The U.S. dollar gained traction Monday after the U.S. and China agreed to pause retaliatory tariffs for 90 days, prompting a gap lower in EUR/USD to 1.1064. Meanwhile, Moody’s downgraded the U.S. credit rating, citing fiscal concerns, sparking risk aversion and supporting safe-haven assets like gold and the yen.

Gold rebounded to $3,220, while silver hovered near $32.30. The pound climbed toward 1.3300 on weak U.S. data and firm UK GDP. Equities showed mixed sentiment amid policy and geopolitical uncertainty.

| Time | Cur. | Event | Forecast | Previous |

| 09:00 | EUR | CPI (YoY) (Apr) | 2.2% | 2.2% |

| 12:30 | USD | FED Bostic Speech |

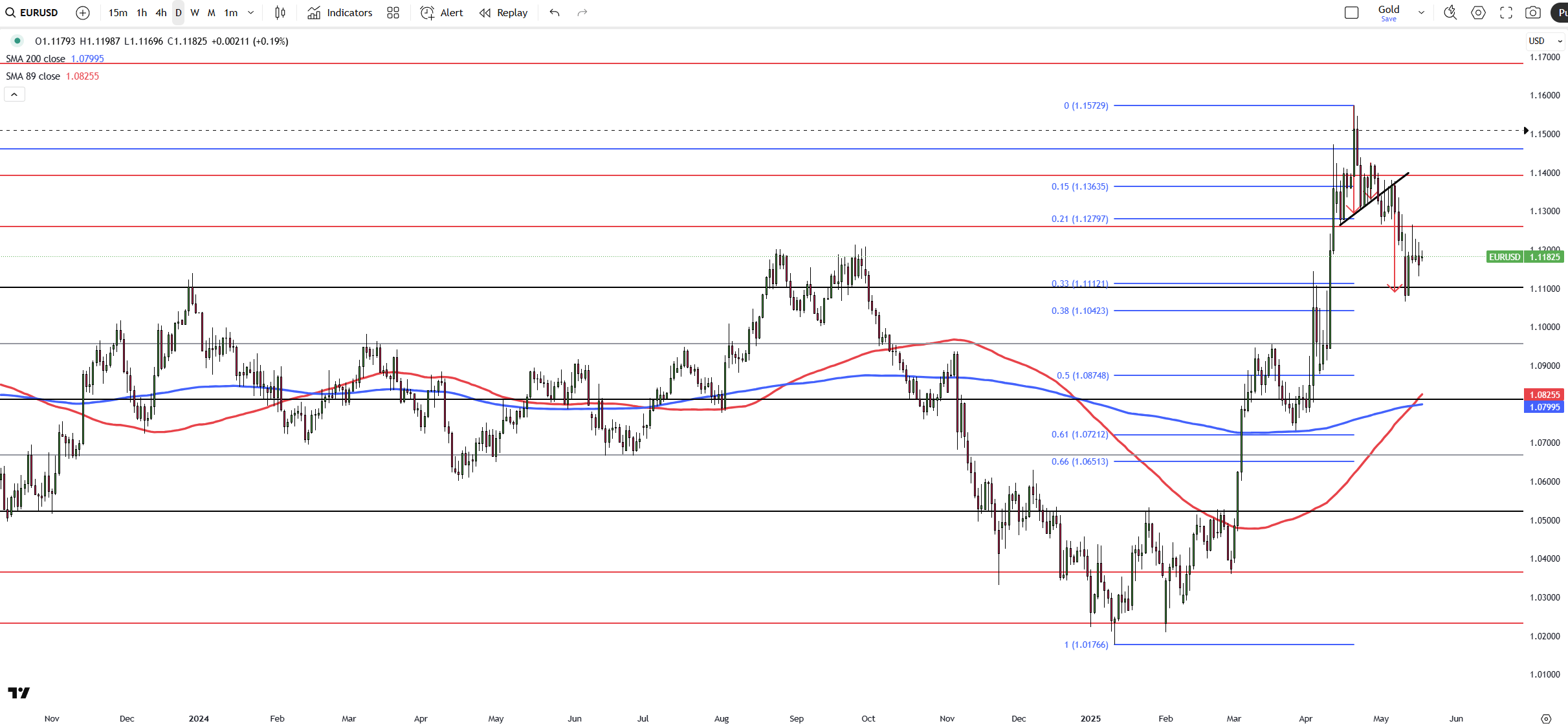

The EUR/USD pair started the week with a downside gap, falling to 1.1064 on Monday as the U.S. dollar gained strength. The move followed easing trade tensions between the U.S. and China, after weekend talks resulted in a joint agreement to pause retaliatory tariffs for 90 days. The U.S. committed to cutting additional tariffs on Chinese goods from 145% to 30%, while China agreed to reduce its tariffs on American imports from 125% to 10%.

The key resistance is located at 1.1260 and the first support stands at 1.1040.

