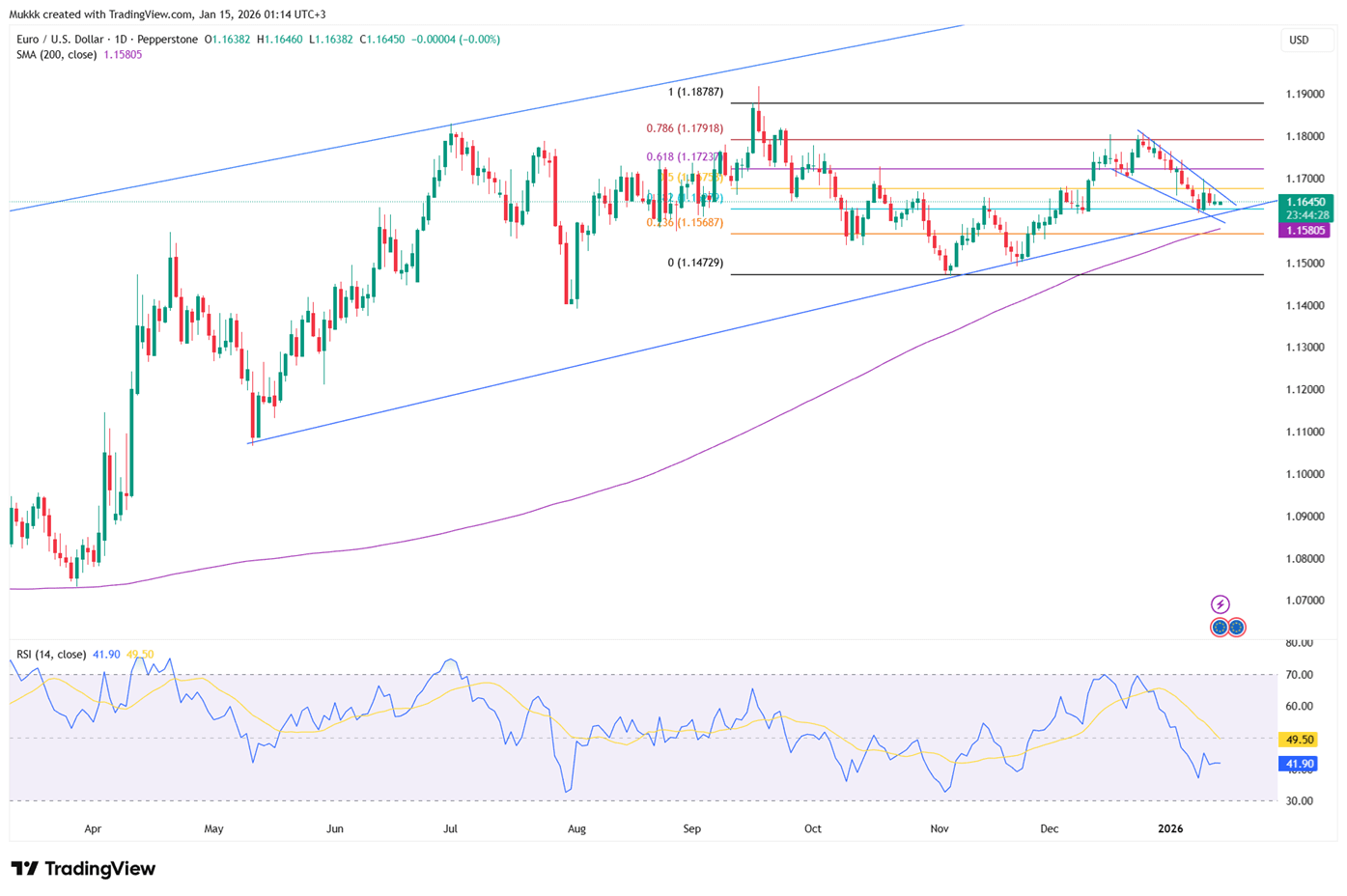

Global markets showed mixed results as geopolitical tensions eased. The euro hovered near a one-month low of $1.165 on cautious Fed expectations, while ECB officials signaled rates will stay on hold.

