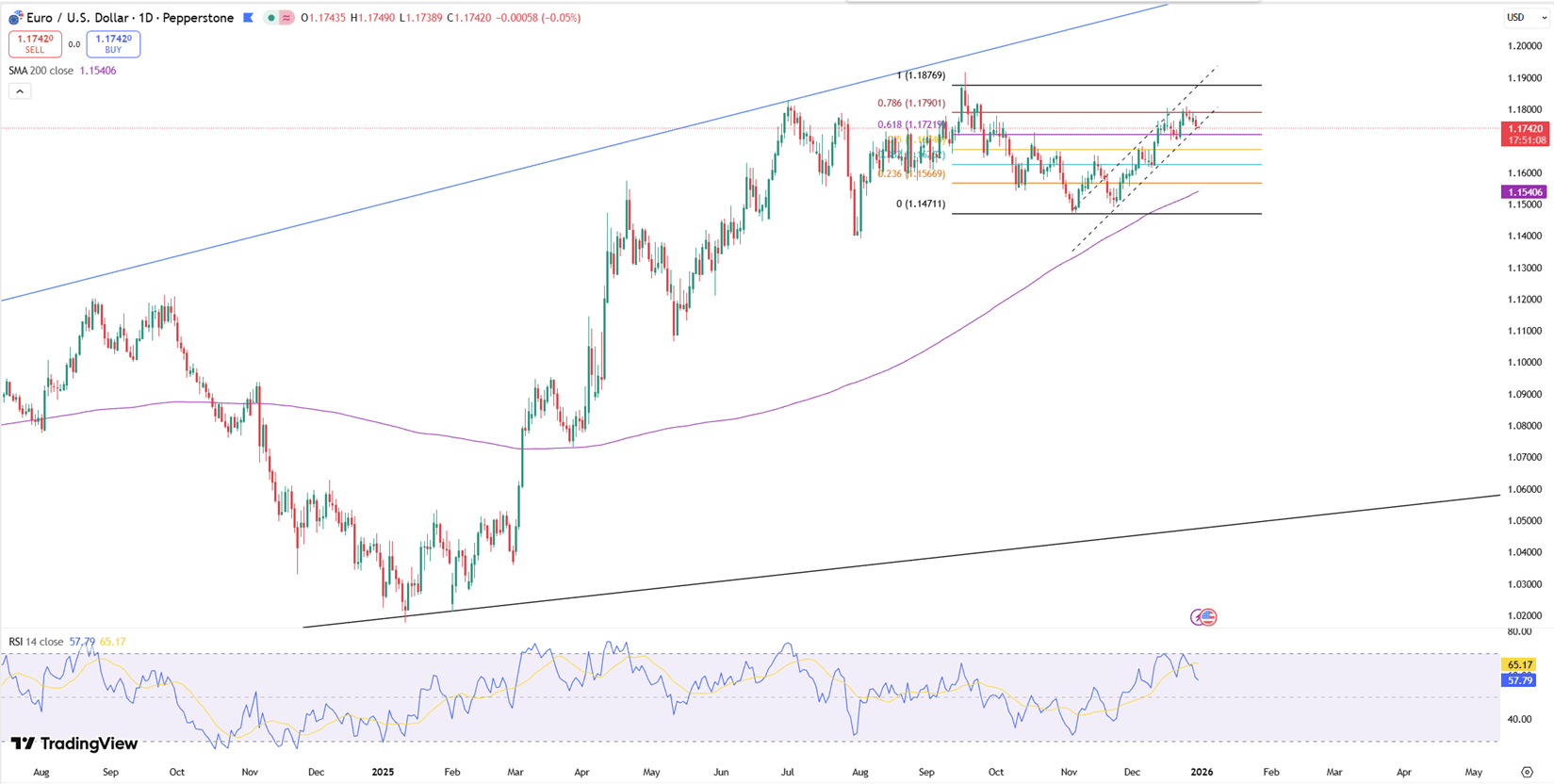

Global markets ended the year with mixed performance as the euro held near 1.1740 during thin year-end trading, supported by the ECB’s pause on rate cuts and expectations of a softer US rate path under a potential Fed leadership change.

