Japan’s 10-year government bond yield rebounded to 2.28% Tuesday as political uncertainty grew following the start of Prime Minister Sanae Takaichi’s snap election campaign. Her sliding approval ratings and expansionary fiscal goals have pressured the market, while the U.S. 10-year Treasury yield held near 4.22% ahead of a Federal Reserve meeting expected to keep rates steady.

Precious metals witnessed a significant rally, with silver jumping over 6% to surpass $110 and gold climbing above $5,070 amid safe-haven demand. Meanwhile, the dollar index remained at a four-month low of 97, weighed down by concerns over Fed independence and potential political shifts.

| Time | Cur. | Event | Forecast | Previous |

| 18:00 | USD | CB Consumer Confidence (Jan) | 90.1 | 89.1 |

| 22:00 | USD | U.S President Trump Speaks | - | - |

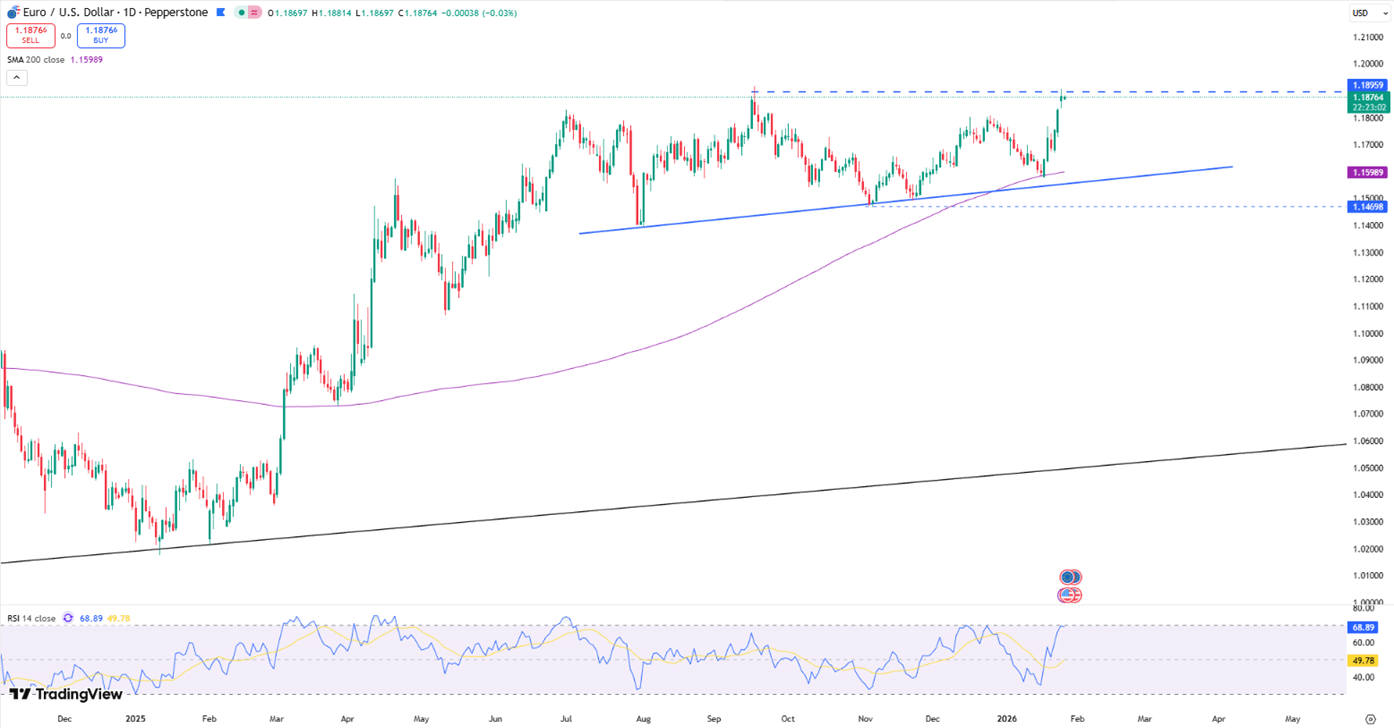

The euro rose toward 1.1880 as the dollar weakened due to fresh trade friction. President Trump’s threat of 100% tariffs on Canada, combined with suspected U.S.–Japan currency intervention, triggered a sharp greenback selloff. EUR/USD recovered from 1.1835 to trade near 1.1900, as investors now pivot to the upcoming FOMC decision and Jerome Powell’s commentary for further policy guidance.

