Markets began the week on a cautious note, with heightened tensions in the Middle East supporting demand for safe-haven assets such as gold and silver. Investor sentiment remained sensitive amid escalating conflict, particularly following Israel’s strikes on Iran, which have intensified regional uncertainty.

Traders also turned their focus to key monetary policy decisions expected this week. The U.S. Federal Reserve is widely anticipated to keep interest rates steady, although any shift in tone could influence expectations for future rate cuts. Similarly, the Bank of England’s upcoming decision may shape the outlook for the British pound, especially following mixed economic data from the UK.

In Europe, European Central Bank Vice President Luis de Guindos adopted a balanced stance on inflation, suggesting that risks are now evenly distributed and that recent policy signals have been well understood by the markets. His comments helped to stabilize the euro, although it remains under pressure from broader geopolitical developments and diverging central bank paths.

Meanwhile, the U.S. dollar regained strength on the back of safe-haven flows, supported by investor demand amid global uncertainty. Additional support came from expectations surrounding new tariffs and upcoming economic data releases, both of which are contributing to market volatility.

As the week unfolds, investors will remain attentive to geopolitical headlines, central bank commentary, and macroeconomic indicators, all of which are likely to drive price action across major asset classes.

| Time | Cur. | Event | Forecast | Previous |

| 09:00 | EUR | Wages in euro zone (YoY) (Q1) | 4.1% |

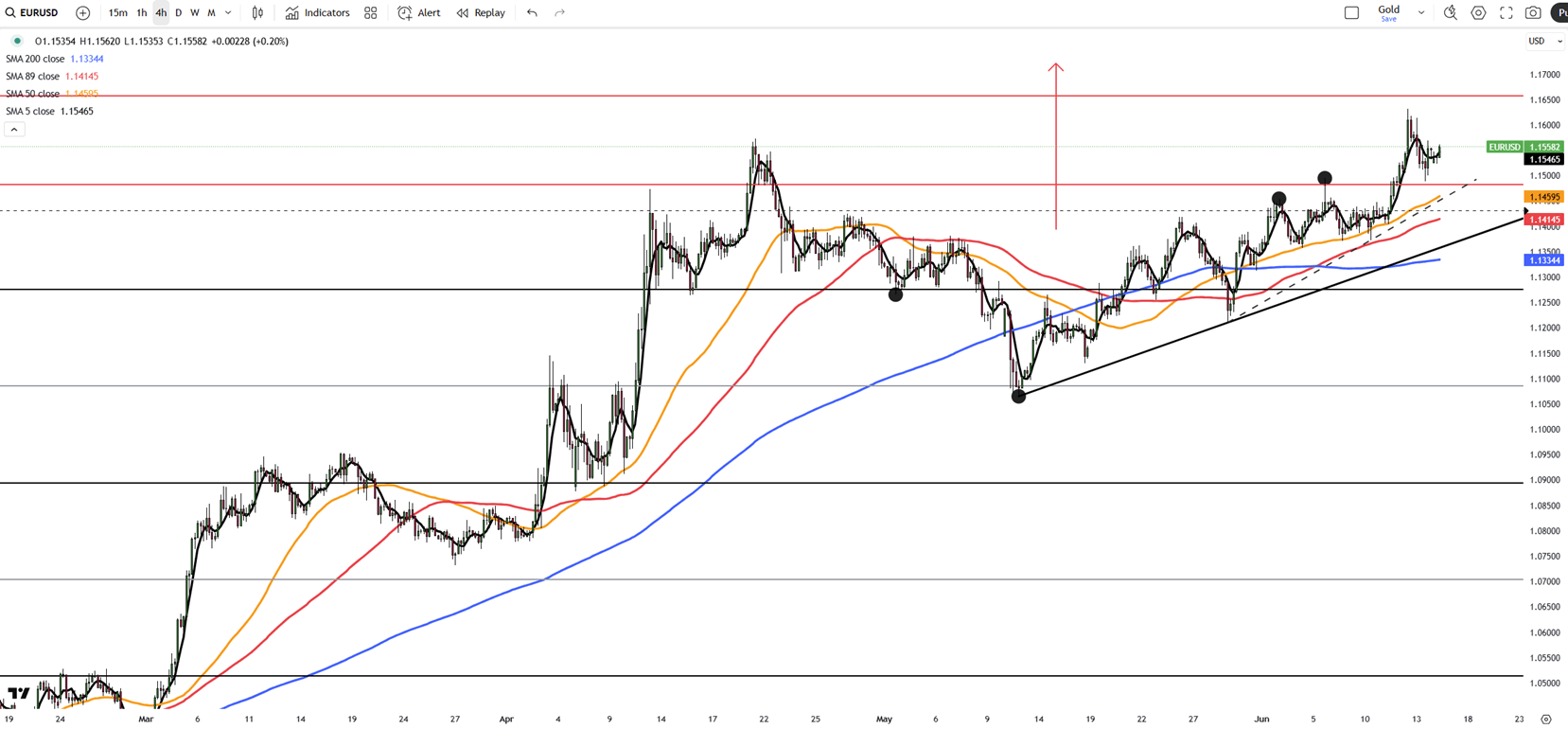

European Central Bank Vice President Luis de Guindos said Monday that the EUR/USD at 1.15 does not hinder the ECB’s inflation goal, noting the euro’s gradual rise and stable volatility.