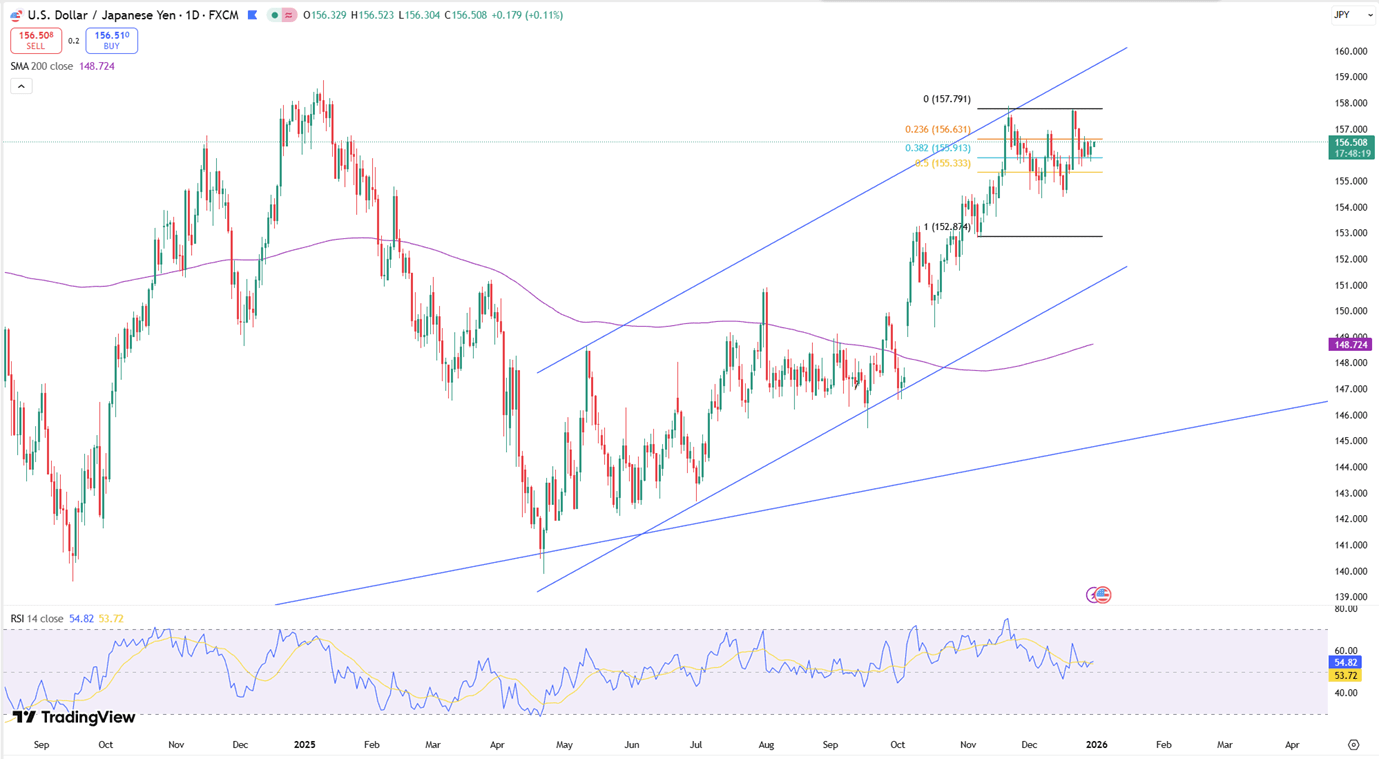

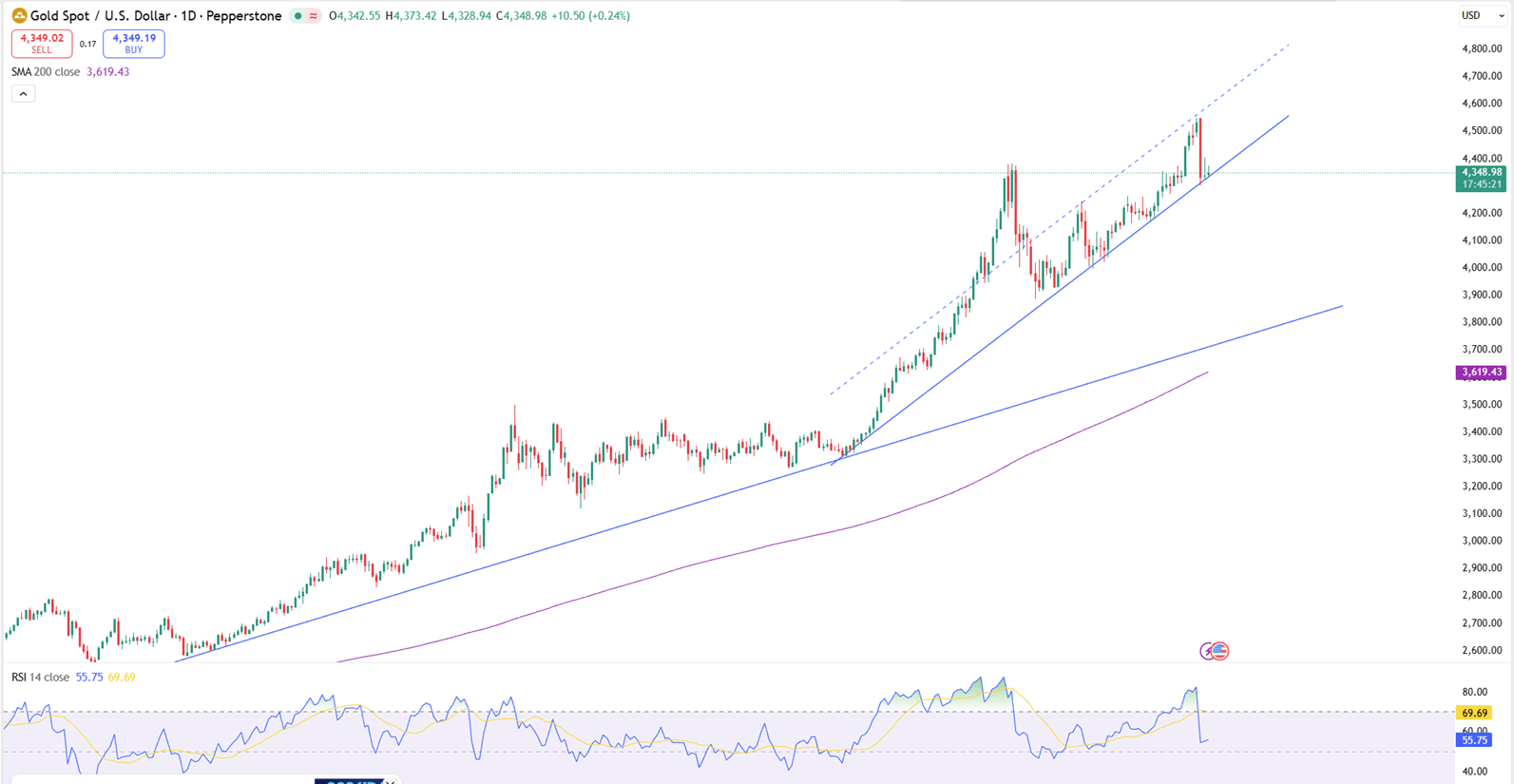

The yen weakened on concerns over Japan’s record budget and fiscal outlook, while gold capped 2025 with its strongest annual gain in decades. Sterling climbed to a three-month high on dollar softness, and silver eased slightly after a powerful year-end rally.