Momentum remains constructive, with 1.1950 in focus on the upside, while 1.1810 defines nearby support.

| R1: 1.1950 | S1: 1.1810 |

| R2: 1.2000 | S2: 1.1760 |

| R3: 1.2050 | S3: 1.1680 |

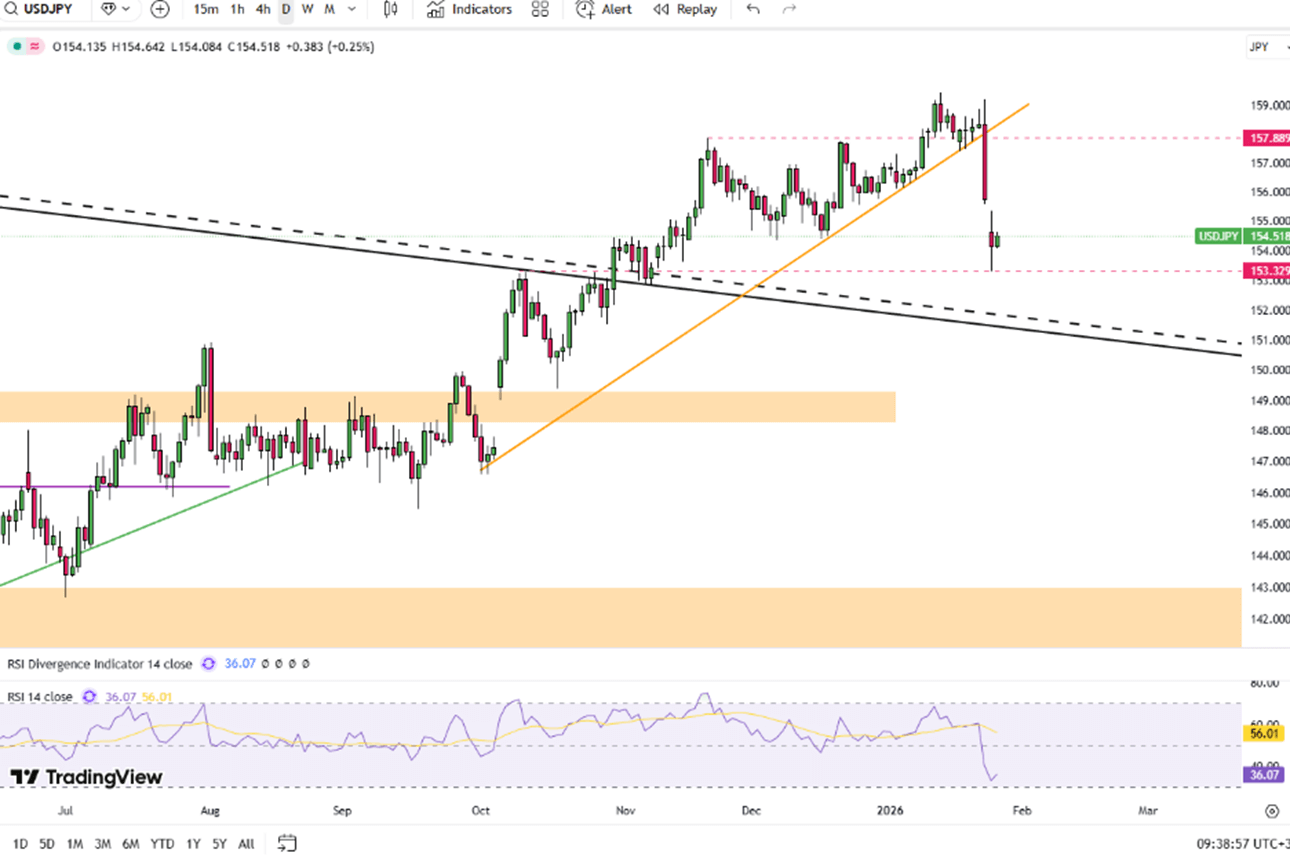

The yen stabilized near 154 per dollar after a massive two-day rally, triggered by speculation of a rare, joint U.S.–Japan market intervention. The move followed reports that the New York Fed conducted "rate checks" with dealers, a tactic often used before official action. While BOJ data suggested the spike was driven by position unwinding rather than direct buying, Japanese officials confirmed they are coordinating closely with Washington. Broader dollar weakness and expectations of a more dovish Federal Reserve leadership further enhanced the yen's recovery.