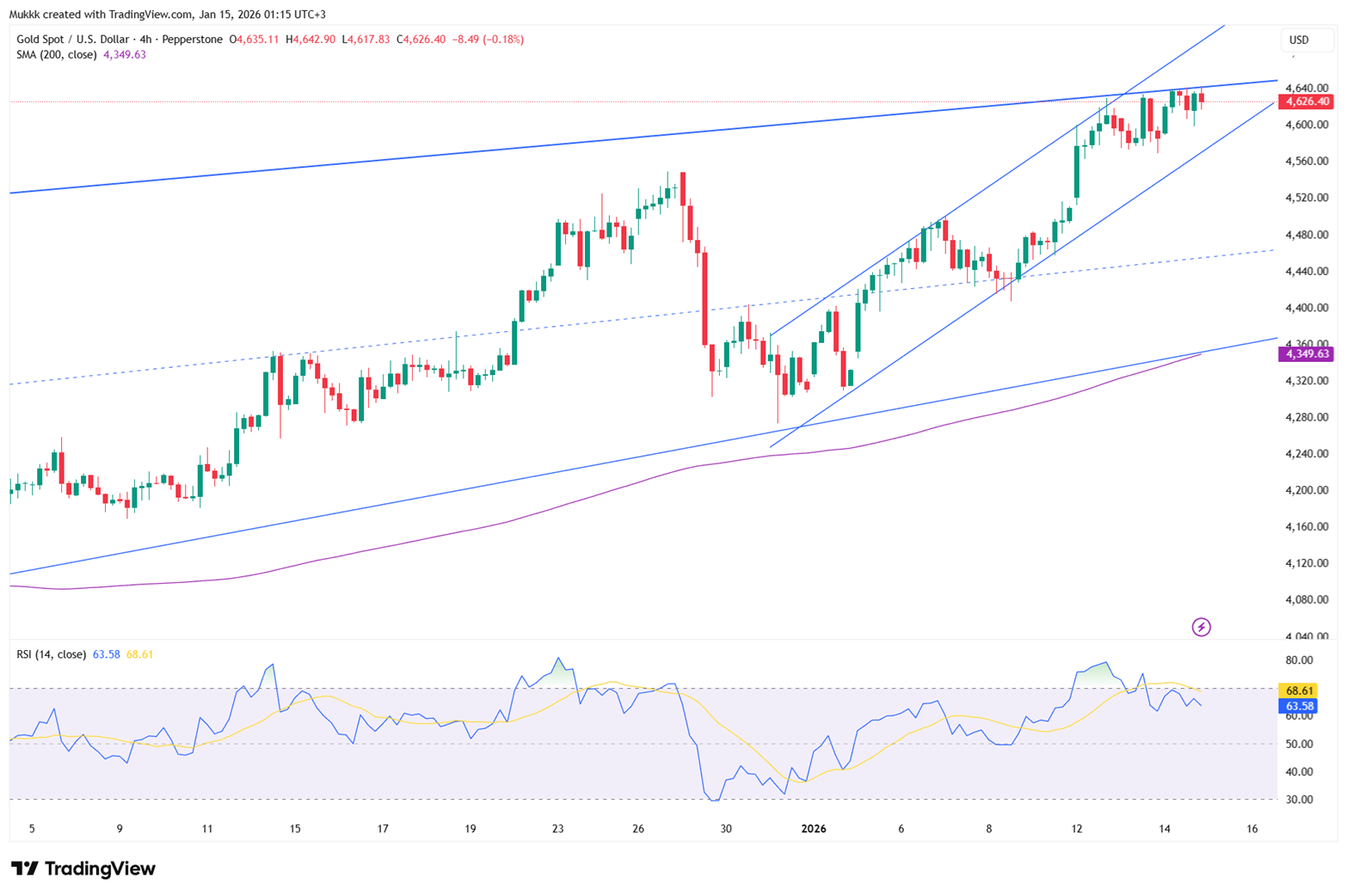

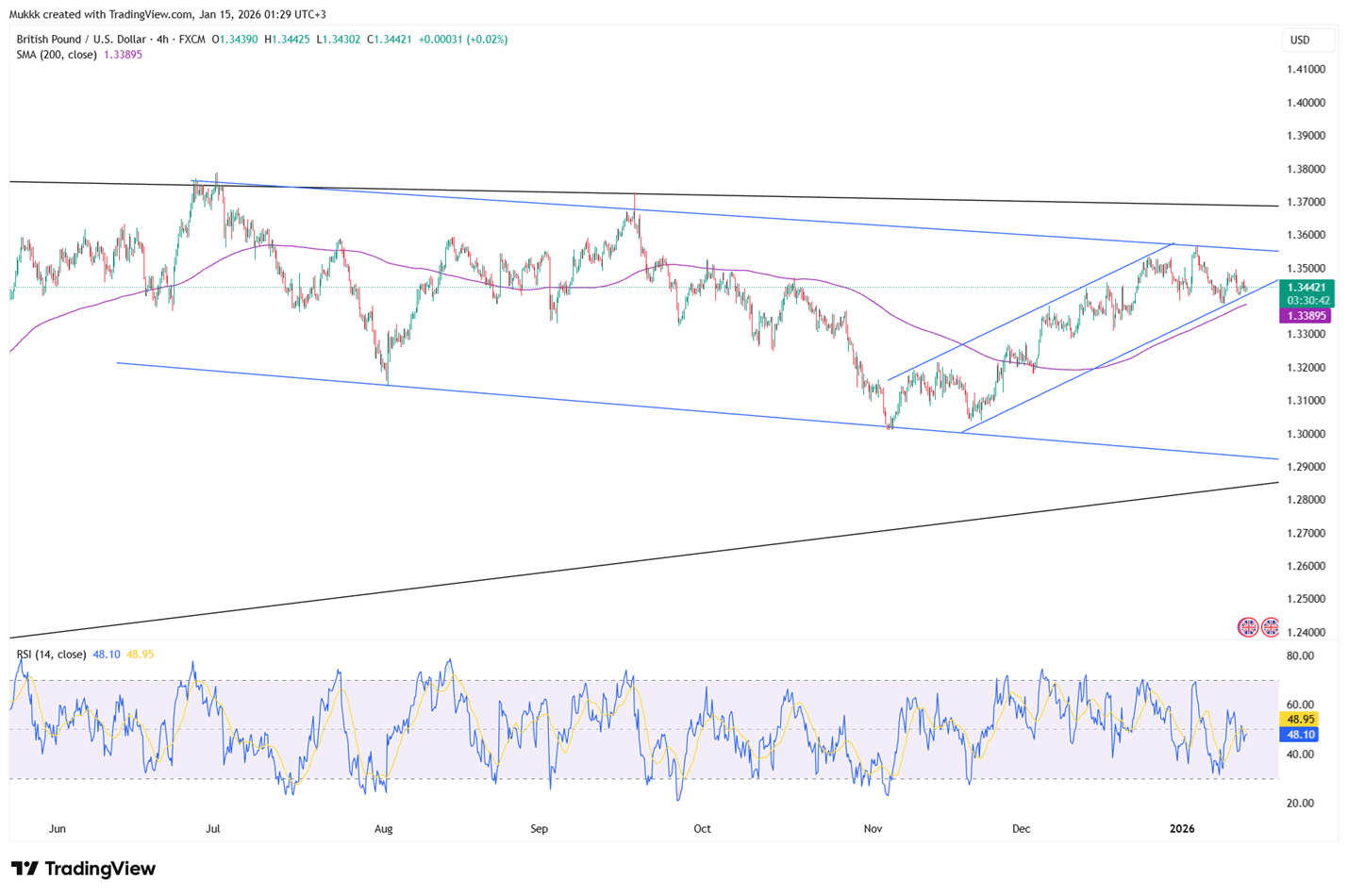

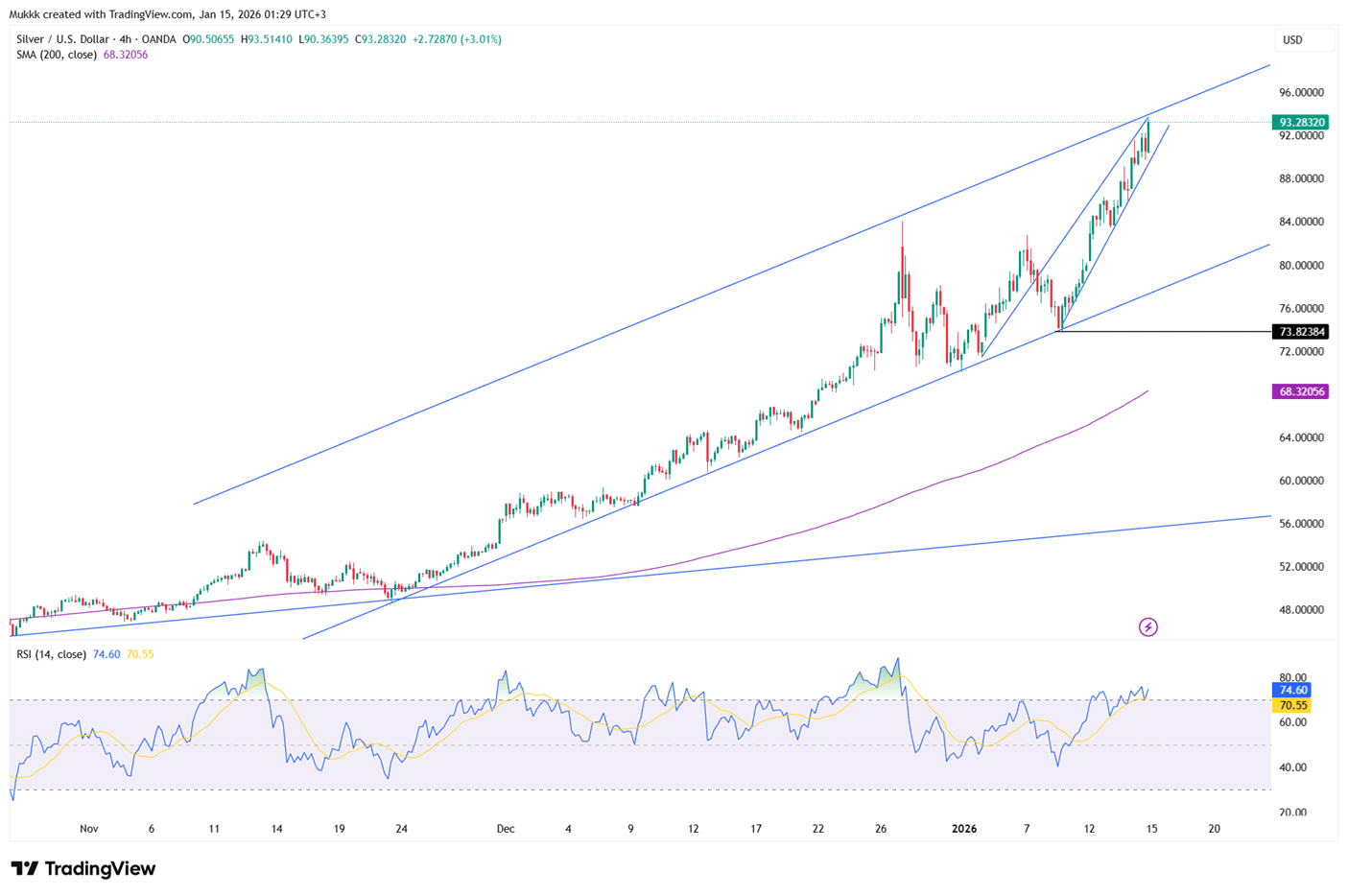

The yen rebounded toward 158 following verbal warnings from Japanese and US officials regarding its weakness. GBP/USD traded sideways near 1.3430 as investors weighed softer UK labor data and upcoming GDP figures. In commodities, gold fell to $4,590 on profit-taking and reduced risk premiums, while silver tumbled 5% below $89 after the US delayed tariffs on critical minerals.

