The markets experienced significant movement this week across multiple assets. The dollar index stabilized around 100.8 after the Federal Reserve's 50 basis point rate cut, the first in four years. Fed Chair Powell emphasized that further cuts would not be the norm, leaving investors eager for upcoming economic data such as US PMI, PCE prices, and speeches from Fed officials. Meanwhile, the yen weakened past 144 per dollar due to the Bank of Japan's continued dovish stance, and the pound held steady at 1.33, awaiting key PMI data that could shape the central bank's policy direction. In commodities, gold prices remained stable above $2,600 with geopolitical tensions and expectations of further rate cuts, while silver pulled back slightly to $30.90 after a strong recent performance.

The dollar index steadied around 100.8 on Monday after a week of intense volatility, as investors awaited new economic data and speeches from Federal Reserve officials to gain insight into future interest rate moves. Last Wednesday, the Fed cut its policy rate by 50 basis points for the first time in four years, citing confidence in a return to 2% inflation but highlighting growing risks in the labor market. Fed Chair Powell stressed that the central bank is not rushing into further easing and noted that half-point rate cuts are not a new norm.

Looking ahead, Monday's US manufacturing and services PMI data are expected to be released, as well as PCE prices, personal income, and spending reports due later in the week. Speeches from Fed officials, including Atlanta Fed President Bostic, Chicago Fed President Goolsbee, and Minneapolis Fed President Kashkari, are also awaited to shed light on further clues on monetary policy.

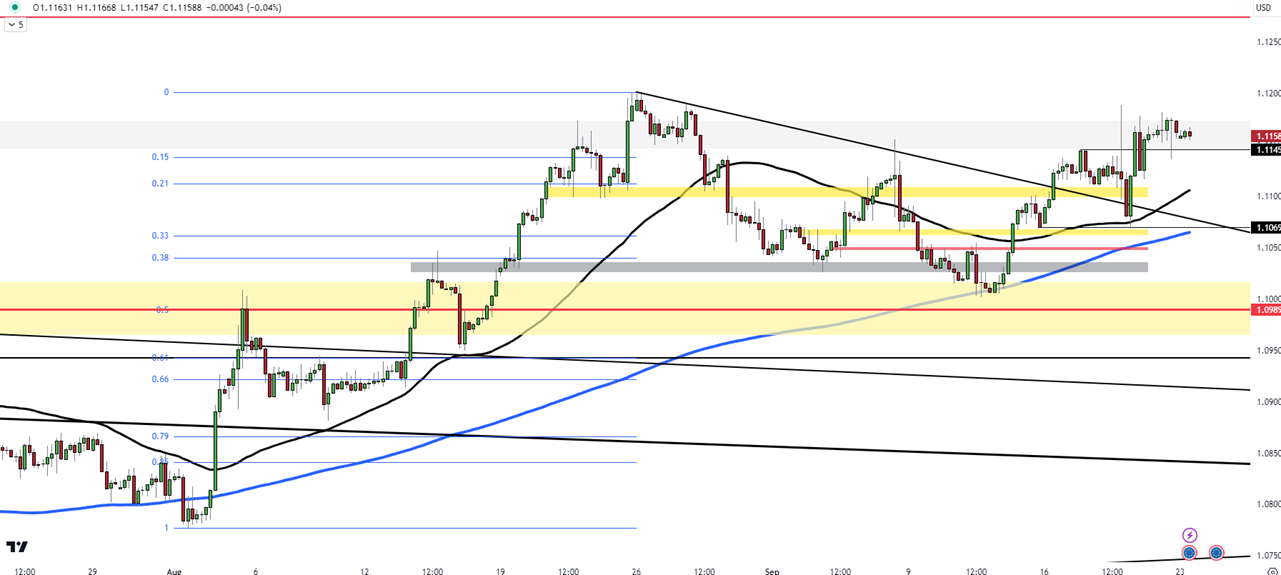

In the currency market, resistance levels for the EUR/USD pair are seen at 1.1200, with further resistance at 1.1250 and 1.1300 if that level is broken. On the downside, support is expected at 1.1150, followed by 1.1100 and 1.1050 below.

