Markets stayed cautious midweek as the U.S. dollar continued to weaken due to fiscal worries, political pressure on the Fed, and anticipation ahead of the jobs report.

| Time | Cur. | Event | Forecast | Previous |

| 09:00 | EUR | Unemployment Rate (May) | 6.2% | 6.2% |

| 12:15 | USD | ADP Nonfarm Employment Change (Jun) | 99K | 37K |

| 14:30 | USD | Crude Oil Inventories | -3.500M | -5.836M |

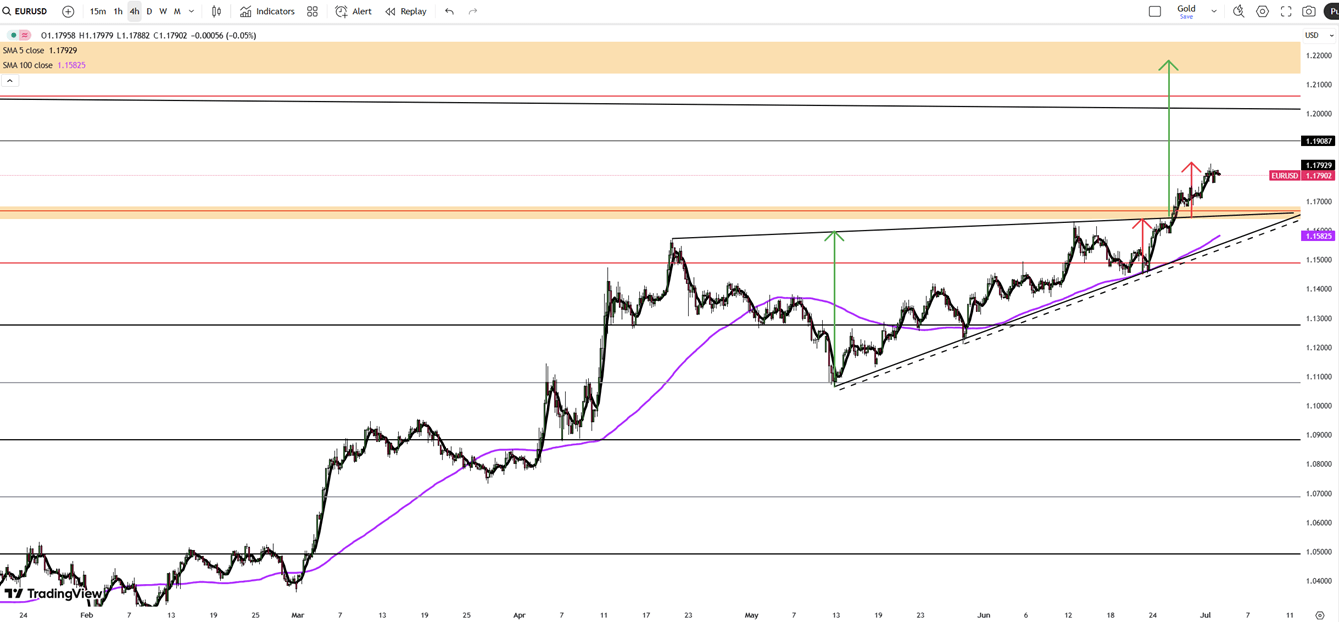

The euro neared $1.1790 on Wednesday, just below its 3.5-year high, as persistent weakness in the U.S. dollar supported demand for the currency. The dollar’s decline was fueled by growing expectations of Federal Reserve rate cuts, with traders pricing in 64 basis points of easing this year, and odds of a July move at 21%.

Fed Chair Jerome Powell’s cautious stance, as well as rising fiscal concerns over Trump’s $3.3 trillion tax-and-spending bill, further eroded confidence in the dollar. Ongoing trade conflicts and a flight from U.S. assets have strengthened the euro’s appeal, positioning it as a key alternative during the dolar’s weakness.