Technically, resistance stands near 155.10, while support is firm at 153.90.

| R1: 155.10 | S1: 153.90 |

| R2: 156.00 | S2: 153.20 |

| R3: 157.30 | S3: 152.50 |

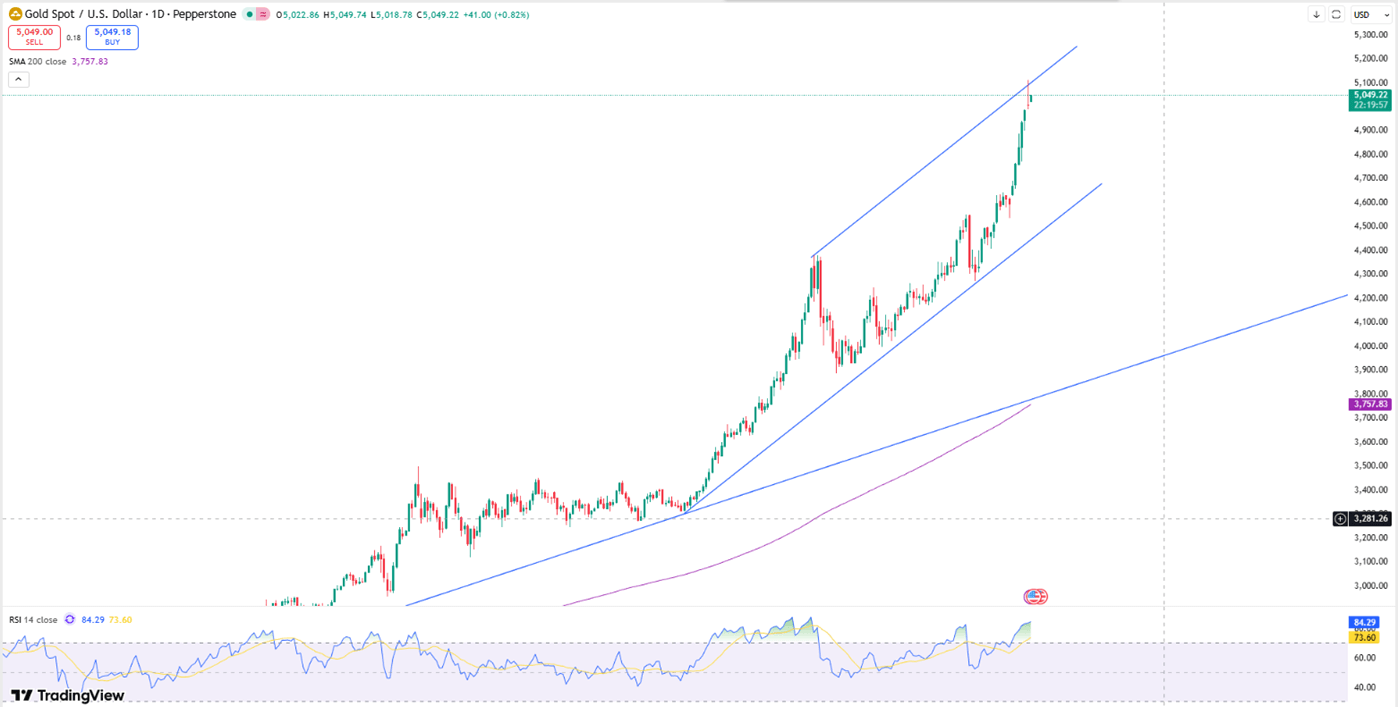

Gold climbed over 1% to roughly $5,070 on Tuesday, after peaking at a record $5,110 in the previous session. Safe haven demand intensified as President Trump threatened to hike tariffs on South Korean autos and pharmaceuticals to 25%, reigniting fears of global trade friction. Markets are now focused on the Federal Reserve meeting, where rates should hold steady. However, bullion remains supported by fiscal concerns, central bank buying, and strong ETF inflows, gaining 17% so far this year.