| Time | Cur. | Event | Forecast | Previous |

| All Day | JPY | Japan – Market Holiday | ||

| 01:30 | CNY | Manufacturing PMI (Dec) | 49.2 | 49.2 |

| 13:30 | USD | Initial Jobless Claims | 219K | 214K |

| 15:30 | USD | Crude Oil Inventories | -2.00M | -0.405M |

The euro held near $1.1740 during a quiet holiday week, staying close to its September peak and locking in a 14.7% annual gain for 2025. This strength stems from the ECB’s decision to pause rate cuts in December, despite President Lagarde’s warnings of high uncertainty. However, the US dollar weakened as markets anticipate Donald Trump will appoint a new Fed chair in May to replace Jerome Powell, a move expected to usher in a lower-interest-rate environment.

Technically, 1.1700 is the key support, while resistance is seen at 1.1800.

| R1: 1.1800 | S1: 1.1700 |

| R2: 1.1840 | S2: 1.1630 |

| R3: 1.1890 | S3: 1.1570 |

The Japanese yen slipped toward 156 per dollar in quiet Wednesday trading as investors reacted to Japan’s aggressive fiscal plans. Prime Minister Sanae Takaichi’s cabinet recently approved a record ¥122.3 trillion budget, attempting to balance high spending with debt control by limiting new bond issuance. Despite these efforts, worries remain over Japan’s financial stability. With public debt at double the size of the economy, the government faces significant hurdles in maintaining policy flexibility.

Technically, resistance stands near 156.90, while support is firm at 155.80.

| R1: 156.90 | S1: 155.80 |

| R2: 157.30 | S2: 155.30 |

| R3: 157.80 | S3: 154.70 |

Gold climbed above $4,360 per ounce on the final trading day of 2025, marking its strongest annual performance in over forty years. Bullion surged 66% this year, with gains accelerating after Donald Trump’s April tariff rollout. Prices were further supported by geopolitical tensions, US rate cuts, strong central bank purchases, and increased ETF inflows. Federal Reserve minutes from December revealed broad support for additional rate cuts if inflation continues to cool, though officials remain divided on the specific timing and scale of future moves.

Gold sees support near $4300, while resistance is around $4380.