Resistance for the pair is at 1.1830, while support is at 1.1730.

| R1: 1.1830 | S1: 1.1730 |

| R2: 1.1910 | S2: 1.1690 |

| R3: 1.2015 | S3: 1.1630 |

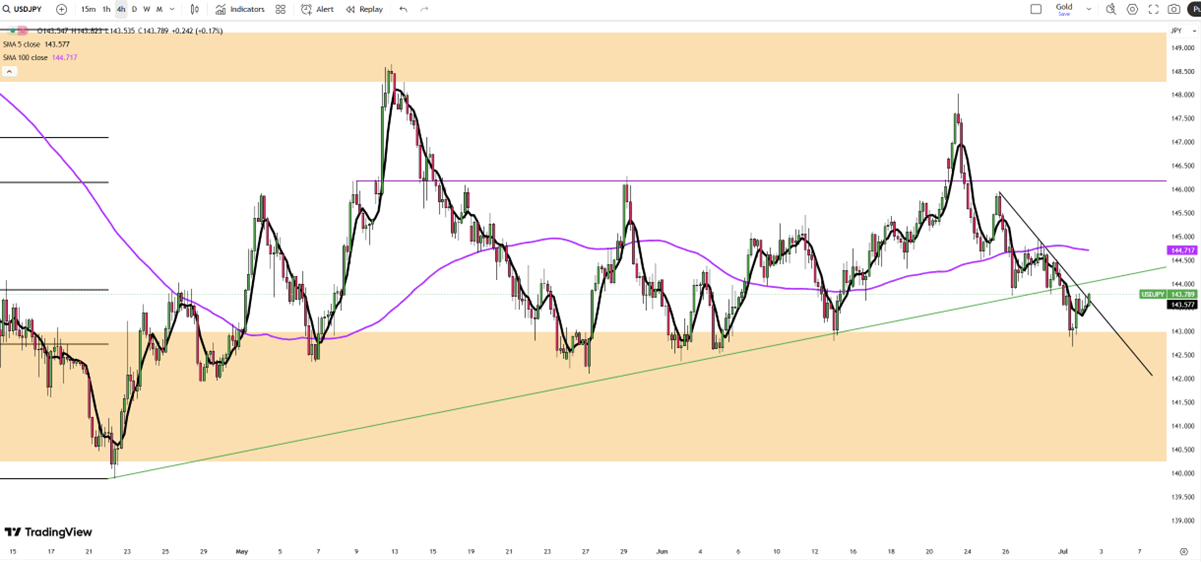

The yen slipped toward 144 per dollar, pulling back from recent three-week highs after Trump threatened a 35% tariff on Japanese goods to push Tokyo into making trade compromises. Trump called the negotiations with Japan “really hard,” renewing his criticism of Japan’s resistance to importing U.S. cars and rice.

Recent data showed an improvement in business sentiment among large manufacturers in Q2, showing the sector’s resilience despite external pressures. Globally, yen remained underpinned by rising expectations of a more dovish Federal Reserve and market concerns over inflation stemming from Trump’s tax-and-spending proposals, which have weakened the U.S. dollar.

The key resistance is at $145.70, and the major support is at $143.55.