He stated inflation risks are balanced, with little chance of falling short of the target, and that markets have clearly understood the ECB’s recent policy signals. De Guindos reaffirmed the ECB is close to its inflation objective

Looking ahead, he warned that tariffs could slow growth and inflation in the medium term but expressed confidence in the Fed maintaining swap line arrangements. He also confirmed there have been no discussions about repatriating gold reserves from New York.

At the time, EUR/USD was down 0.09%, trading near 1.1537.

Resistance is located at 1.1580, while support is seen at 1.1460.

| R1: 1.1580 | S1: 1.1460 |

| R2: 1.1660 | S2: 1.1390 |

| R3: 1.1700 | S3: 1.1350 |

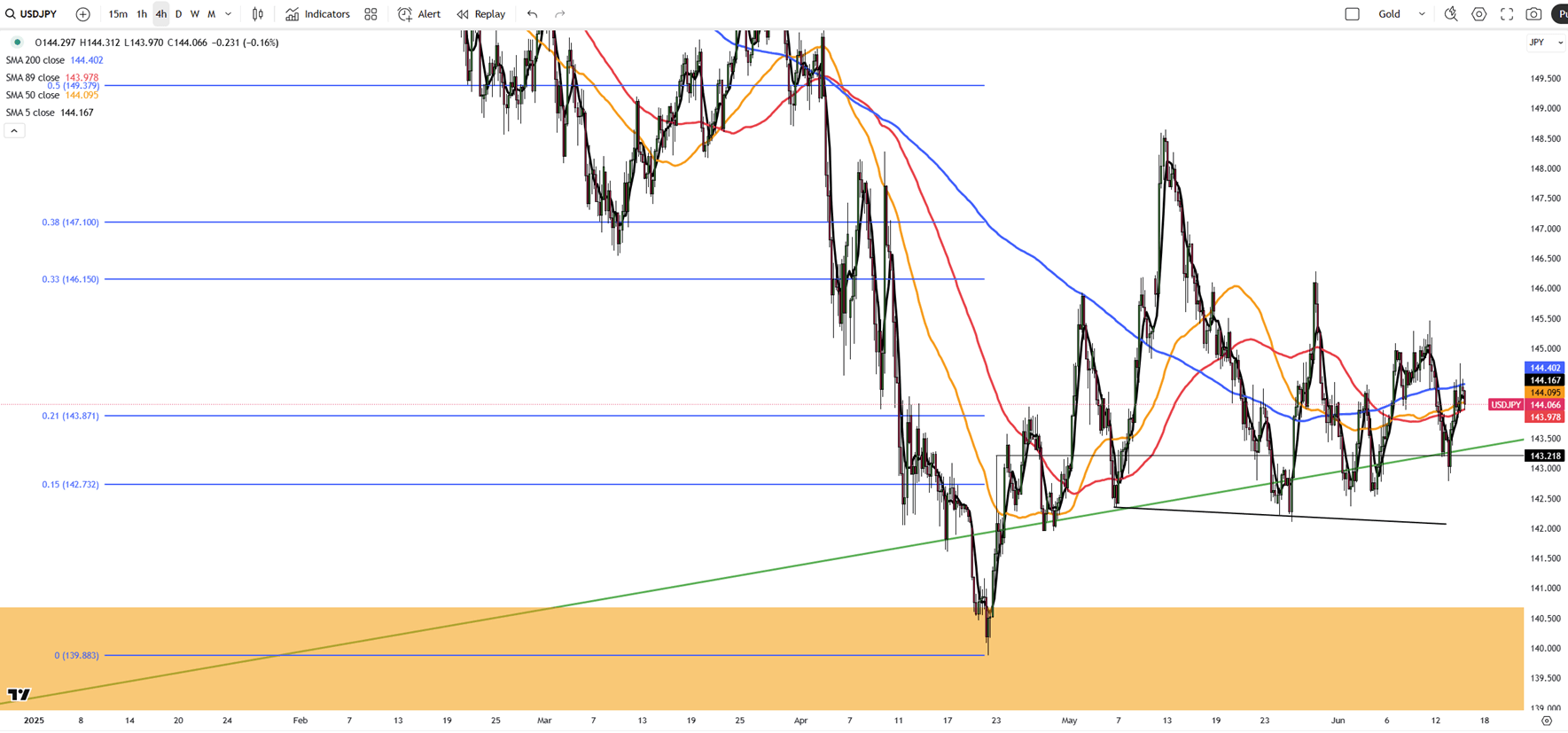

The Japanese yen fell past 144.2 per dollar on Monday, marking a second day of losses, as the U.S. dollar strengthened on increased safe-haven demand. This followed renewed conflict between Israel and Iran, with both sides targeting energy facilities and pushing oil prices higher. The rise in energy costs may reduce the chances of a near-term Fed rate cut as inflation and trade risks persist. Meanwhile, focus turns to the Bank of Japan’s upcoming policy meeting, where it is expected to keep rates unchanged while assessing the inflation impact of rising oil prices amid global uncertainty.

Resistance is at 145.30, while support stands near 142.50.

