Global markets are navigating a landscape defined by shifting Fed policy expectations and heightened political uncertainty.

While softer U.S. inflation data fuels bets for two rate cuts this year, the dollar remains resilient, pressuring the euro and sterling while pushing the Japanese yen toward the critical 160 level amid snap-election speculation. Meanwhile, gold and silver have surged to record highs, driven by safe-haven demand, rising fiscal debt, and concerns over Fed independence. This combination of geopolitical tension and sensitive policy signals is keeping volatility elevated across all major asset classes.

| Time | Cur. | Event | Forecast | Previous |

| 13:30 | USD | PPI (MoM) (Oct) | 0.3% | |

| 13:30 | USD | Retail Sales (MoM) (Nov) | 0.4% | 0.0% |

| 13:30 | USD | Core Retail Sales (MoM) (Nov) | 0.4% | 0.4% |

| 15:00 | USD | Existing Home Sales (Dec) | 4.21M | 4.13M |

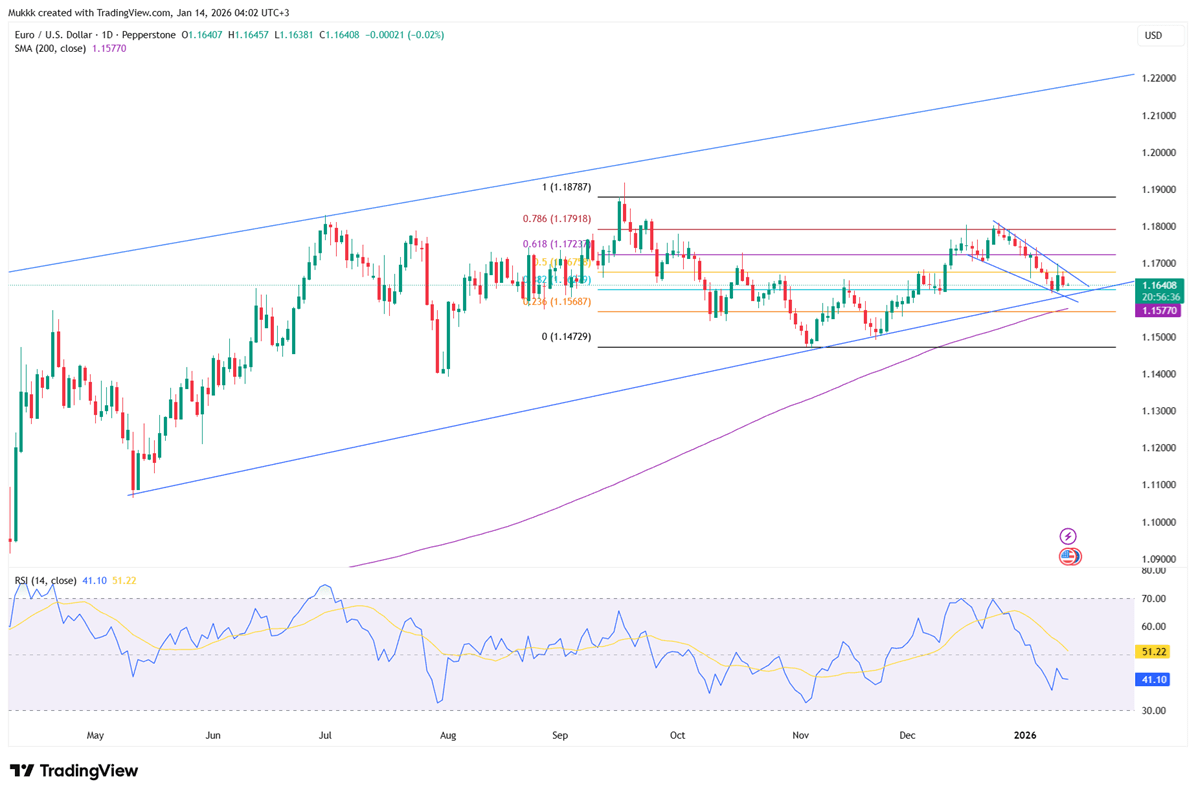

The euro traded near $1.165, hovering close to last week’s one-month low. Market sentiment was shaped by fresh U.S. data showing headline CPI at 2.7% and core inflation cooling to 2.6%. These figures support expectations for Federal Reserve rate cuts later this year. Simultaneously, pressure on the dollar eased as several Republican lawmakers criticized the Justice Department’s investigation into Chair Jerome Powell, reducing immediate fears regarding the central bank’s political independence.