Gold sees support near $5000, while resistance is around $5090.

| R1: 5090 | S1: 5000 |

| R2: 5140 | S2: 4940 |

| R3: 5200 | S3: 4850 |

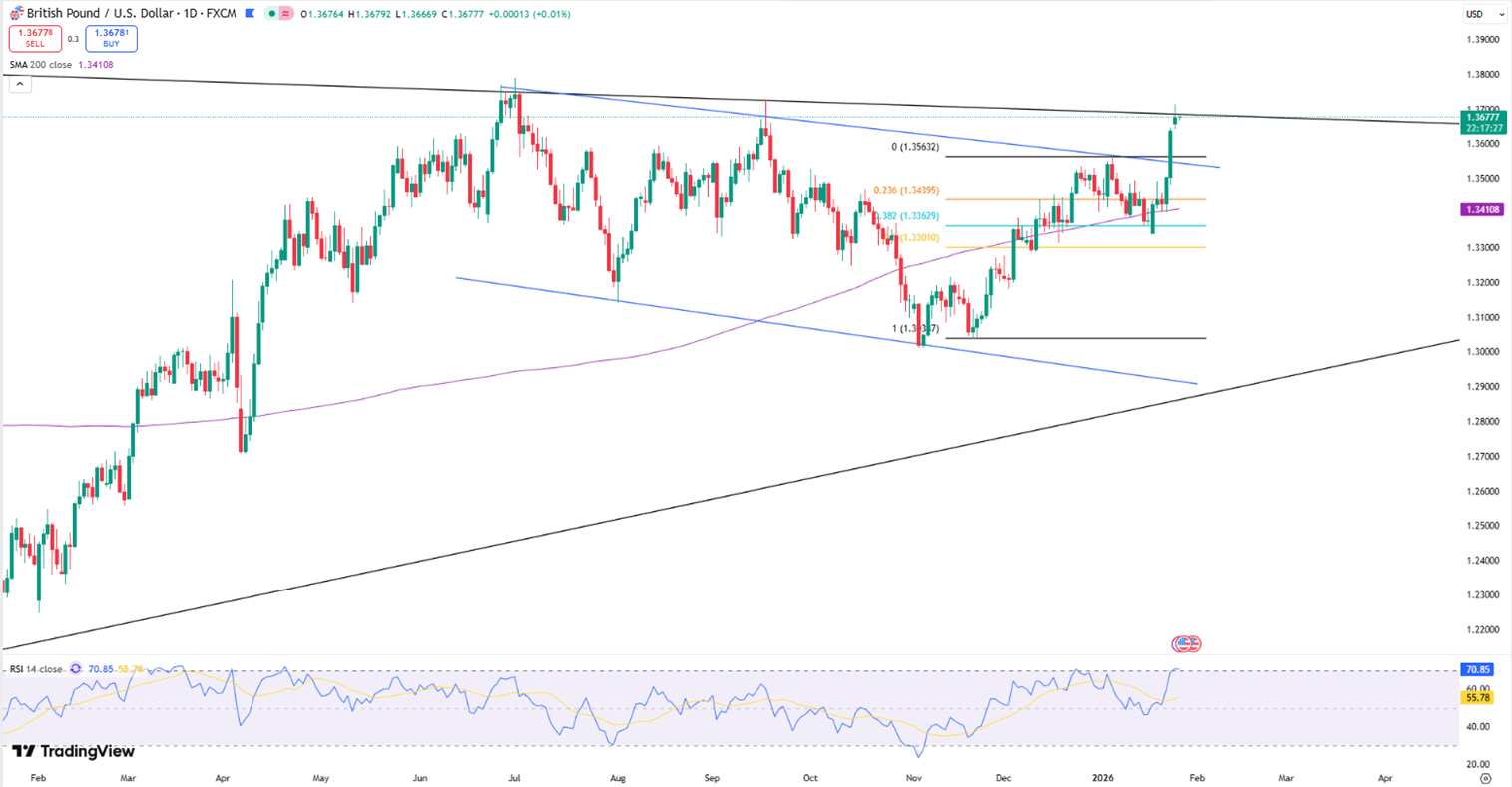

GBP/USD rose at the start of the week, testing 1.3700 for the first time since September. Despite the Trump administration’s threats of new tariffs on European nations over the Greenland dispute, markets largely dismissed the rhetoric as temporary. This resilience in risk appetite, combined with broad dollar softness, helped the pound maintain its upward momentum.

