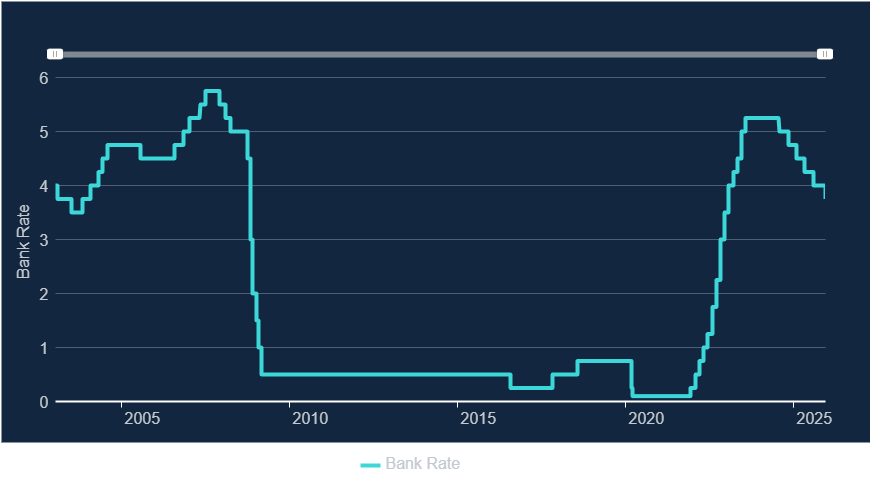

The Bank of England cut its policy rate by 25 basis points to 3.75%, marking the fourth reduction of the year as weaker growth, softer labor conditions, and fast disinflation reshaped the policy outlook.

The decision was passed by a 5-4 vote within the Monetary Policy Committee, emphasizing how finely balanced the debate has become. While inflation is moving lower, it remains above the 2% target, keeping policymakers cautious even as economic momentum fades.

Despite the rate cut, the Bank avoided signaling a shift toward rapid accommodation. Officials stressed that inflation progress alone does not justify aggressive easing, emphasizing that future decisions will hinge on inflation expectations, wage trends, and overall economic stability. The message was clear: policy flexibility remains intact, and further moves will depend strictly on incoming data rather than a preset path.

The Bank framed the current direction as a measured easing cycle, not a sequence of swift cuts. Financial conditions are expected to loosen gradually, but policymakers warned that deeper reductions in 2026 would require careful reassessment. Concerns around persistent wage growth and services inflation continue to limit how far and how fast rates can fall, even as broader activity stays fragile.

Market reaction was subdued. Sterling and the FTSE 100 traded largely flat, reflecting that the move had been widely priced in. In contrast, 10-year UK gilt yields edged slightly higher, suggesting lingering caution around future inflation risks and fiscal dynamics. Positioning continues to favor a slow, controlled easing cycle rather than a sharp policy pivot.

Looking further out, economists note that weak growth projections for late 2025 could justify additional easing if structural pressures persist. Still, the Bank remains closely focused on wage settlements and labor-market signals, which could complicate the disinflation process. For now, the latest cut represents an effort to support a softening economy without losing control of inflation, with the Bank of England’s ongoing attempt to hold that balance steady.

Global markets reflected a mix of economic slowdown signals and tentative geopolitical optimism.

Detail Markets Rebound After Strike Delay (03.24.2026)Markets saw a short-lived recovery after the U.S. delayed planned strikes on Iranian energy infrastructure, easing immediate geopolitical pressure.

Detail Dollar Dominance Deepens (03.23.2026)Global markets remained under pressure as inflation fears tied to the ongoing Iran conflict strengthened the U.S. dollar and reshaped investor positioning.

DetailThen Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!