Technically, 1.1610 is the key support, while resistance is seen at 1.1700.

| R1: 1.1700 | S1: 1.1610 |

| R2: 1.1780 | S2: 1.1570 |

| R3: 1.1850 | S3: 1.1500 |

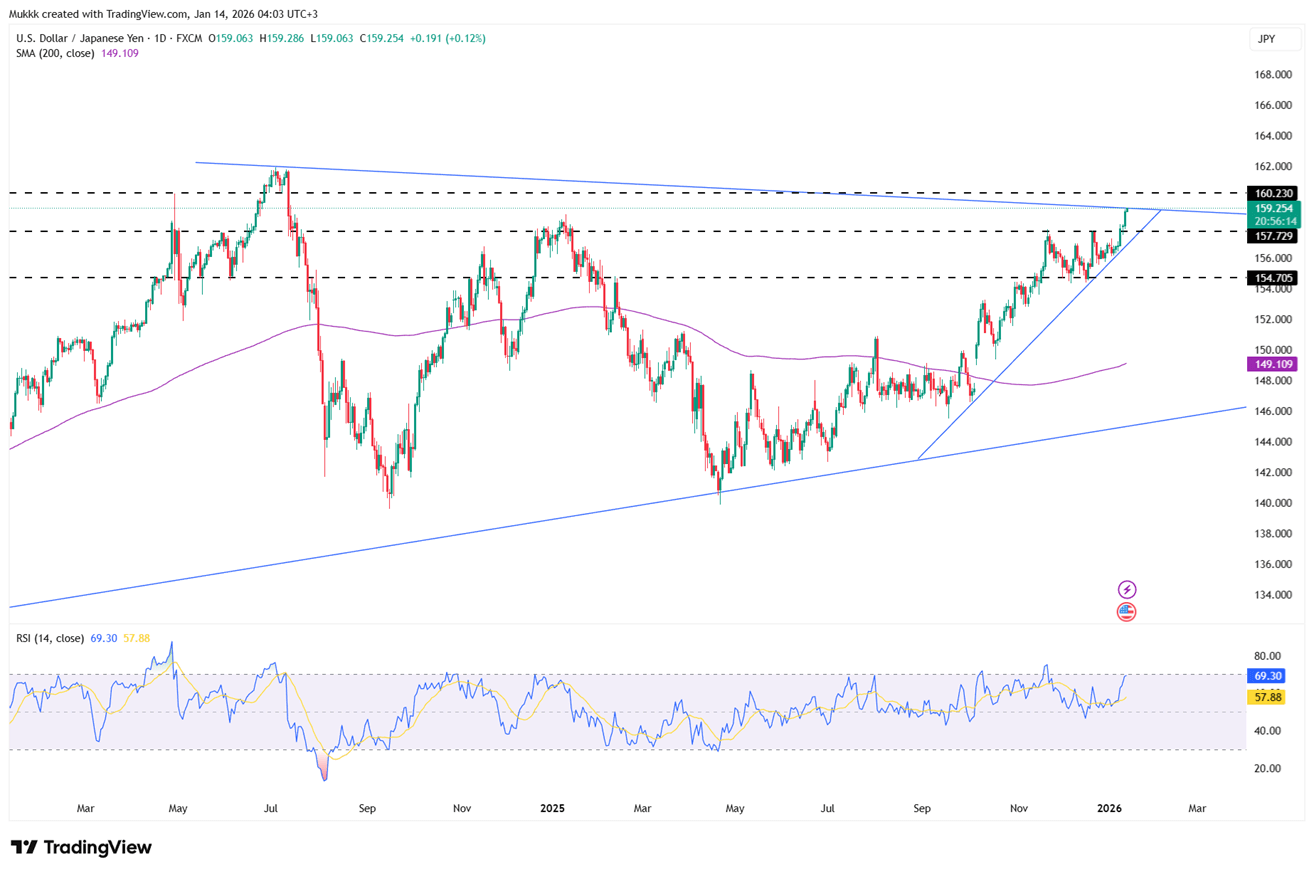

The Japanese yen weakened past 159 against the dollar on Wednesday, hitting its lowest level since July 2024 and edging closer to the 160 mark that has previously triggered official intervention. The decline comes amid political speculation that Prime Minister Sanae Takaichi could call an early election, possibly on February 8, to secure a stronger mandate and advance expansionary fiscal measures.