| R1: 1.1200 | S1: 1.1150 |

| R2: 1.1250 | S2: 1.1100 |

| R3: 1.1300 | S3: 1.1050 |

The Japanese yen weakened past 144 per dollar in thin holiday trading on Monday, continuing its decline from last week on concerns that the Bank of Japan (BoJ) is in no rush to raise interest rates. Last week, the yen dropped over 2% after the BoJ unanimously decided to maintain its policy rate at 0.25%, in line with expectations. BoJ Governor Kazuo Ueda noted “some weakness” in the economy during his post-meeting press conference, adopting a slightly more dovish tone than in previous statements. His comments diminished the likelihood of a rate hike in October, though a move in December remains anticipated. Ueda also highlighted that the economy is progressing steadily towards a modest recovery, asserting that the central bank will continue to adjust its easing measures if economic and price forecasts are met. Additionally, the yen faced external pressure from a rally in risk assets, spurred by the Federal Reserve’s significant rate cut, which improved the global economic outlook.

In USDJPY, the first support is at 143.60, with subsequent levels at 142.00 and 140.45 below that. On the upside, the initial resistance is at 144.60, followed by 145.90 and 146.50 if this level is breached.

| R1: 144.60 | S1: 143.60 |

| R2: 145.90 | S2: 142.00 |

| R3: 146.50 | S3: 140.45 |

Gold prices were steady at around $2,620 per ounce on Monday, maintaining fresh record highs after surpassing the $2,600 mark last week. This stability was supported by expectations of further interest rate cuts and rising geopolitical tensions, which increased the appeal of bullion. Last Wednesday, the Federal Reserve announced its first interest rate cut in four years, reducing the rate by 50 basis points and indicating that an additional half percentage point cut could occur by year-end. Market participants are now focused on upcoming economic data, including PCE prices, personal income, and spending reports, as well as speeches from several Fed officials, for insights into the interest rate outlook. Meanwhile, gold's safe-haven status was maintained by escalating tensions in the Middle East, with Israel and Hezbollah intensifying their cross-border attacks on Sunday and exchanging hostile threats amid a rapidly worsening situation.

The first support is at 2600 for gold, with the next levels at 2550 and 2530 below. Above, the initial resistance is at 2630, followed by 2650 and 2700 if this level is surpassed.

| R1: 2630 | S1: 2600 |

| R2: 2650 | S2: 2550 |

| R3: 2700 | S3: 2530 |

On Monday morning, the pound was trading around 1.33, with attention focused on the upcoming PMI data, which will be important for insights into the central bank's potential moves in future meetings. Additionally, economic reports from both the US and Europe are expected to influence market volatility throughout the day.

In the GBP/USD pair, immediate support is seen at 1.3300, followed by 1.3270 and 1.3250. On the upside, resistance begins at 1.3340, with further levels at 1.3400 and 1.3450 if the initial barrier is broken.

