The US dollar index rose toward 99, its fourth straight gain, as investors await today’s jobs report for Fed cues.

While claims rose, layoffs hit a mid-2024 low, supporting expectations that the Fed will hold rates in January but ease later this year. The dollar recorded its strongest week against the euro.

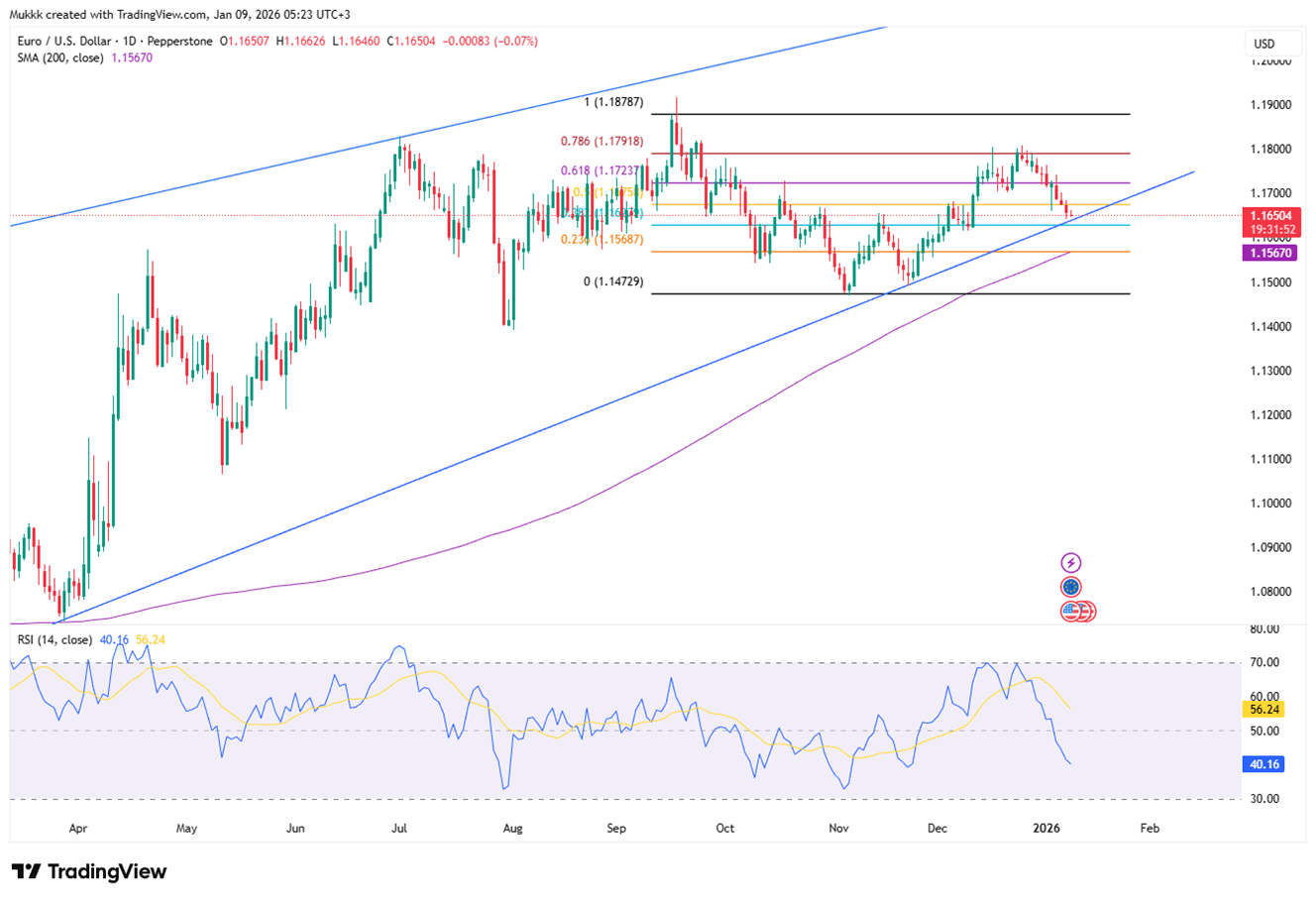

EUR/USD held near 1.1650 as markets waited for the US Nonfarm Payrolls report to set the next directional cue. The yen extended losses on broad dollar strength, while gold and silver steadied ahead of the data despite expectations for Fed cuts later this year. Sterling stayed close to recent highs, supported by policy divergence between the Fed and the Bank of England.

