The Euro weakened significantly against the US Dollar, driven by a sharp decline in German Factory Orders and expectations of aggressive interest rate cuts by the European Central Bank.

The US Dollar gained strength from hawkish signals from the Federal Reserve, concerns over Trump's trade policies, and an underperforming ADP employment report. Gold dipped to $2,650 but found support from ETF inflows and weaker U.S. private employment figures.

| Time | Cur. | Event | Forecast | Previous |

| 18:00 | USD | Atlanta Fed GDPNow (Q4) | 2.7% | 2.7% |

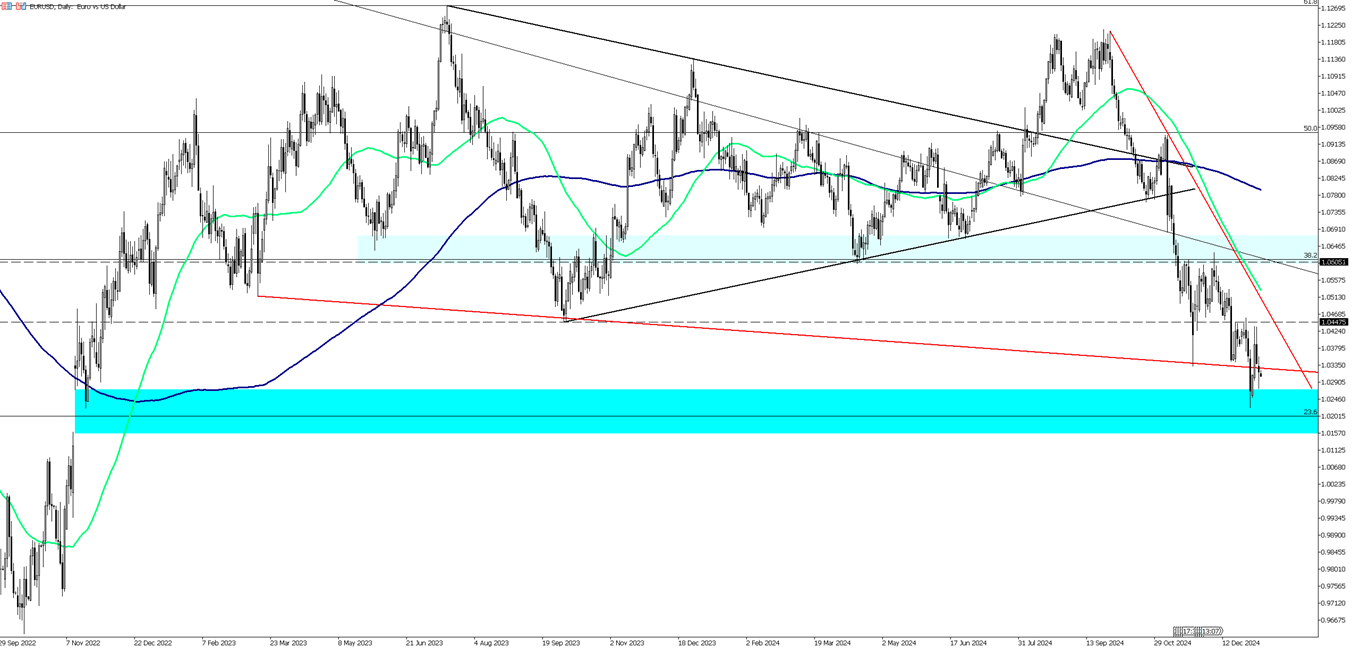

The EUR/USD pair remains in negative territory for the third straight day, trading near 1.0310 during Thursday’s early European session. Weak German Factory Orders for November and expectations of aggressive ECB rate cuts this year are pressuring the euro. Focus later shifts to Eurozone Retail Sales and remarks from Federal Reserve officials.

German Factory Orders dropped 5.4% month-over-month in November, higher than October’s 1.5% decline and the expected flat reading, further weighing on the euro.

The dollar index held steady at 109 as markets analyzed the Fed’s December meeting minutes, which highlighted inflation concerns and the potential economic impacts of Trump’s trade and immigration policies. The Fed signaled it may soon slow the pace of policy easing. Reports of Trump considering a national economic emergency for tariffs also supported the dollar. Meanwhile, the ADP report showed private-sector employment fell to a four-month low in December, raising labor market concerns ahead of Friday’s payrolls report.