| R1: 1.1260 | S1: 1.1040 |

| R2: 1.1460 | S2: 1.1000 |

| R3: 1.1580 | S3: 1.0960 |

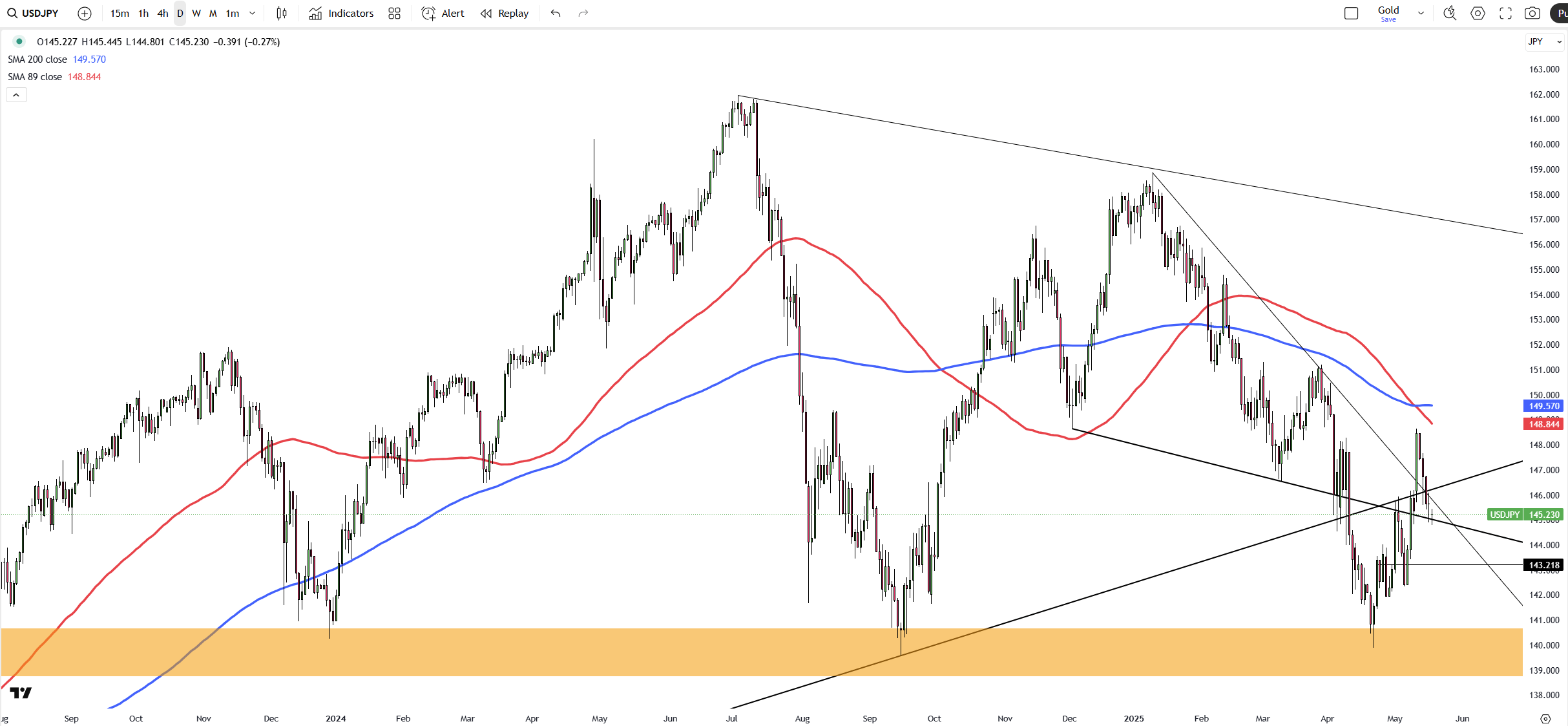

USD/JPY declined to around 144.80 on Monday, hitting its lowest level in over a week amid renewed selling pressure during Asian trading. The pair extended last week’s pullback from a nearly six-week high, driven by firm expectations that the Bank of Japan may raise interest rates again in 2025. Additionally, Moody’s unexpected downgrade of the U.S. sovereign credit rating to "Aa1" from "Aaa" heightened market caution. The agency cited growing national debt as the key concern, prompting risk aversion and supporting the safe-haven Japanese yen.

The key resistance is at $148.60 meanwhile the major support is located at $139.70.

