America’s housing market is still moving through an unusual cycle.

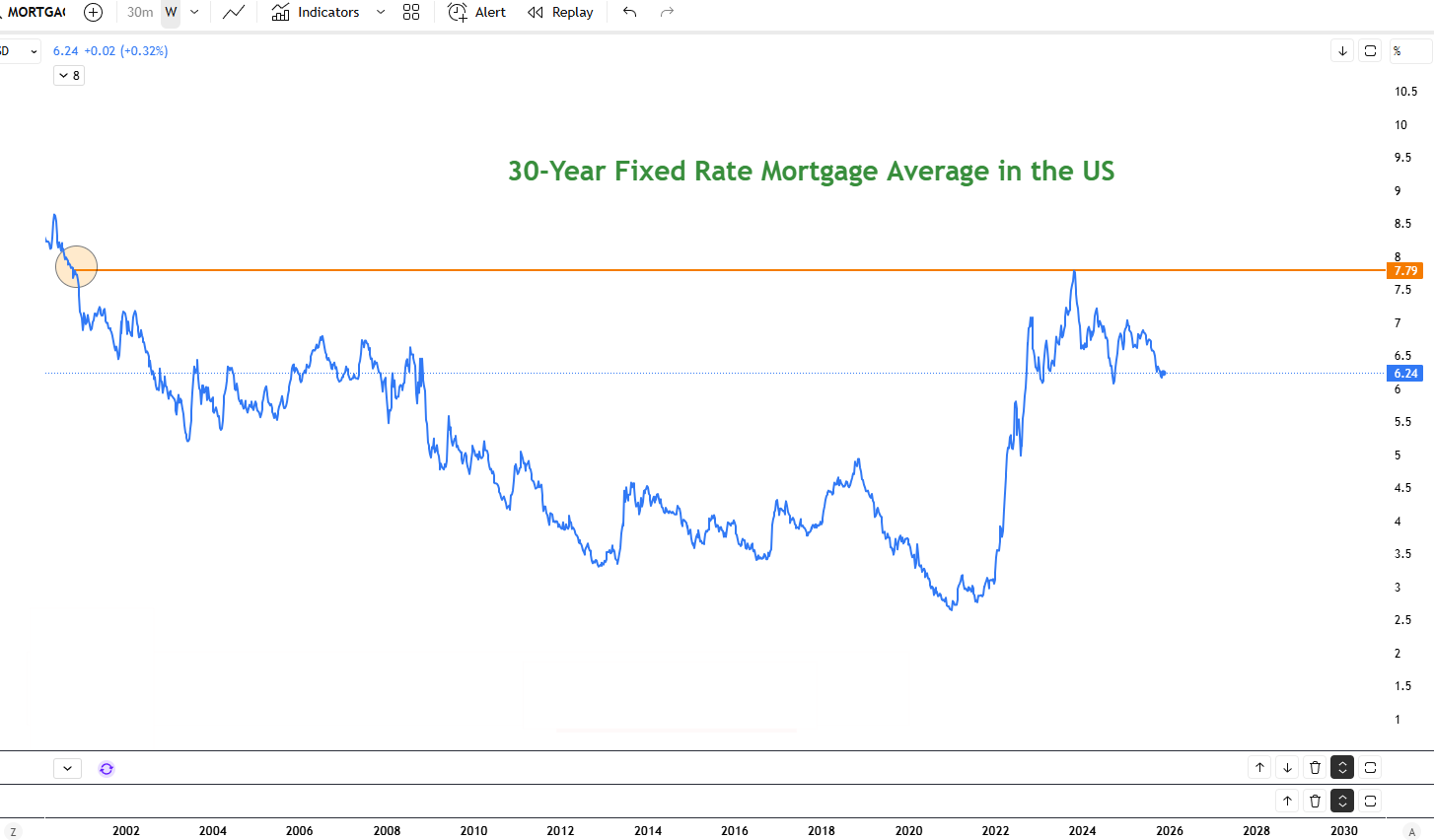

Mortgage rates remain near multi-year highs, yet demand has not collapsed as many analysts once predicted. Instead, buyers are adjusting to a new environment defined by expensive financing, limited inventory, and home prices that show little interest in correcting in any meaningful way. This struggle between affordability and persistent demand sits at the heart of the current debate.

One idea circulating lately is the introduction of 50-year mortgages. Supporters view them as a potential lifeline for buyers who have been pushed out of the market. The appeal is clear: lower monthly payments and a path to ownership in an increasingly expensive landscape.

Critics see the other side. Extending payments over half a century may ease the short-term pressure, but it does not address the core issue: prices are too high. Some argue that longer maturities could even inflate prices further by giving buyers more borrowing power, ultimately worsening the same affordability challenge policymakers are trying to fix.

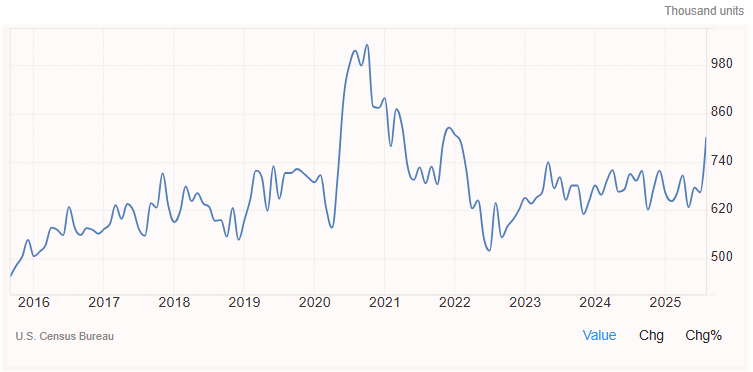

Recent data paints a complicated picture. Mortgage applications have improved slightly, supported by a modest pullback in long-term yields. But new-home construction and existing-home sales still point to a market that is cooling rather than recovering. Builders are offering incentives, buyers are negotiating more aggressively, and sellers are becoming more realistic about pricing. Yet nothing in the current trends suggests a broad decline. The market is stabilizing, not collapsing.

Looking ahead, the central question is whether any policy shift (including ultra-long mortgages) can truly improve affordability. Without more supply or a meaningful drop in rates, households will continue to face the same structural barriers. A 50-year mortgage may offer marginal relief, but it is unlikely to resolve the imbalance that has shaped the US housing market for years. For now, the outlook remains unchanged: tight supply, cautious buyers, and a market waiting for a more definitive signal before deciding where it goes next.

Signs of diplomatic progress between Washington and Tehran reduced immediate concerns about energy supply disruptions and inflation pressures.

Detail Week’s Optimism Starts to Fade (05.28.2026)Recent military developments in Iran weakened confidence in a near-term diplomatic breakthrough.

Detail Currencies Advance as Oil Concerns Ease (05.26.2026)Improving prospects for a US-Iran agreement supported risk sentiment and reduced demand for the US dollar.

DetailThen Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!