bond yields reduce the opportunity cost of holding non-yielding assets like silver, making it more attractive.

The outlook for the US Dollar and bond yields is expected to remain strong as the Federal Reserve (Fed) is likely to implement fewer interest rate cuts this year, given officials' positive view on the economy. Market sentiment is also buoyed by expectations of stronger US economic growth under President-elect Donald Trump’s administration, with policies such as stricter immigration controls, higher import tariffs, and tax cuts potentially boosting economic activity.

Goldman Sachs analysts predict the Fed will make its next rate cut in March, with two additional cuts expected in June and September, bringing borrowing rates to the 3.50%-3.75% range. In 2024, the Fed had already lowered rates three times by a total of 100 basis points, bringing them to 4.25%-4.50%.

Technically, the first resistance level will be 29.85 level. In case of this level’s breach, the next levels to watch would be 30.20 and 30.70 consequently. On the downside 28.50 will be the first support level. 28.00 and 27.50 are the next levels to monitor if the first support level is breached.

| R1: 29.85 | S1: 28.50 |

| R2: 30.20 | S2: 28.00 |

| R3: 30.70 | S3: 27.50 |

Trump Signals Extended Military Campaign

Trump Signals Extended Military CampaignGeopolitical tensions in the Middle East have intensified following recent remarks from Donald Trump suggesting that the ongoing military campaign against Iran may last longer than anticipated. While Trump stated that early operational objectives were achieved ahead of schedule, he acknowledged that broader strategic goals could require additional time and sustained military pressure.

Detail US DST Change March 8 2026

US DST Change March 8 2026Daylight Saving Time will change in the United States on Sunday, March 8, 2026. The trading schedule for various financial instruments will be adjusted to align with U.S. exchange hours.

Detail Dollar Leads Risk-Off (03.06.2026)Global markets remained under pressure as escalating Middle East tensions and rising energy prices strengthened the US dollar and unsettled major currencies.

Then Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!