Technically, resistance is at 1.0460, with further levels at 1.0515 and 1.0575. Support is at 1.0270, followed by 1.0220 and 1.0125.

| R1: 1.0460 | S1: 1.0270 |

| R2: 1.0515 | S2: 1.0220 |

| R3: 1.0575 | S3: 1.0125 |

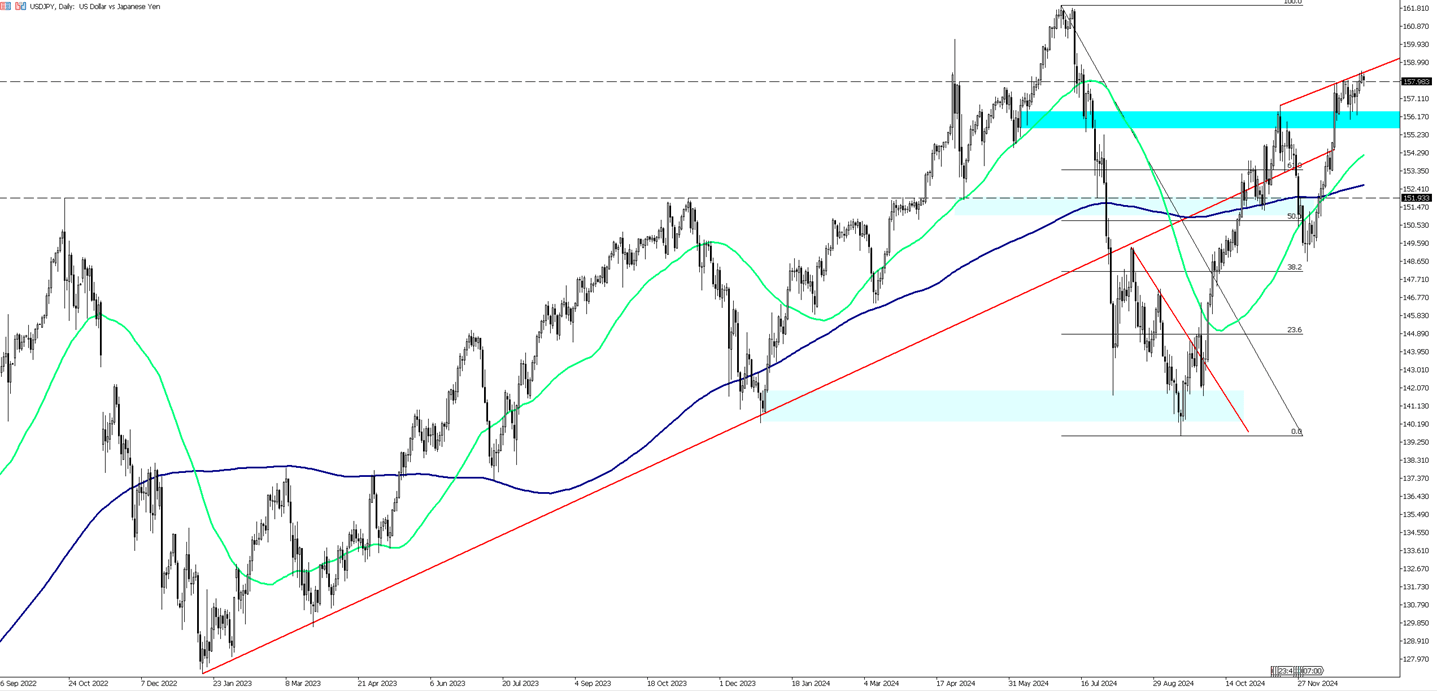

The Japanese yen traded near 158 per dollar on Thursday, close to a six-month low, pressured by the dollar’s strength. The greenback remains firm due to hawkish Fed signals and concerns over Trump’s tariff threats.

Domestically, Japan’s real wages dropped 0.3% year-on-year in November, the fourth month of decline, raising doubts about potential BOJ rate hikes. Consumer sentiment weakened in December, reinforcing expectations for a dovish BOJ stance. Finance Minister Katsunobu Kato reiterated warnings about speculative currency moves, signaling possible intervention if volatility continues.