| R1: 4380 | S1: 4300 |

| R2: 4450 | S2: 4220 |

| R3: 4500 | S3: 4170 |

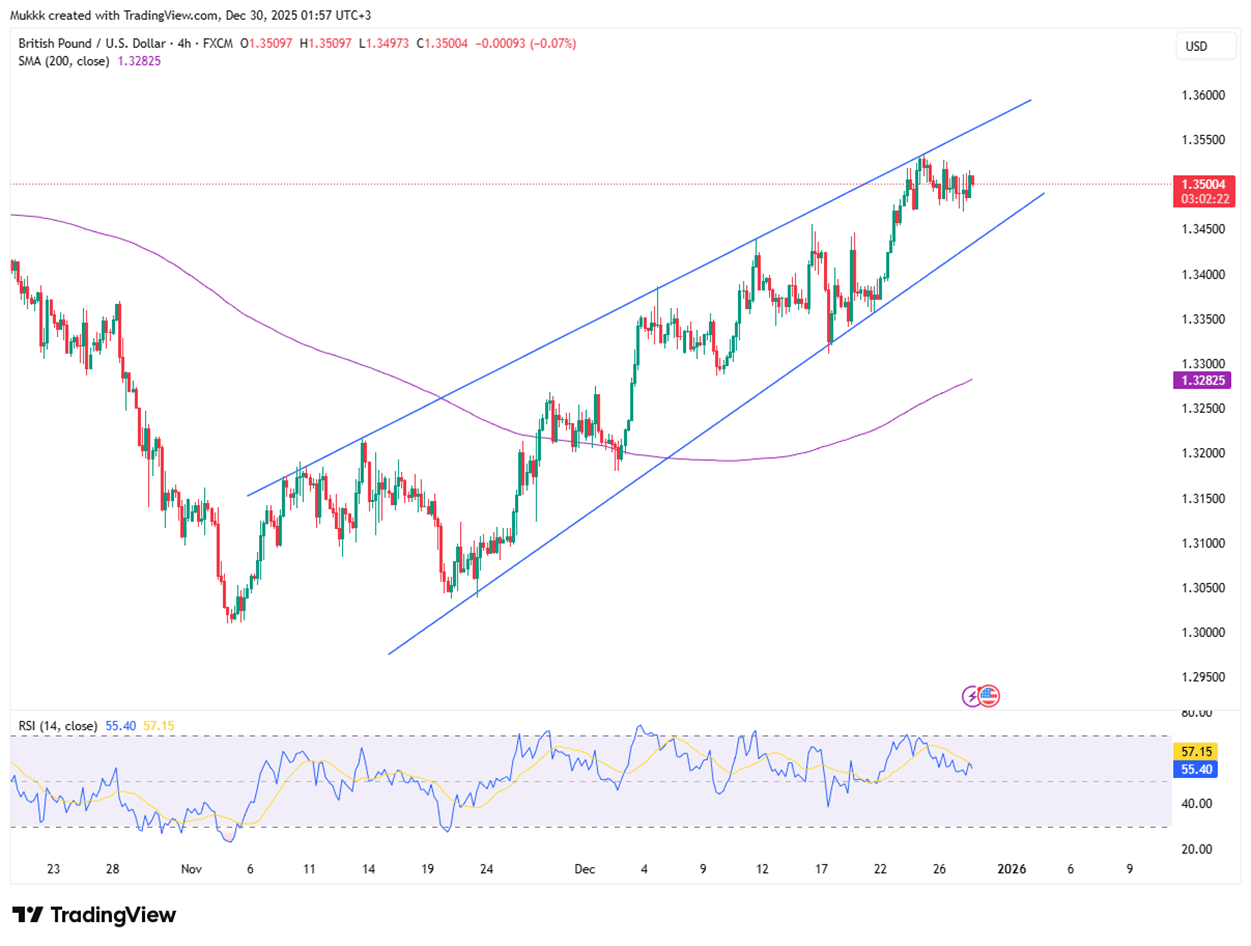

The British pound rose above $1.35, hitting a three-month high as the dollar weakened on expectations of two 2026 Fed rate cuts. This shift narrows the dollar’s interest rate advantage over Sterling. In December, the Bank of England cut rates by 25 basis points to 3.75% via a narrow 5–4 vote. Although November inflation cooled to 3.2%, it stays above the 2% target. Governor Andrew Bailey noted that while further cuts are likely, the pace will be more gradual than investors anticipate.

From a technical view, support stands near 1.3400, with resistance around 1.3510.