| Time | Cur. | Event | Forecast | Previous |

| 0.3% | 0.1% | |||

| 66K | 64K | |||

| 4.5% | 4.6% |

On Friday, EUR/USD is hovering near 1.1650 as investors await the U.S. Nonfarm Payrolls report. This release is critical for shaping Federal Reserve policy expectations in the near term. The U.S. dollar is currently supported by a resilient labor market, while the euro finds strength in improving Eurozone sentiment and stable inflation. With both the Fed and ECB expected to maintain current interest rates, the pair will likely trade within a tight range until the employment data provides a new catalyst.

Technically, 1.1610 is the key support, while resistance is seen at 1.1690.

| R1: 1.1690 | S1: 1.1610 |

| R2: 1.1740 | S2: 1.1560 |

| R3: 1.1780 | S3: 1.1510 |

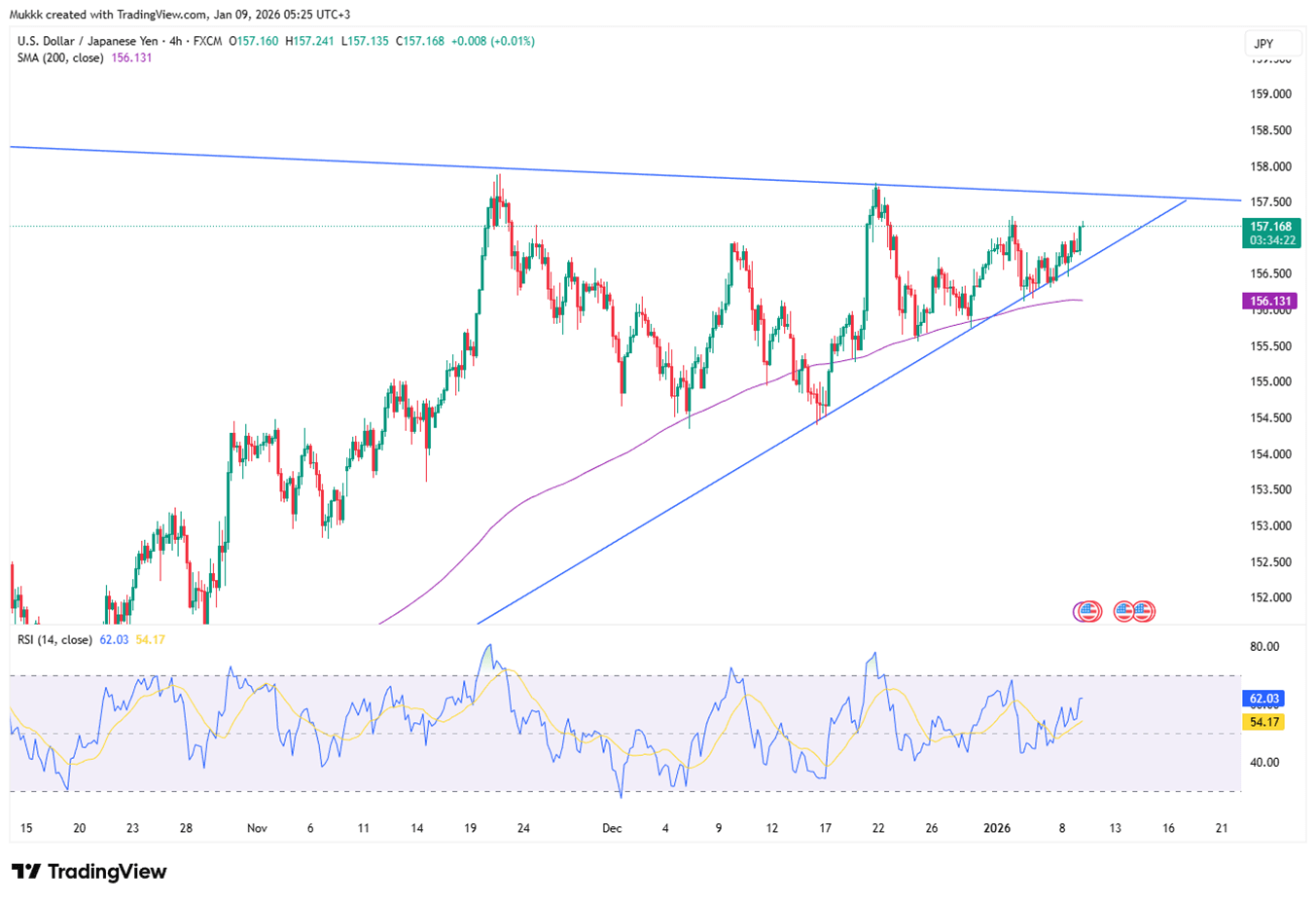

The Japanese yen weakened past 157 per dollar on Friday, marking its fourth straight day of declines. This move was driven by broad U.S. dollar strength as investors recalibrated their Federal Reserve policy expectations. While Japanese household spending rose, the yen remained pressured by falling real wages, which highlight stubborn inflation. Although Bank of Japan officials remain open to raising interest rates, they have stressed that such tightening depends entirely on economic data aligning with their long-term price projections.

Technically, resistance stands near 157.80, while support is firm at 156.80.