Technically, resistance stands near 159.70, while support is firm at 158.80.

| R1: 159.70 | S1: 158.80 |

| R2: 160.20 | S2: 157.50 |

| R3: 161.00 | S3: 154.70 |

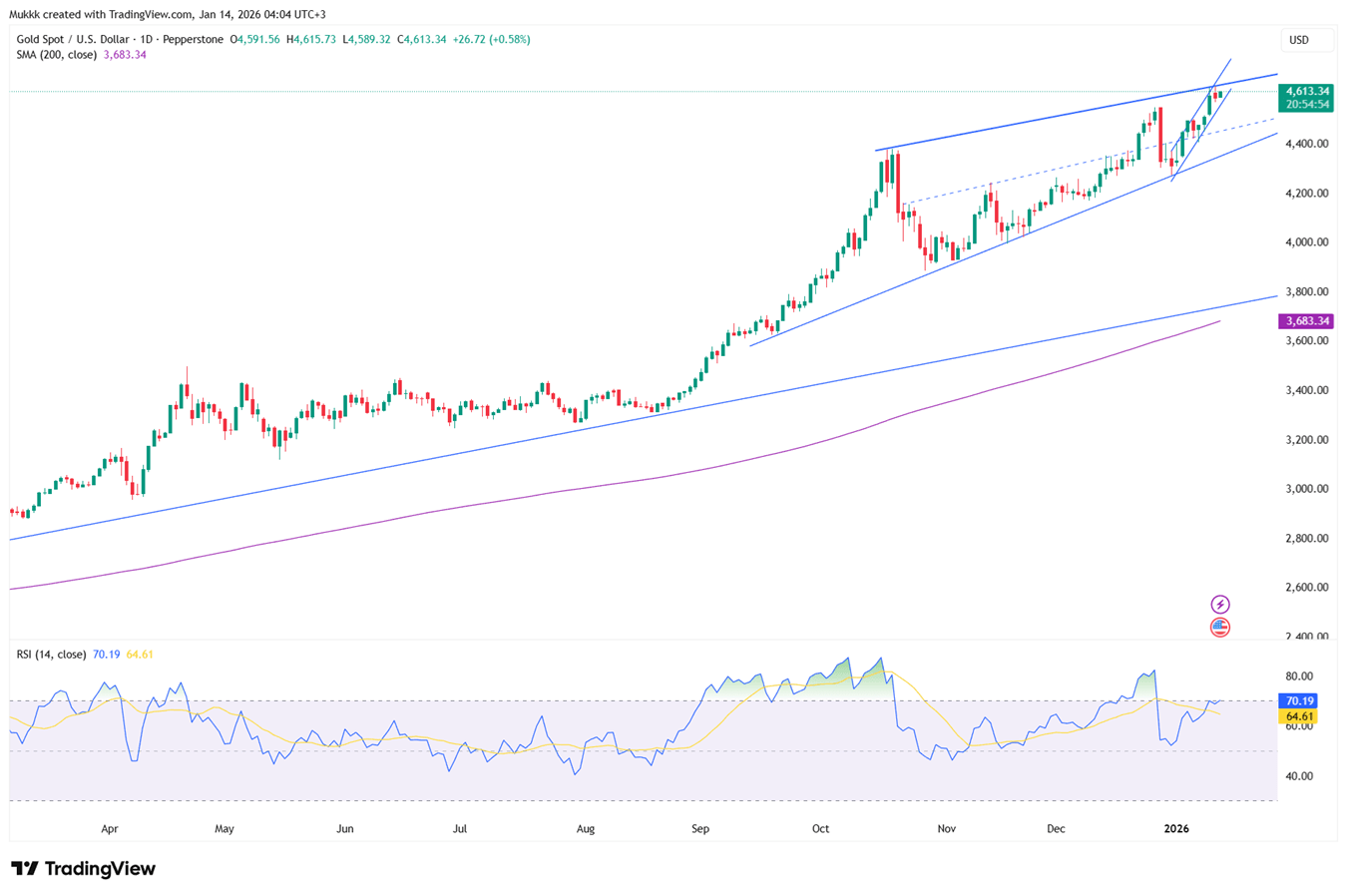

Gold prices surged past $4,630 on Wednesday, reaching a historic peak as cooling U.S. inflation data supported rate-cut expectations. With December’s core inflation easing to 2.6%, investors are increasingly betting on two or three Federal Reserve cuts this year, far exceeding official forecasts. This shift, combined with persistent safe-haven demand amid the ongoing Fed independence dispute and Iranian unrest, continues to drive gold's unprecedented rally.