Resistance is at 158.60, with further levels at 160.00 and 161.00. Support lies at 154.90, followed by 153.40 and 152.40.

| R1: 158.60 | S1: 154.90 |

| R2: 160.00 | S2: 153.40 |

| R3: 161.00 | S3: 152.40 |

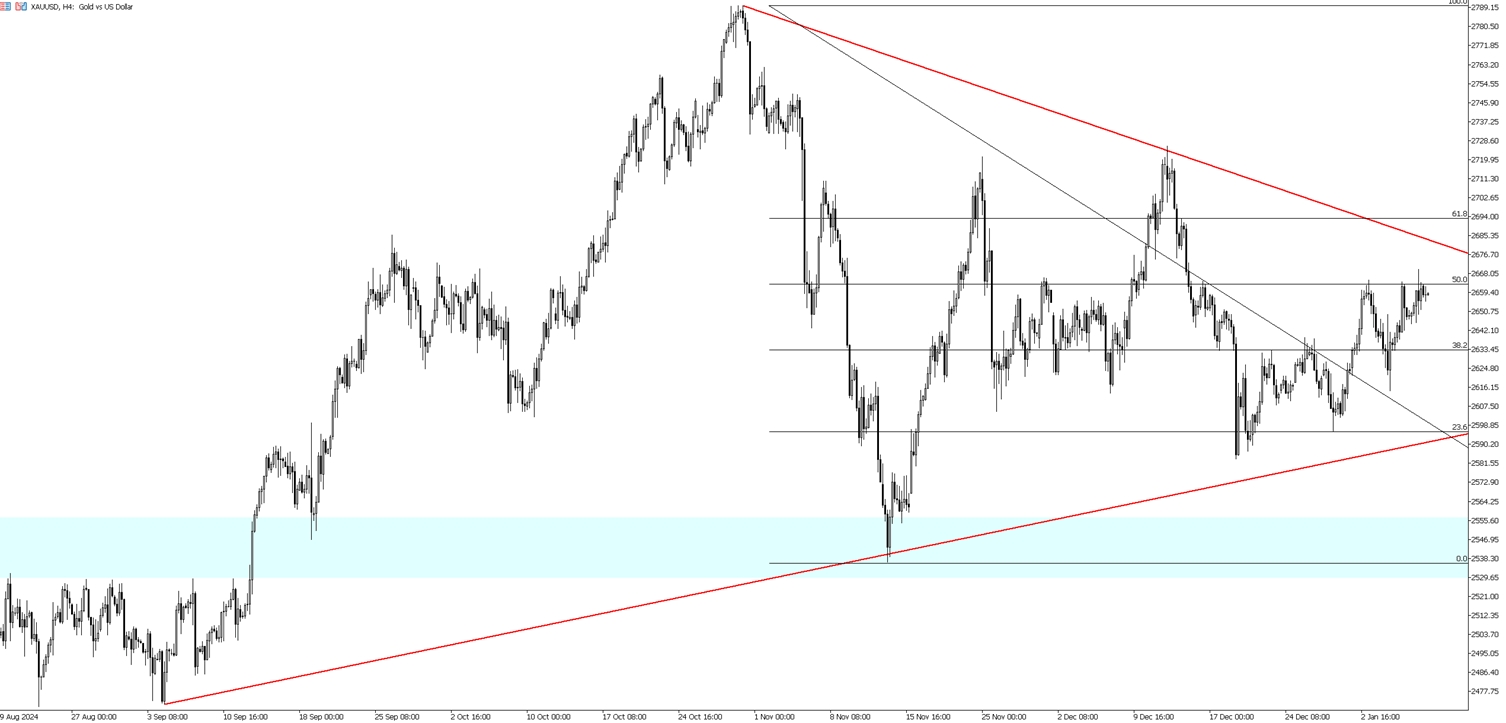

Gold edged lower to around $2,650 per ounce on Thursday, reversing two days of gains as investors assessed the Fed's policy outlook ahead of key jobs data. FOMC minutes indicated inflation may slow this year but highlighted persistent price risks, partly influenced by Trump’s policies. The Fed also hinted at potentially slowing the pace of policy easing, reducing the appeal of non-yielding assets.

The precious metal received some support from a weaker-than-expected private employment report for December, suggesting the Fed might ease its stance on rate cuts. Additionally, gold-backed ETFs recorded their first inflows in four years, led by Asia, with North American funds seeing their first positive annual flow since 2020 and European outflows declining compared to 2023, according to the World Gold Council.