| R1: 148.60 | S1: 139.70 |

| R2: 149.80 | S2: 137.00 |

| R3: 151.20 | S3: 135.00 |

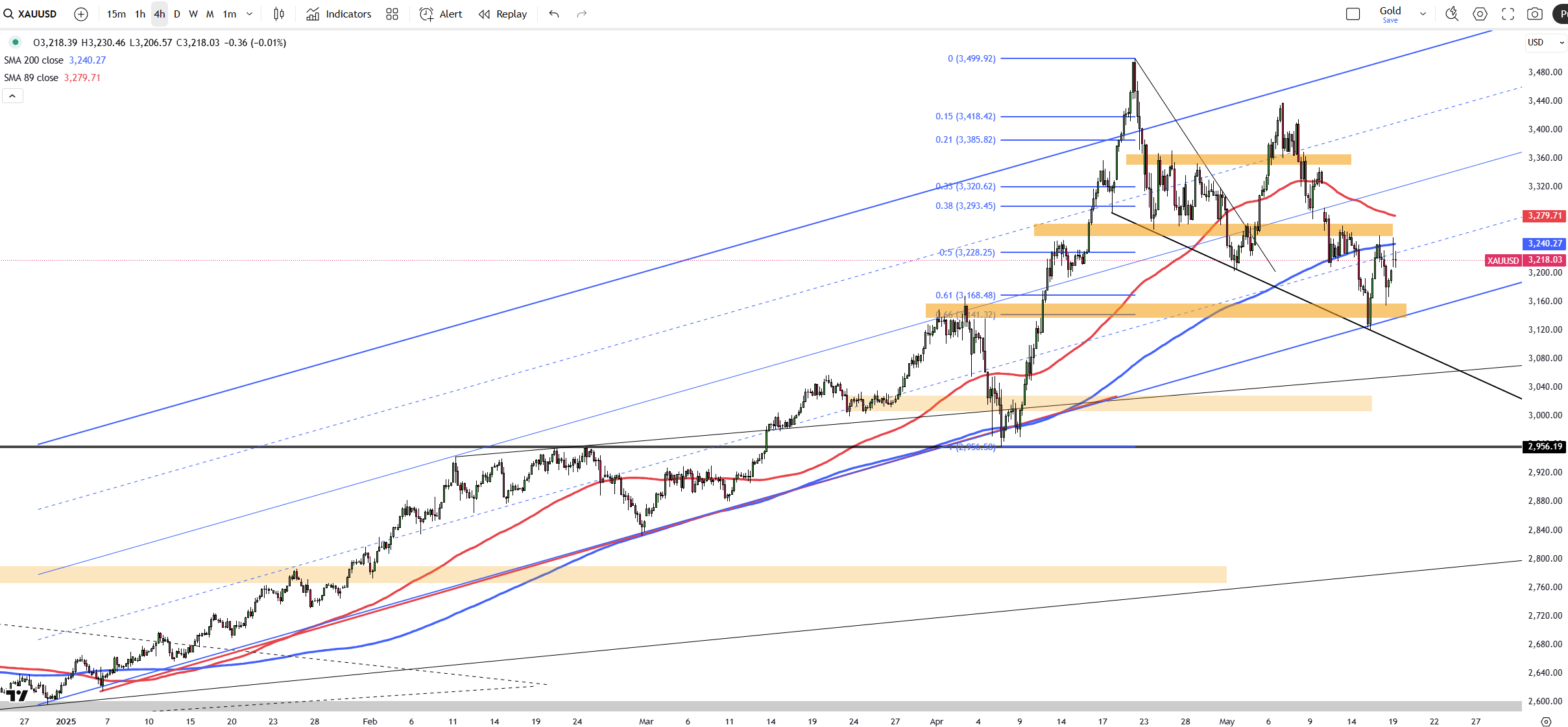

Gold rose above $3,220 per ounce on Monday, recovering from its steepest weekly decline in six months, as safe-haven demand picked up amid growing concerns about the U.S. economy and fiscal outlook. The rebound followed Moody’s downgrade of the U.S. credit rating, citing persistent deficits and rising debt costs. Last week, gold dropped over 3%, its sharpest fall since November, as easing U.S.-China trade tensions increased market risk appetite. Meanwhile, soft inflation and weak U.S. data have reinforced expectations of further Fed rate cuts this year.

The first critical support for gold is seen at the $3120 and the first resistance is located at $3250.