Gold sees support near $4590, while resistance is around $4650.

| R1: 4650 | S1: 4590 |

| R2: 4685 | S2: 4420 |

| R3: 4720 | S3: 4400 |

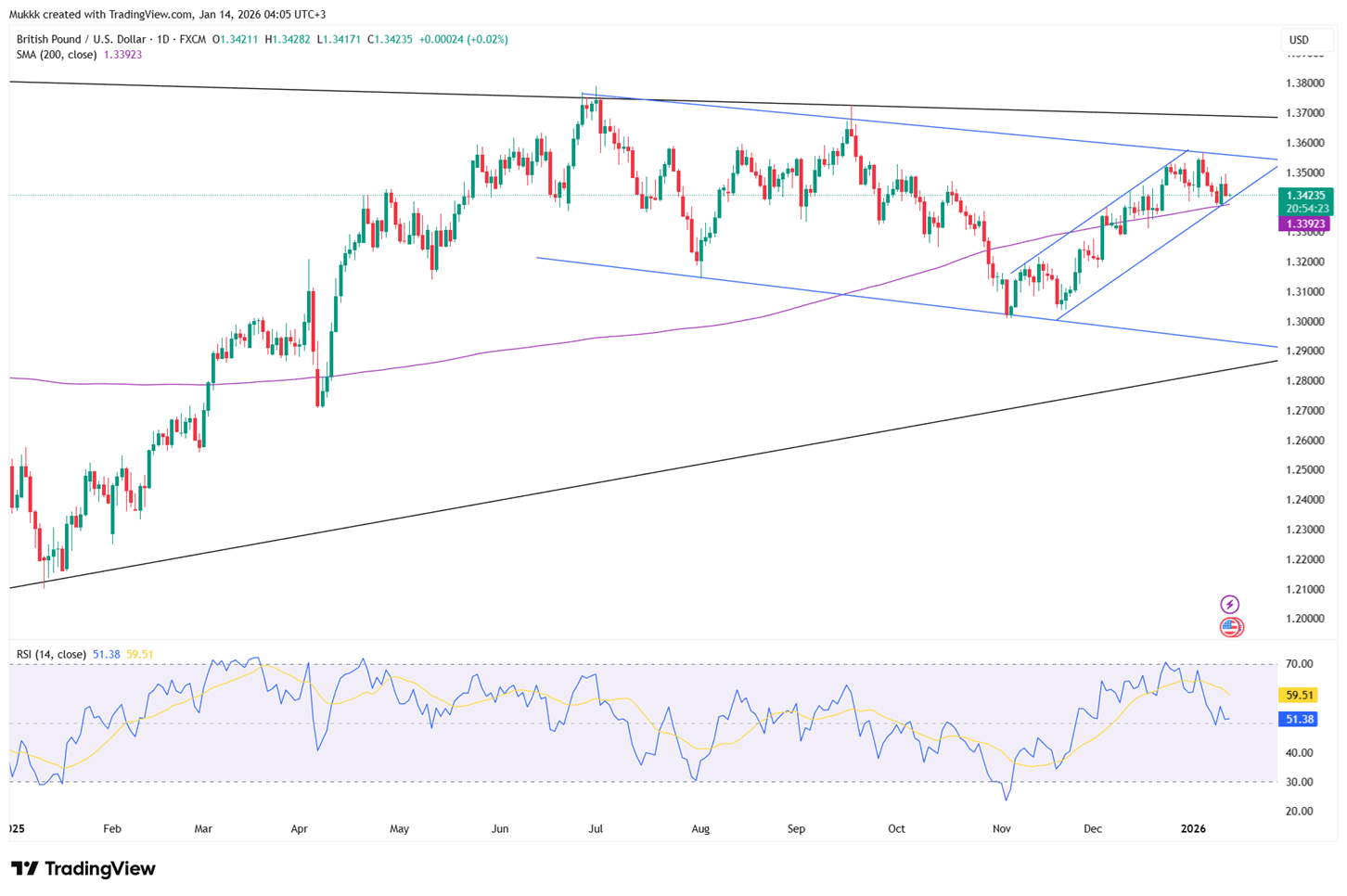

The GBPUSD pair retreated toward 1.3425 during Wednesday's Asian session as the U.S. dollar regained its footing. While December's U.S. inflation held steady at 2.7%, investors are now pivoting toward today's Retail Sales and Producer Price Index (PPI) data for further direction. Despite the slight dip, sterling remains supported by ongoing political clouds surrounding the Federal Reserve.