| R1: 1.3340 | S1: 1.3300 |

| R2: 1.3400 | S2: 1.3270 |

| R3: 1.3450 | S3: 1.3250 |

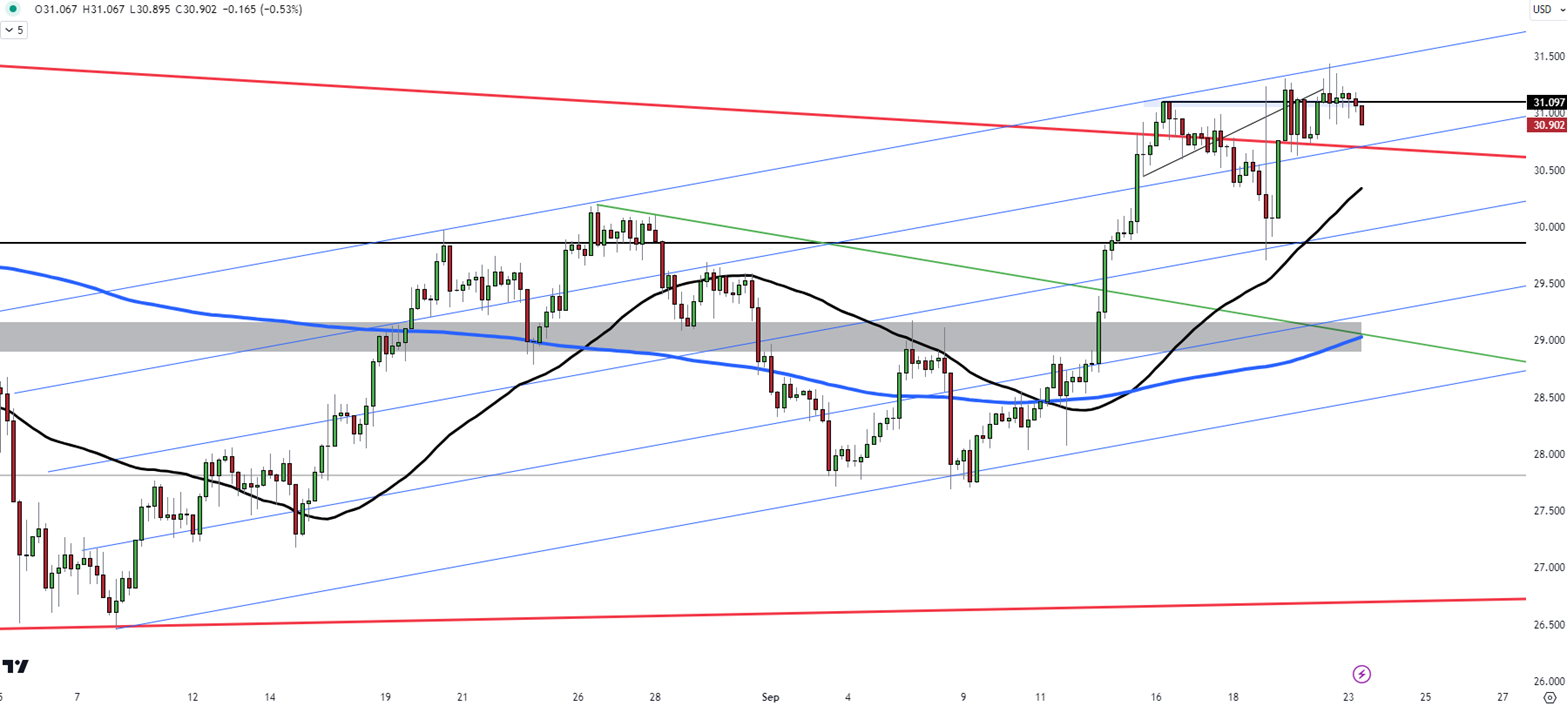

Silver started the week by retreating to around $30.90, diverging negatively from gold. Throughout the week, market participants will be looking for clues regarding potential recession risks and the Federal Reserve's rate-cut roadmap, with key data releases on the horizon. Attention will also be on whether the industrial metal can maintain its performance from the last two weeks while remaining above critical support levels.

In silver, the first support is at 30.75, with subsequent levels at 30.40 and 30.00 below that. On the upside, the initial resistance is at 31.10, followed by 31.50 and 32.00 if this level is surpassed.

| R1: 31.10 | S1: 30.75 |

| R2: 31.50 | S2: 30.40 |

| R3: 32.00 | S3: 30.00 |

Oil Tanker Attacks Create Volatility

Oil Tanker Attacks Create VolatilityRecent strikes on oil tankers in the Persian Gulf have exposed the extreme vulnerability of global energy supplies. Footage of burning vessels near the Iraqi coastline has saturated financial media, serving as a reminder to market participants of the risks inherent in the region. Whenever tensions escalate in this region, energy traders immediately begin pricing in the possibility of supply disruptions.

Detail Dollar Leads as Markets Reprice Risk (03.12.2026)Currency markets remained under pressure as energy-driven inflation concerns and ongoing geopolitical tensions continued to support the U.S. dollar.

Global markets remained cautious as investors weighed the economic impact of the ongoing Middle East conflict and volatile energy prices.

Then Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!