| R1: 157.80 | S1: 156.80 |

| R2: 158.50 | S2: 156.20 |

| R3: 159.00 | S3: 155.70 |

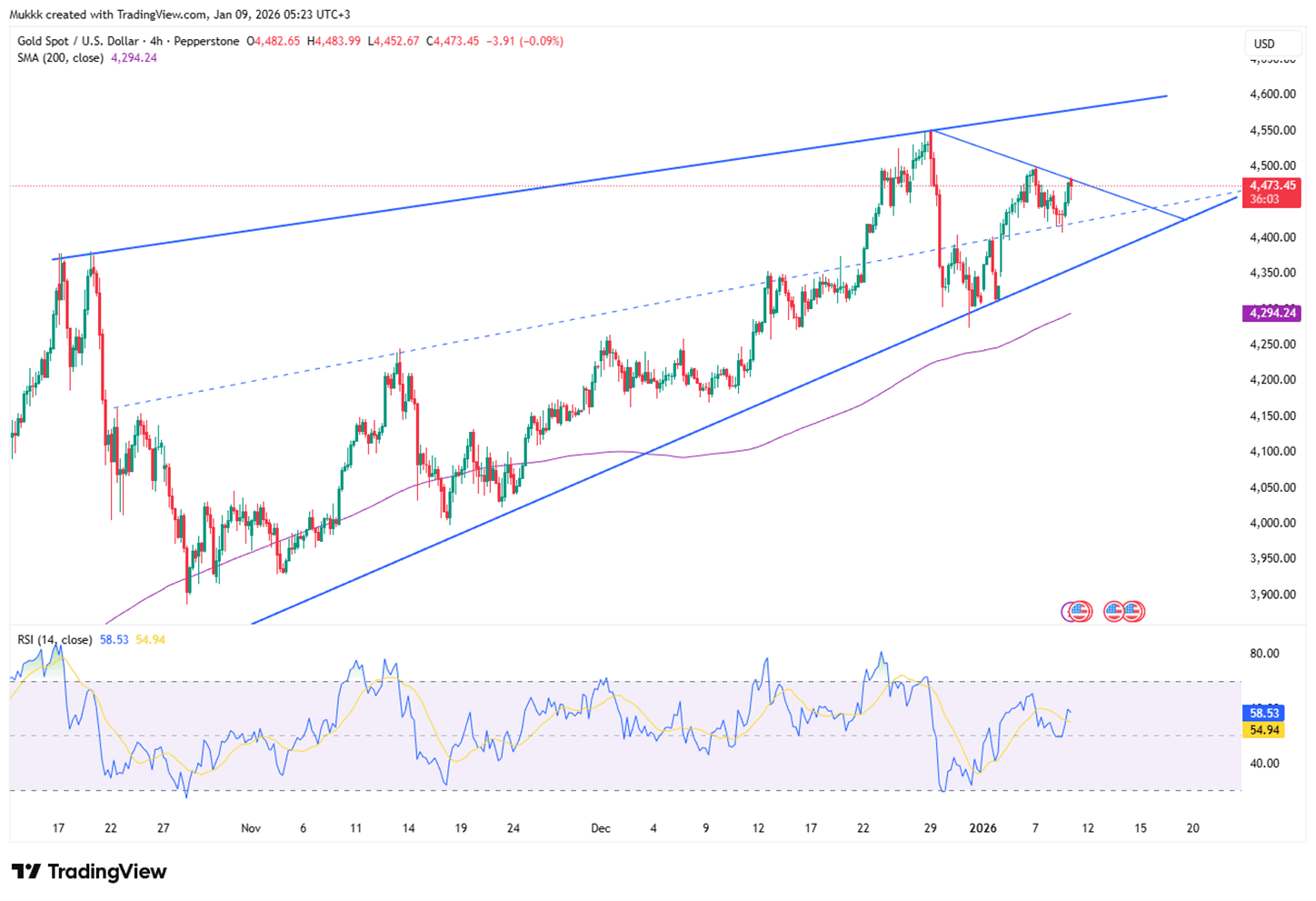

Gold prices stabilized near $4,470 per ounce on Friday as investors paused ahead of the U.S. Nonfarm Payrolls report. While markets anticipate steady employment growth, they still expect two Federal Reserve rate cuts later this year. Despite this momentary stall, gold is set for a strong weekly gain. Prices remain supported by heightened geopolitical risks and consistent central bank demand, particularly as China marked its fourteenth straight month of gold purchases.

Gold sees support near $4415, while resistance is around $4500.