| R1: 3250 | S1: 3120 |

| R2: 3300 | S2: 3030 |

| R3: 3350 | S3: 2956 |

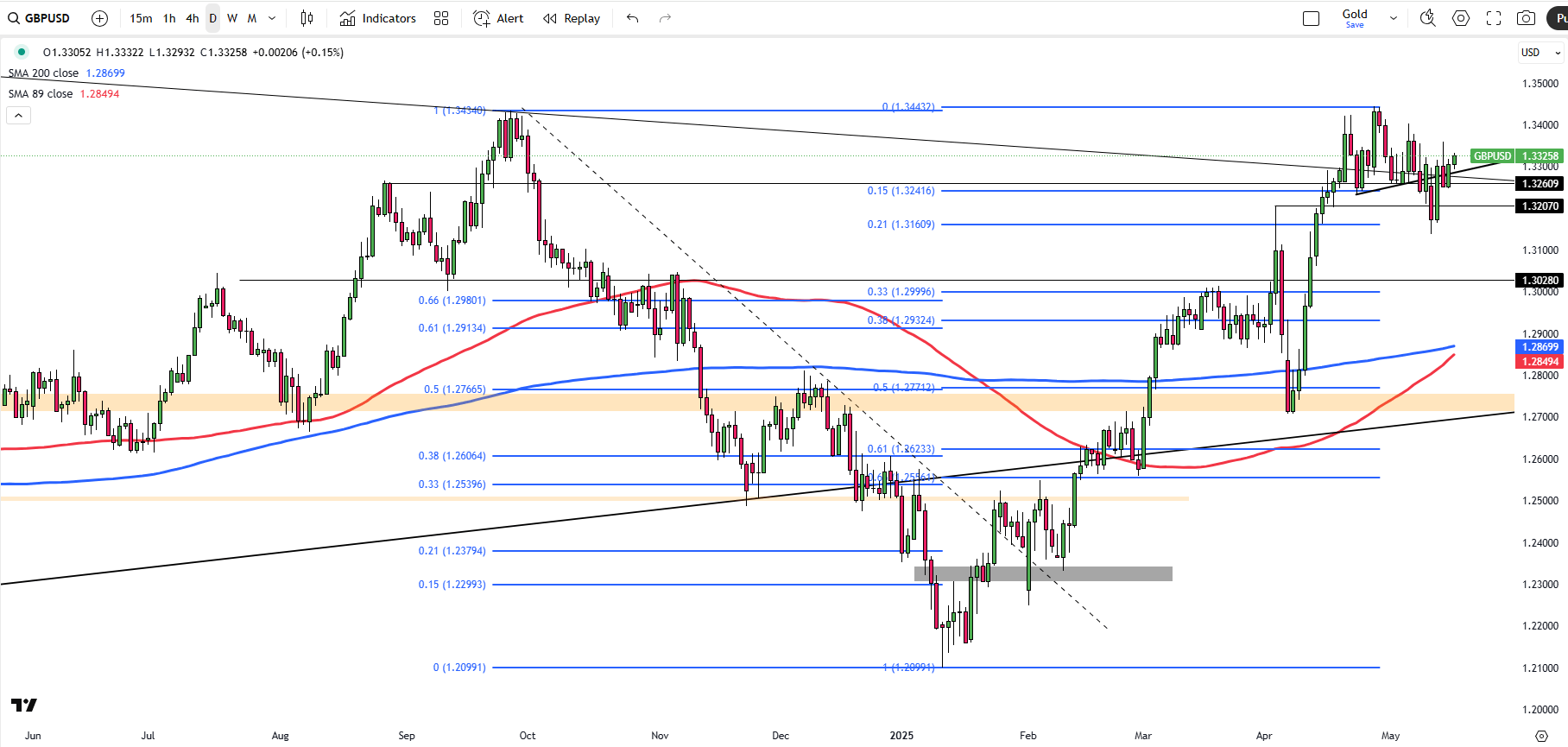

The GBP/USD pair edged toward 1.3300 in Monday’s Asian session, supported by a softer U.S. Dollar following Moody’s credit rating downgrade, which reflected concerns over rising debt and borrowing costs. Weak U.S. data, particularly the sharp drop in consumer sentiment, also strengthened expectations for Fed rate cuts. While positive developments in U.S. diplomacy with China, Iran, and Russia offered some support to the dollar, the Pound found additional strength from better UK GDP figures, which may encourage the Bank of England to keep rates unchanged if inflation remains elevated.

The first critical support for GBP/USD is seen at the 1.3160 and the first resistance is located at 1.3350.