From a technical view, support stands near 1.3390, with resistance around 1.3470.

| R1: 1.3470 | S1: 1.3390 |

| R2: 1.3510 | S2: 1.3340 |

| R3: 1.3620 | S3: 1.3290 |

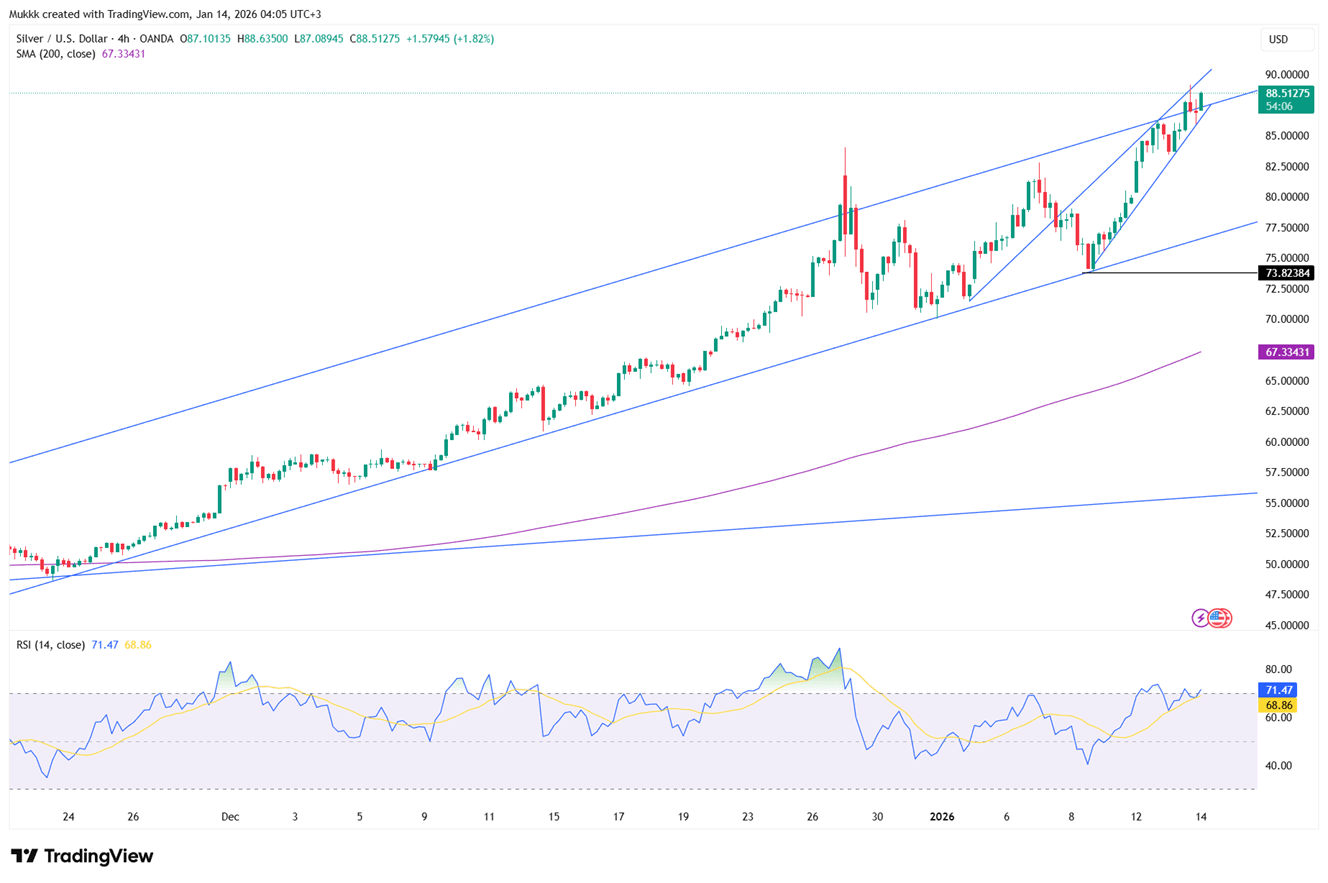

Silver prices exploded past $91 on Wednesday, marking a historic all-time high. This parabolic rally is fueled by intensifying safe-haven demand as investors hedge against escalating Iranian unrest and threats to the Federal Reserve’s independence. Furthermore, December's cooling inflation data has solidified expectations for multiple interest rate cuts this year, significantly increasing the appeal of non-yielding precious metals.

From a technical view, resistance stands near $91.80 while support is located around $89.90.

| R1: 91.80 | S1: 89.90 |

| R2: 93.00 | S2: 88.50 |

| R3: 95.50 | S3: 86.00 |

Higher oil prices lifted inflation expectations, pushing the probability of a September Fed rate hike to 78%.

Detail Conflict Fuels Inflation Fears (07.23.2026)Middle East tensions lifted Brent crude above $95, a six-week high, on fears of supply disruptions.

Detail The Yen Adds to BOJ Pressure (07.22.2026)Japan's 10-year yield rose to 2.74%, a one-week high, as higher oil prices and a 40-year low in the yen reinforced expectations of further BOJ tightening.

DetailThen Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!