| R1: 4500 | S1: 4415 |

| R2: 4550 | S2: 4350 |

| R3: 4600 | S3: 4270 |

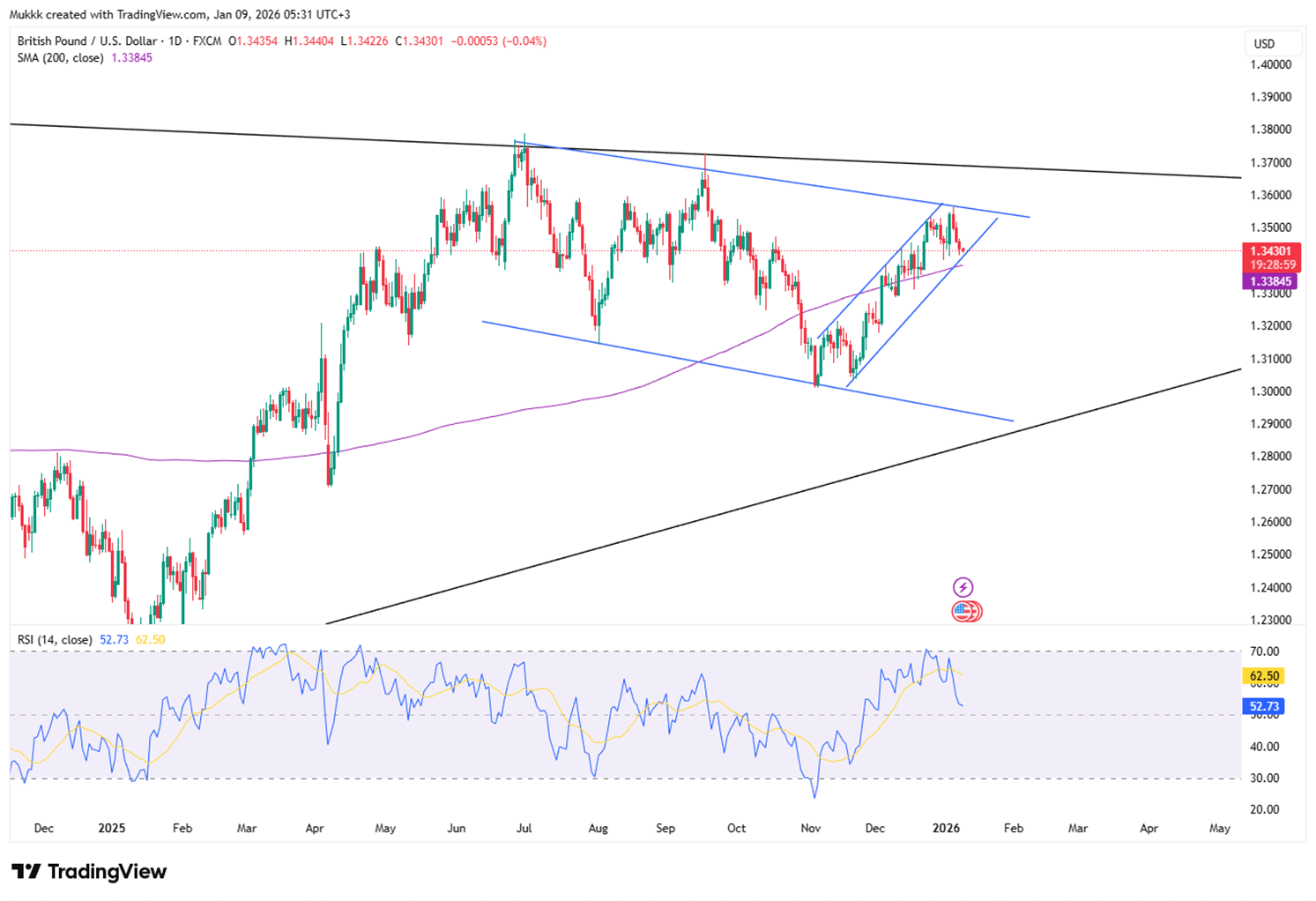

On Friday, the British pound hovered around $1.343, remaining close to its three-month high of $1.352. This strength is driven by diverging policy paths; markets anticipate multiple Federal Reserve cuts this year, whereas only one further Bank of England cut is fully priced in. This outlook provides sterling with a yield advantage. Additionally, while mortgage approvals have dipped, strong consumer borrowing data suggests that UK household demand remains resilient despite higher rates.

From a technical view, support stands near 1.3400, with resistance around 1.3500.