Resistance is at 2,665, with additional levels at 2,695 and 2,725. Support stands at 2,630, followed by 2,620 and 2,600.

| R1: 2665 | S1: 2630 |

| R2: 2695 | S2: 2620 |

| R3: 2725 | S3: 2600 |

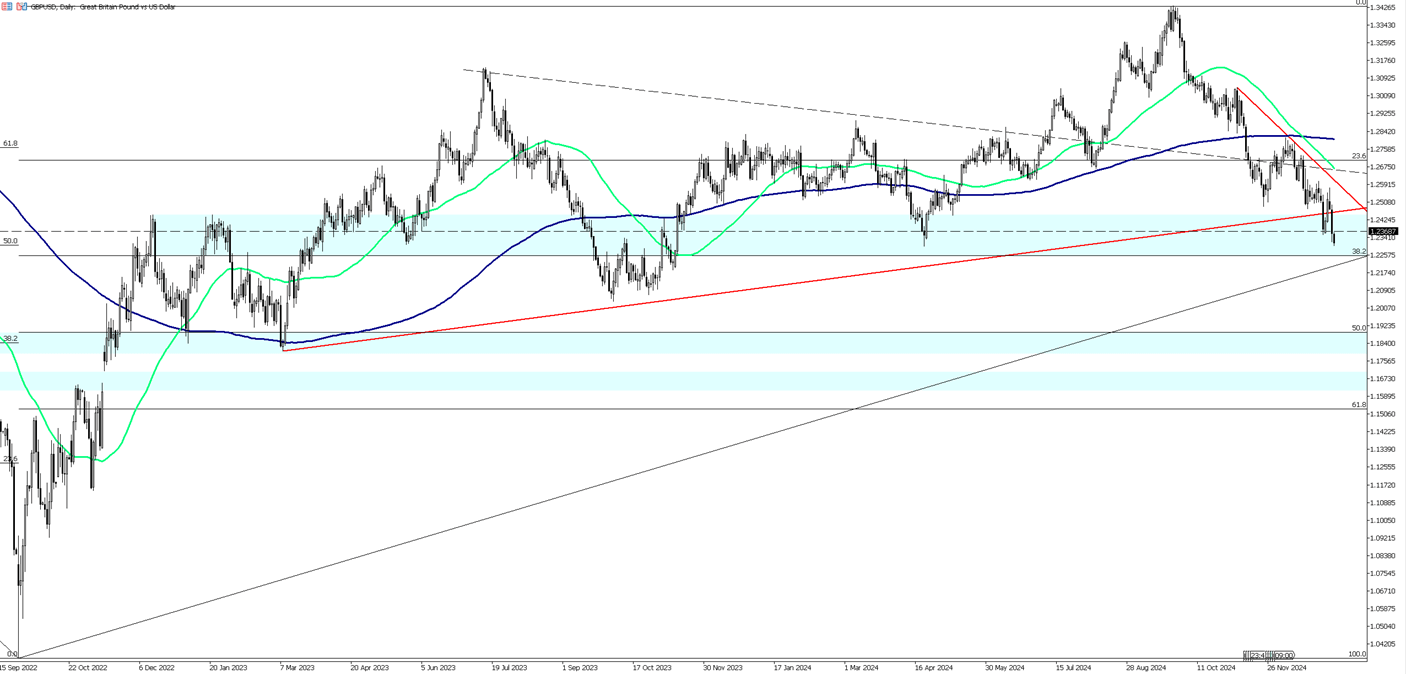

GBP/USD is trading near 1.2315 on Thursday, retreating from 1.2570, a level buyers have struggled to reclaim. The pair briefly dipped below 1.2350, nearing multi-month lows. With no major UK economic data this week, cable traders are focusing on broader market flows, particularly the U.S. dollar. Attention turns to the week's end, with Fed speeches and December’s Challenger Job Cuts data ahead of Friday’s anticipated Nonfarm Payrolls (NFP) report.

On Wednesday, the ADP Employment Change report showed weaker-than-expected December hiring, with 122K jobs added versus a 140K forecast and November’s 146K. ADP also reported the slowest wage growth since mid-2021.

Fed meeting minutes released the same day revealed heightened concern over Trump's proposed tariffs, previously downplayed. Policymakers noted potential impacts on monetary decisions, emphasizing a cautious outlook. The Fed agreed to slow the pace of rate cuts, with fewer reductions expected in 2025 than initially anticipated.

