Exports to the U.S. plunge, highlighting pressure on Europe’s industrial powerhouses.

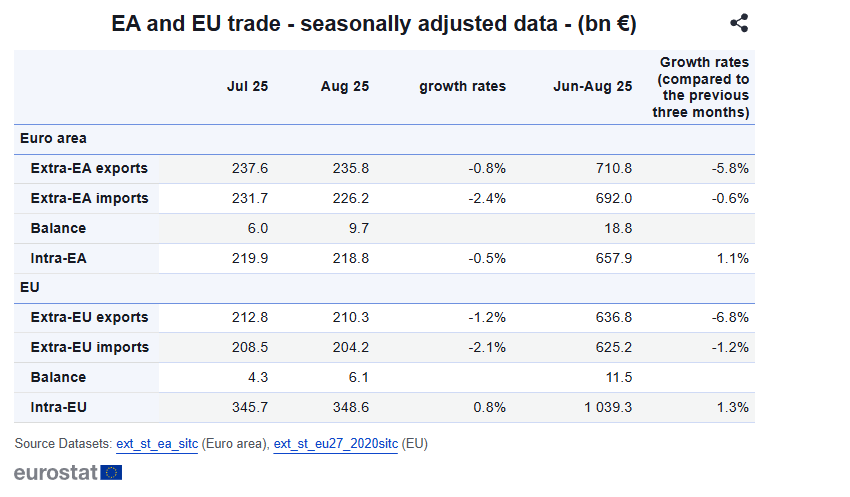

The Eurozone’s trade surplus narrowed sharply in August 2025, slipping to just €1.0 billion from €3.0 billion a year earlier, a sharp miss against market forecasts of €6.9 billion. The weaker performance shows how soft global demand, persistent trade frictions, and sluggish manufacturing activity are weighing on the region’s export-heavy economies.

The data reveal particular strain on key exporters such as Germany and the Netherlands, where slowing international trade is eroding what has long been one of Europe’s primary growth engines.

A sharp deterioration in the Eurozone’s trade surplus with the United States was a major drag on overall performance. The surplus plunged to €5.8 billion from €14.2 billion a year earlier, following a 22.3% collapse in exports.

Officials cited ongoing uncertainty around tariffs and global supply chain shifts as contributing factors. European exporters, especially in the manufacturing and technology sectors, are also facing stiffer competition from U.S. and Asian producers. Imports from the U.S. edged down only 0.6%, underscoring the depth of the export-driven decline.

Total Eurozone exports fell 4.7% year-on-year to €205.9 billion, led by steep declines in chemicals (-9.6%) and machinery and vehicles (-3.9%). Weakness was widespread across major destinations, with shipments to China (-12.8%), Japan (-24.9%), South Korea (-14.2%), and India (-9.8%) all dropping sharply.

Exports to Turkey, Brazil, and the United Kingdom also contracted, pointing to a broad-based slowdown in global industrial demand and waning competitiveness of European goods.

Imports declined 3.8% to €204.9 billion, cushioned by lower purchases of fuels and lubricants (-16.9%) and crude materials (-9.7%). The pullback was supported by energy price normalization and softer domestic demand, with particularly steep declines in imports from Norway, the UK, China, and India.

Although the Eurozone maintained a modest surplus, the sharp contraction highlights growing pressure on its external sector. With global demand weakening and trade policy uncertainty lingering, the region’s export engine, once a vital source of growth, appears to be losing momentum. Economists caution that, unless conditions improve, Europe’s trade balance may continue to erode through the end of the year.

Global markets remained cautious as investors weighed the economic impact of the ongoing Middle East conflict and volatile energy prices.

Currency markets remained volatile as ongoing Middle East tensions continued to shape global sentiment.

") Hormuz Blockade Rattles Markets (09 - 13 March)

Hormuz Blockade Rattles Markets (09 - 13 March)Global sentiment was dominated this week by the second week of the war with Iran and the effective blockade of the Strait of Hormuz, driving Brent crude prices above $100/barrel. Despite a catastrophic US labor report showing a loss of 92,000 jobs in February, safe-haven demand pushed the US Dollar Index to 99.1. The energy shock has ignited fears of "stagflation," particularly in Europe and Japan, as soaring fuel costs threaten to reverse recent disinflationary trends.

DetailThen Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!