| R1: 145.70 | S1: 143.55 |

| R2: 146.20 | S2: 142.45 |

| R3: 147.00 | S3: 141.00 |

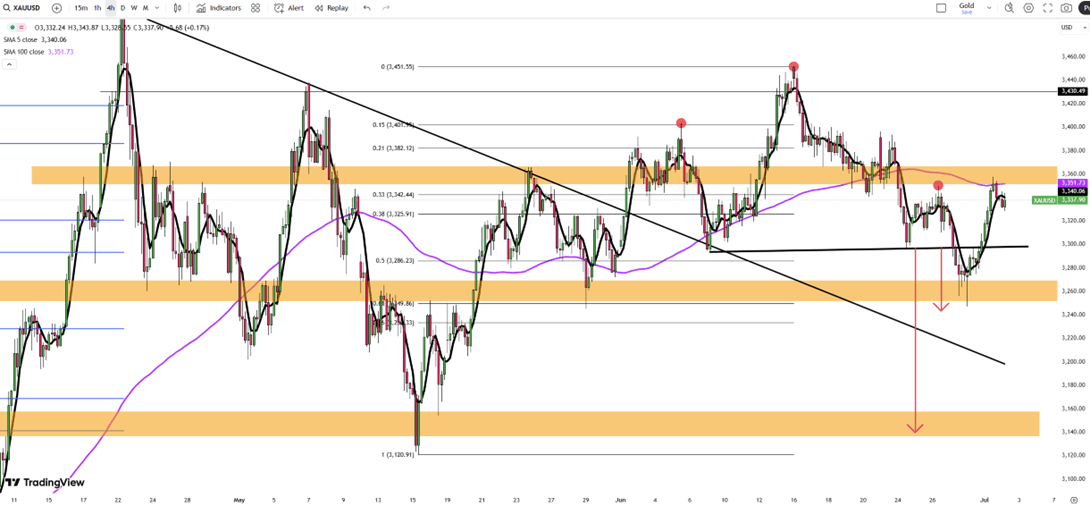

Gold held above $3,330 per ounce with the gains of over 1% from the day before, as a weaker U.S. dollar supported prices. The Senate's approval of Trump’s massive tax-and-spending package, expected to increase national debt by $3.3 trillion, added to these concerns.

Powell stressed a patient stance on rate cuts but didn’t rule out action this month, while Treasury Secretary Scott Bessent predicted cuts by September. Markets are now focused on upcoming U.S. labor data, especially Thursday’s payroll report, for direction on the Fed’s next moves. However, fading geopolitical risks slightly softened the gold demand, as Trump announced a 60-day Gaza ceasefire agreement with Israel and issued a warning to Hamas.

Resistance is at $3,350, while support holds at $3,300.

| R1: 3350 | S1: 3300 |

| R2: 3395 | S2: 3250 |

| R3: 3430 | S3: 3200 |

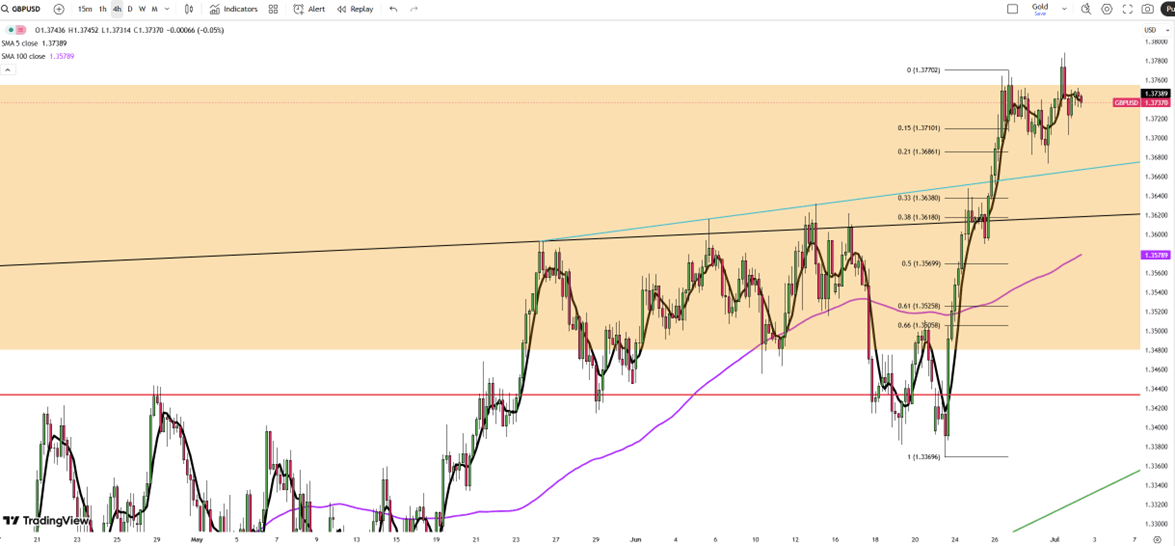

The British pound rose to $1.374, as the U.S. dollar weakness continued to support sterling. Market sentiment remained cautious before Thursday’s U.S. payrolls report.

Growing concerns over the inflationary impact of Trump’s $3.3 trillion tax-and-spending bill and political pressure on the Fed eased investor confidence in the dollar, allowing GBP/USD to build on recent gains. The pound also benefited from Bank of England Governor Andrew Bailey’s comments suggesting inflation pressures persist and that policy remains restrictive for now, giving GBP/USD relative support against the dollar.