From a technical view, support stands near 1.3620, with resistance around 1.3710.

| R1: 1.3710 | S1: 1.3620 |

| R2: 1.3770 | S2: 1.3580 |

| R3: 1.3850 | S3: 1.3440 |

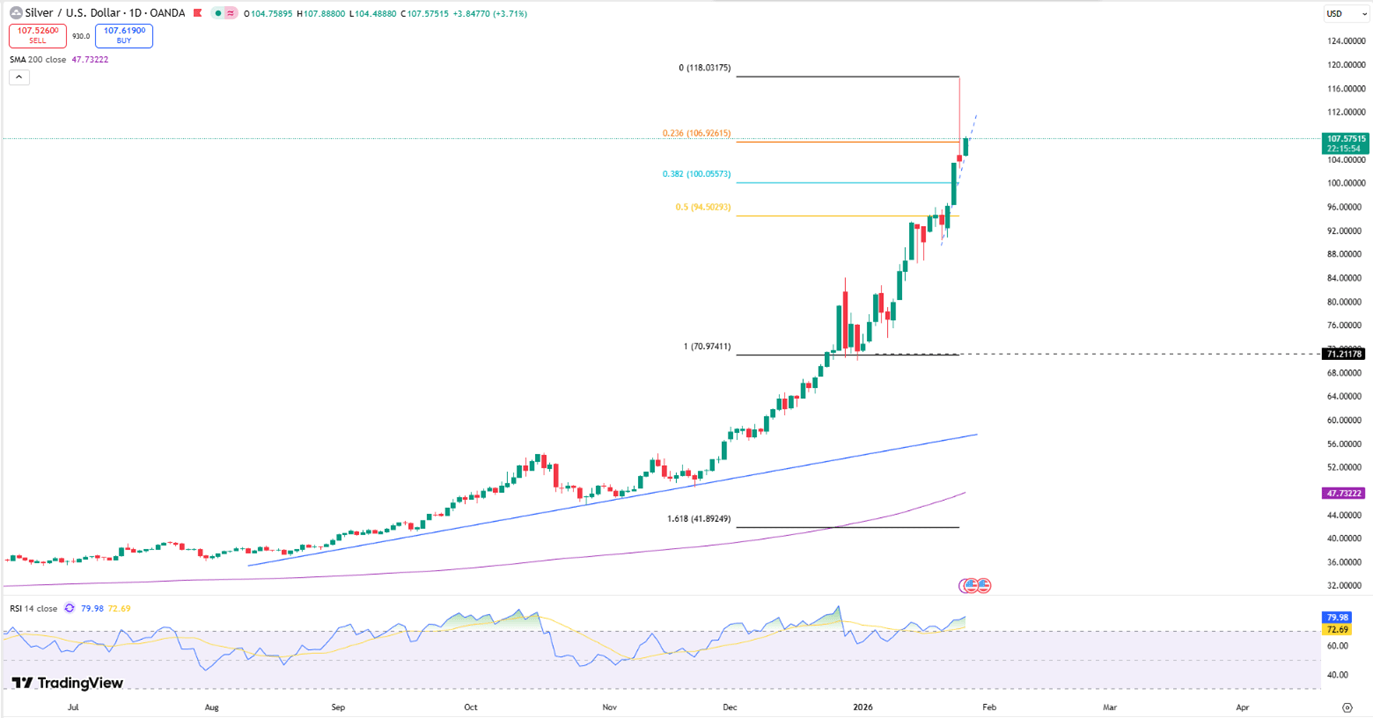

Silver prices surged over 6% on Tuesday, catapulting past $110 per ounce as investors fled traditional bonds and fiat currencies. The historic rally intensified after President Trump threatened to hike tariffs on South Korean autos, lumber, and pharmaceuticals from 15% to 25%, citing legislative delays in Seoul. This renewed trade friction has driven a massive wave of safe haven buying, as capital flows into precious metals to hedge against growing global economic instability and policy uncertainty.

From a technical view, resistance stands near $110, while support is located around $106.80.

| R1: 110.00 | S1: 106.80 |

| R2: 111.60 | S2: 105.00 |

| R3: 113.50 | S3: 102.90 |

Higher oil prices lifted inflation expectations, pushing the probability of a September Fed rate hike to 78%.

Detail Conflict Fuels Inflation Fears (07.23.2026)Middle East tensions lifted Brent crude above $95, a six-week high, on fears of supply disruptions.

Detail The Yen Adds to BOJ Pressure (07.22.2026)Japan's 10-year yield rose to 2.74%, a one-week high, as higher oil prices and a 40-year low in the yen reinforced expectations of further BOJ tightening.

DetailThen Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!