| R1: 1.3350 | S1: 1.3160 |

| R2: 1.3450 | S2: 1.3000 |

| R3: 1.3550 | S3: 1.2960 |

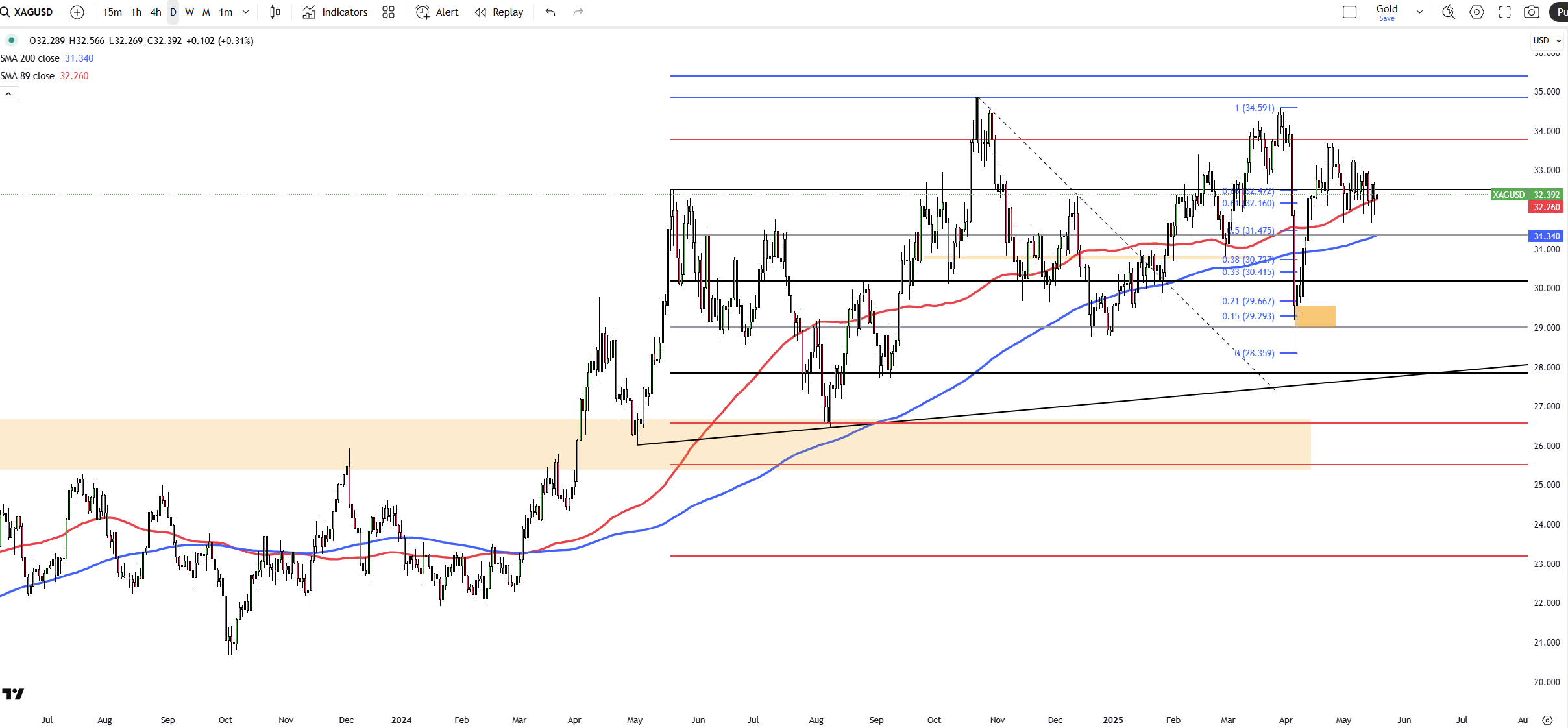

Silver (XAG/USD) declined for a second consecutive session on Monday, hovering around $32.30 per ounce. The retreat followed improved global risk appetite after the US and China agreed to reduce tariffs and geopolitical tensions eased. However, downside may be limited due to renewed safe-haven demand, as Moody’s downgraded the US credit rating and warned of rising debt levels. Additionally, soft US economic data and falling consumer sentiment have reinforced expectations of Fed rate cuts, which may lend support to silver in the coming sessions.

The first critical support for silver is seen at the $31.40 and the first resistance is located at $32.50.

| R1: 32.50 | S1: 31.40 |

| R2: 33.80 | S2: 30.20 |

| R3: 34.20 | S3: 29.80 |

Oil Tanker Attacks Create Volatility

Oil Tanker Attacks Create VolatilityRecent strikes on oil tankers in the Persian Gulf have exposed the extreme vulnerability of global energy supplies. Footage of burning vessels near the Iraqi coastline has saturated financial media, serving as a reminder to market participants of the risks inherent in the region. Whenever tensions escalate in this region, energy traders immediately begin pricing in the possibility of supply disruptions.

Detail Dollar Leads as Markets Reprice Risk (03.12.2026)Currency markets remained under pressure as energy-driven inflation concerns and ongoing geopolitical tensions continued to support the U.S. dollar.

Global markets remained cautious as investors weighed the economic impact of the ongoing Middle East conflict and volatile energy prices.

Then Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!