Resistance is seen at 1.3760, while support holds at 1.3620.

| R1: 1.3760 | S1: 1.3670 |

| R2: 1.3835 | S2: 1.3620 |

| R3: 1.3900 | S3: 1.3570 |

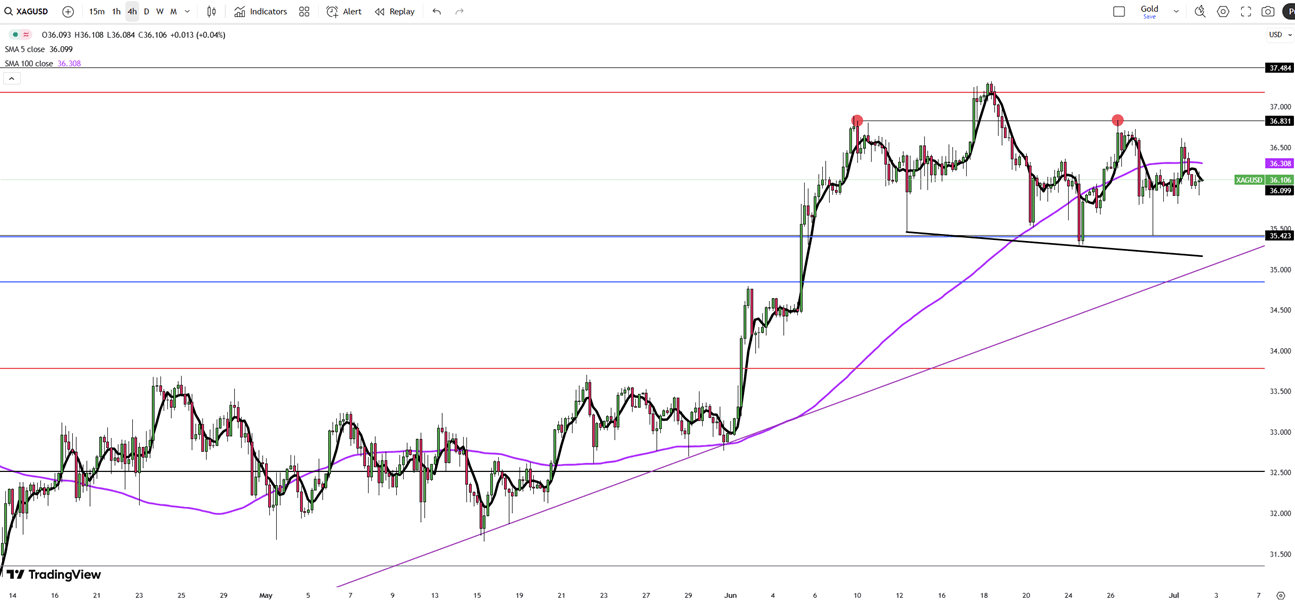

Silver prices dipped slightly with spot silver edging down 0.1% to $36 per ounce, as investors adopted a cautious stance before the U.S. labor market data. While the broader sentiment remained supportive due to a weaker U.S. dollar, which made precious metals more attractive to foreign buyers, traders remained on the sidelines, awaiting the ADP employment report and Thursday’s nonfarm payrolls for clearer direction.

Despite the dip, silver held near multi-year highs, reflecting ongoing demand and strong industrial interest.

Resistance is seen at 36.85, while support holds at 35.40.

| R1: 36.85 | S1: 35.40 |

| R2: 37.50 | S2: 34.85 |

| R3: 39.00 | S3: 33.80 |

Global markets entered a holding pattern as investors awaited key central bank decisions from the Federal Reserve, ECB, and Bank of England.

Markets remained cautious as a stronger U.S. dollar pressured major currency pairs ahead of key central bank decisions.

") Strong USD and Surging Oil Amid Tensions (16–20 March)

Strong USD and Surging Oil Amid Tensions (16–20 March)Global markets faced significant upward pressure on yields and energy prices this week as the conflict in the Middle East entered its third week. The US Dollar Index surged above 100.3, its highest since May 2025, fueled by safe-haven flows and Defense Secretary Pete Hegseth's announcement of the largest planned strike wave against Iran to date. Brent crude breached the $105 threshold following strikes on Kharg Island and warnings that 90% of Iran’s export facilities could be targeted.

DetailThen Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!