Technically, resistance is at 1.2350, with additional levels at 1.2410 and 1.2500. Support is at 1.2300, followed by 1.2265 and 1.2190.

| R1: 1.2350 | S1: 1.2300 |

| R2: 1.2410 | S2: 1.2265 |

| R3: 1.2500 | S3: 1.2190 |

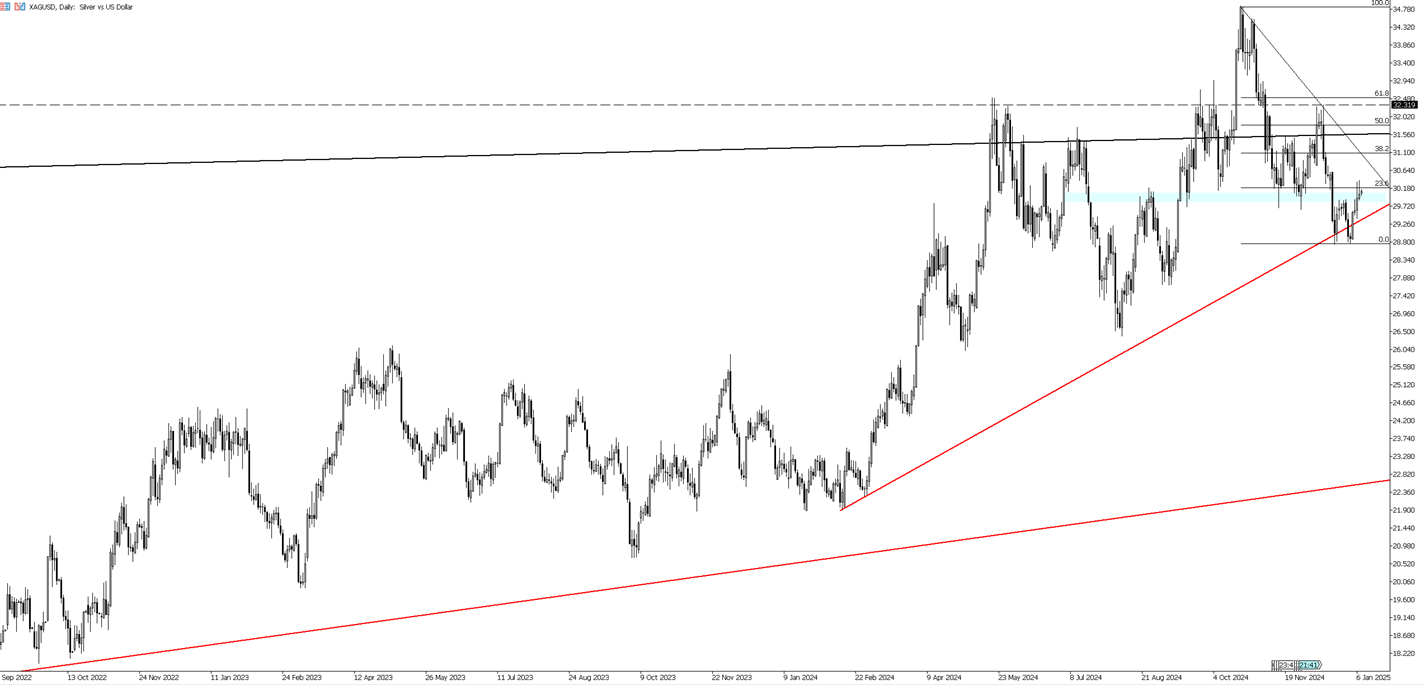

Silver prices held above $30 per ounce on Thursday, near a three-week high, as investors evaluated the Federal Reserve's cautious stance on rate cuts. Uncertainty around inflation and potential tariffs under Trump has supported silver's appeal as a trusted asset.

Strong industrial demand, driven by silver's use in renewable energy and electronics, and supply disruptions from labor strikes and mining issues have further supported prices. Geopolitical tensions and economic uncertainties have also increased market volatility, prompting investors to seek stability in precious metals.

Resistance is at 30.35, with further levels at 30.70 and 31.00. Support is at 29.85, followed by 28.50 and 28.00.

| R1: 30.35 | S1: 29.85 |

| R2: 30.70 | S2: 28.50 |

| R3: 31.00 | S3: 28.00 |

Global markets remained dominated by dollar strength as geopolitical tensions and rising energy prices reshaped monetary expectations.

Oil Tanker Attacks Create Volatility

Oil Tanker Attacks Create VolatilityRecent strikes on oil tankers in the Persian Gulf have exposed the extreme vulnerability of global energy supplies. Footage of burning vessels near the Iraqi coastline has saturated financial media, serving as a reminder to market participants of the risks inherent in the region. Whenever tensions escalate in this region, energy traders immediately begin pricing in the possibility of supply disruptions.

Detail Dollar Leads as Markets Reprice Risk (03.12.2026)Currency markets remained under pressure as energy-driven inflation concerns and ongoing geopolitical tensions continued to support the U.S. dollar.

Then Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!