| Time | Cur. | Event | Forecast | Previous |

| 07:00 | GBP | GDP (MoM) (Nov) | 0.1% | 0.1% |

| 13:30 | USD | Philadelphia Fed Manufacturing Index (Jan) | -1.6 | -10.2 |

| 13:30 | USD | Initial Jobless Claims | 215K | 208K |

| 13.45 | USD | S&P Global Manufacturing PMI (Jan) | 52.2 |

The euro hovered near $1.165, remaining close to its one-month low. Investors analyzed U.S. inflation data, where headline CPI held at 2.7% while core inflation cooled to 2.6%. These figures reinforce expectations for potential Fed easing. In the Eurozone, ECB official François Villeroy de Galhau countered talk of rate hikes, suggesting a lengthy period of unchanged policy. This divergence in central bank outlooks continues to exert pressure on the currency pair.

Technically, 1.1610 is the key support, while resistance is seen at 1.1710.

| R1: 1.1710 | S1: 1.1610 |

| R2: 1.1760 | S2: 1.1550 |

| R3: 1.1850 | S3: 1.1500 |

The Japanese yen strengthened toward 158 per dollar on Thursday, rebounding from eighteen-month lows. This recovery follows Finance Minister Satsuki Katayama’s meeting with U.S. Treasury Secretary Scott Bessent, where both expressed deep concern over the yen’s "one-sided" decline. With the currency previously nearing the critical 160 intervention threshold, these high-level discussions have heightened market anticipation of potential direct action to support the yen.

Technically, resistance stands near 158.80, while support is firm at 157.50.

| R1: 158.80 | S1: 157.50 |

| R2: 159.40 | S2: 156.80 |

| R3: 160.00 | S3: 154.70 |

Gold prices settled near $4,590 on Thursday as investors engaged in profit-taking following Wednesday’s record peak. Demand for safe-haven assets dampened after President Trump tempered his rhetoric, noting that the crackdown on Iranian protesters appeared to be subsiding. His comments, suggesting that mass executions are no longer expected, provided a brief reprieve from the intense geopolitical anxiety that had been driving prices higher.

Gold sees support near $4570, while resistance is around $4620.

| R1: 4620 | S1: 4570 |

| R2: 4642 | S2: 4490 |

| R3: 4700 | S3: 4300 |

The GBPUSD pair maintained stability near 1.3430 for a second session during Thursday’s early Asian trade. Investors remain on edge awaiting pivotal monthly GDP figures. Meanwhile, a recent KPMG/REC survey highlighted a sharp decline in hiring at the end of 2025, as rising employment costs and dampened business confidence following the late-November tax hikes continue to restrain recruitment.

From a technical view, support stands near 1.3390, with resistance around 1.3470.

| R1: 1.3470 | S1: 1.3390 |

| R2: 1.3510 | S2: 1.3340 |

| R3: 1.3620 | S3: 1.3290 |

Silver tumbled 5% to below $89 on Thursday, retreating sharply from its recent all-time high. The sell-off intensified after President Trump paused plans for new tariffs on critical mineral imports. Instead, Trump aims to negotiate bilateral deals to secure supplies and mitigate supply chain risks, providing a sudden reprieve from the trade-related fears that had fueled silver’s record rally.

From a technical view, resistance stands near $88.90 while support is located around $85.95.

| R1: 88.90 | S1: 85.95 |

| R2: 90.00 | S2: 84.00 |

| R3: 92.50 | S3: 82.50 |

") Ceasefire Pause Eases Oil and Inflation Fears (27 – 31 July)

Ceasefire Pause Eases Oil and Inflation Fears (27 – 31 July)Global markets began the week on a more positive footing after a pause in US and Iranian military operations reduced immediate concerns over energy supplies and inflation. The United States quietly suspended its nearly two-week strike campaign against Iran late Friday, while Tehran halted retaliatory operations and entered discussions with Oman regarding the Strait of Hormuz. The developments pushed oil prices sharply lower, supporting precious metals and government bonds after weeks of pressure from rising energy costs.

Detail Fed in Focus Amid Easing Tensions (07.27.2026)Global markets began the week on a firmer footing as a pause in U.S.–Iran hostilities eased concerns over energy supplies and inflation.

Higher oil prices lifted inflation expectations, pushing the probability of a September Fed rate hike to 78%.

DetailThen Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!