| R1: 1.3510 | S1: 1.3400 |

| R2: 1.3570 | S2: 1.3350 |

| R3: 1.3620 | S3: 1.3290 |

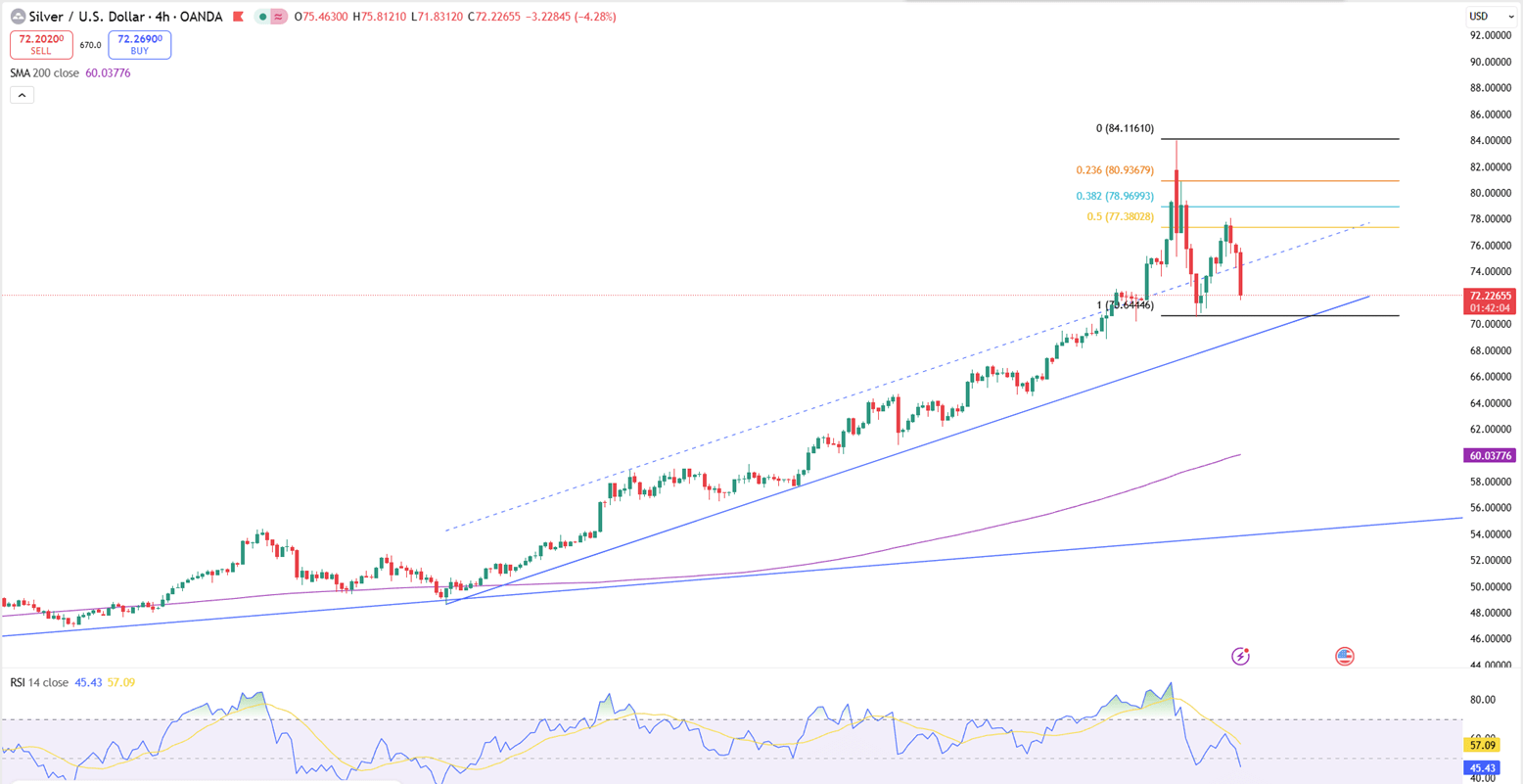

Silver traded near $72.50 during Wednesday’s Asian session, retreating from the 4.5% gain seen previously. Analysts attribute this dip to investors unwinding positions rather than a drop in actual demand. Despite this minor pullback, silver is still poised for an annual gain exceeding 150% in 2025. This record-breaking surge represents the metal's strongest yearly performance to date.

From a technical view, resistance stands near $74.90 while support is located around $71.50.

| R1: 74.90 | S1: 71.50 |

| R2: 76.10 | S2: 70.20 |

| R3: 79.00 | S3: 68.00 |

Global markets remained cautious as investors weighed the economic impact of the ongoing Middle East conflict and volatile energy prices.

Currency markets remained volatile as ongoing Middle East tensions continued to shape global sentiment.

") Hormuz Blockade Rattles Markets (09 - 13 March)

Hormuz Blockade Rattles Markets (09 - 13 March)Global sentiment was dominated this week by the second week of the war with Iran and the effective blockade of the Strait of Hormuz, driving Brent crude prices above $100/barrel. Despite a catastrophic US labor report showing a loss of 92,000 jobs in February, safe-haven demand pushed the US Dollar Index to 99.1. The energy shock has ignited fears of "stagflation," particularly in Europe and Japan, as soaring fuel costs threaten to reverse recent disinflationary trends.

DetailThen Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!