| R1: 1.3500 | S1: 1.3400 |

| R2: 1.3550 | S2: 1.3360 |

| R3: 1.3620 | S3: 1.3310 |

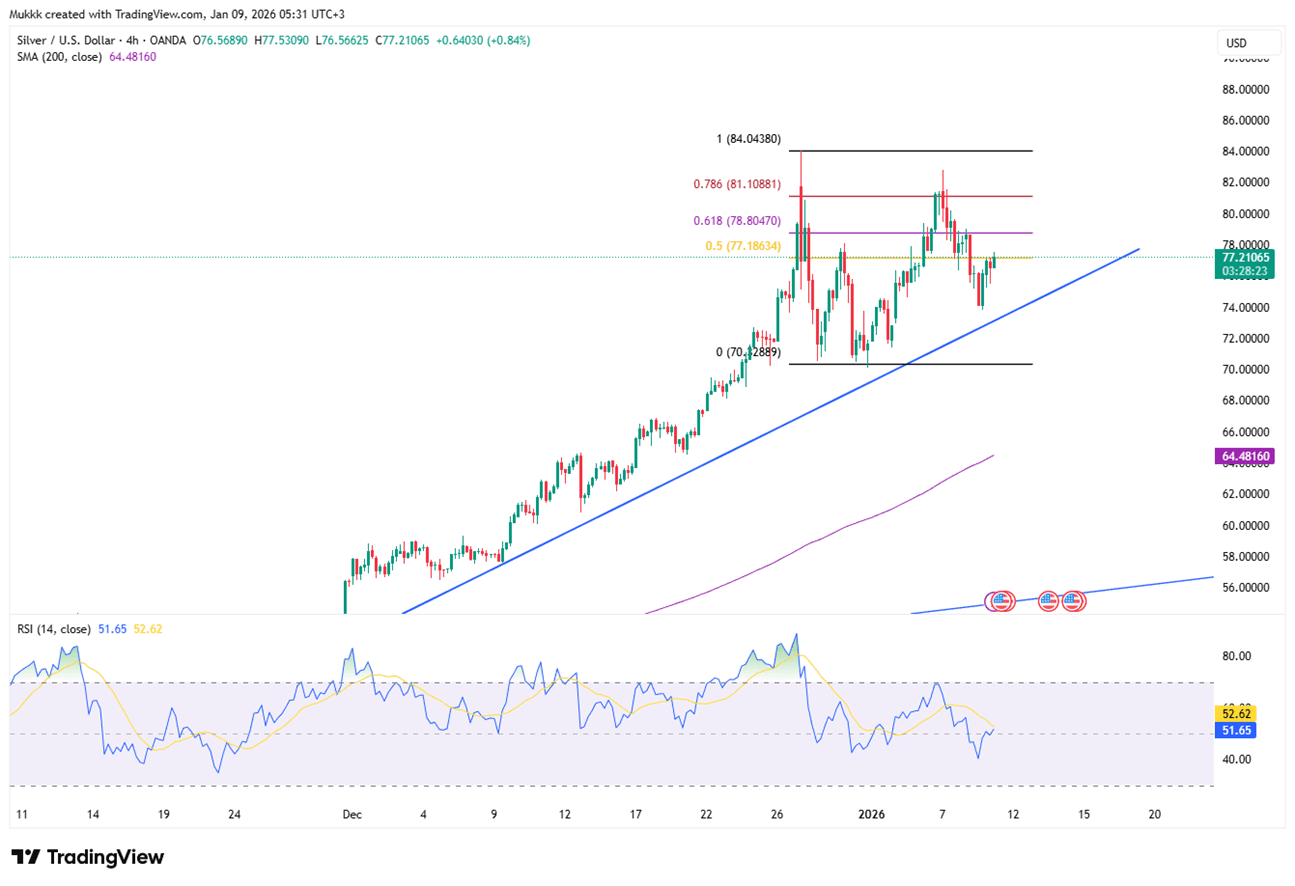

Silver rose to approximately $77.00 on Friday, recovering from earlier losses as traders awaited the U.S. Nonfarm Payrolls report. The metal’s safe-haven status helped it maintain its position despite a resilient U.S. dollar. Silver is currently on track for a weekly gain exceeding 6%, driven largely by intensifying geopolitical tensions. These risks continue to fuel demand for haven assets, providing a strong floor for prices ahead of critical Federal Reserve policy cues.

From a technical view, resistance stands near $78.80 while support is located around $74.10.

| R1: 78.80 | S1: 74.10 |

| R2: 81.00 | S2: 72.40 |

| R3: 82.80 | S3: 70.50 |

Global markets remain dominated by geopolitical risk as escalating conflict between the United States, Israel, and Iran fuels a strong shift toward safe-haven assets. The dollar index hit 99.3 Wednesday, rising for a third day as conflict concerns fueled inflation and shifted Fed rate cut expectations from July to September.

A US court rejected Trump's tariff refund delay as the Dollar (98.5) and 10 year yield (4.04%) held gains amid Middle East escalation and inflation fears.

After Khamenei: Who Will Lead Iran Next?

After Khamenei: Who Will Lead Iran Next?Following the death of Supreme Leader Ali Khamenei, Iran has entered a pivotal transition phase. Senior officials in Tehran are acting swiftly to uphold the existing structure of the Islamic Republic, prioritizing continuity to head off potential internal instability. Despite these efforts, the sudden leadership vacuum has sparked intense political and military maneuvering behind the scenes.

DetailThen Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!