| R1: 145.30 | S1: 142.50 |

| R2: 146.10 | S2: 142.10 |

| R3: 148.15 | S3: 141.50 |

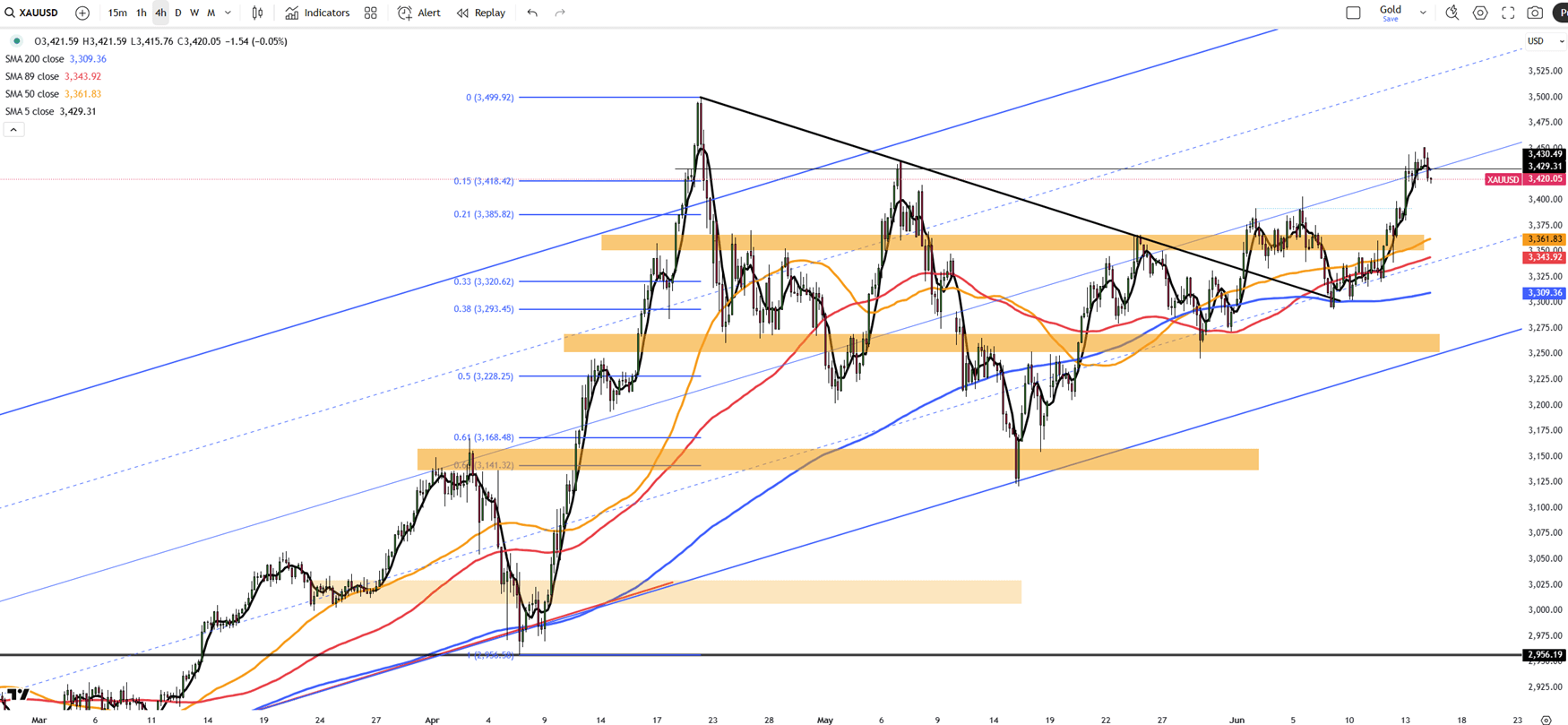

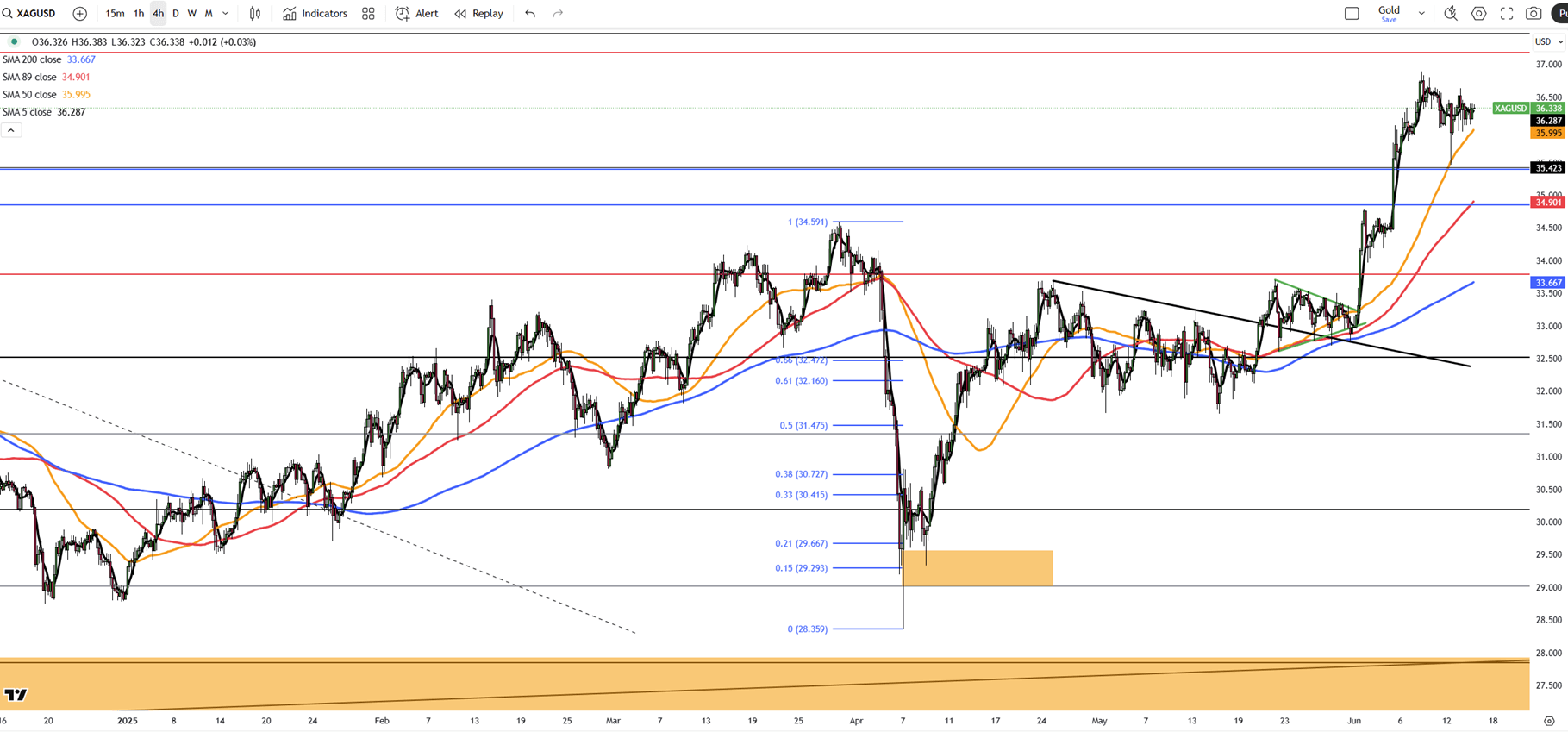

Gold rose to around $3,440 per ounce on Monday, staying near April’s record highs, as escalating Middle East tensions increased safe-haven demand. Weekend clashes between Israel and Iran raised fears of broader conflict.

Markets now look ahead to upcoming central bank meetings, especially the U.S. Federal Reserve. While rates are expected to remain unchanged, investors are watching for signals on future cuts. Last week’s weaker inflation data has increased expectations for a potential rate cut by September.

Traders are also awaiting details on President Donald Trump’s upcoming tariff decisions, expected in the coming weeks.

Resistance is seen at $3,430, while support holds at $3,392.

| R1: 3430 | S1: 3392 |

| R2: 3500 | S2: 3340 |

| R3: 3600 | S3: 3310 |

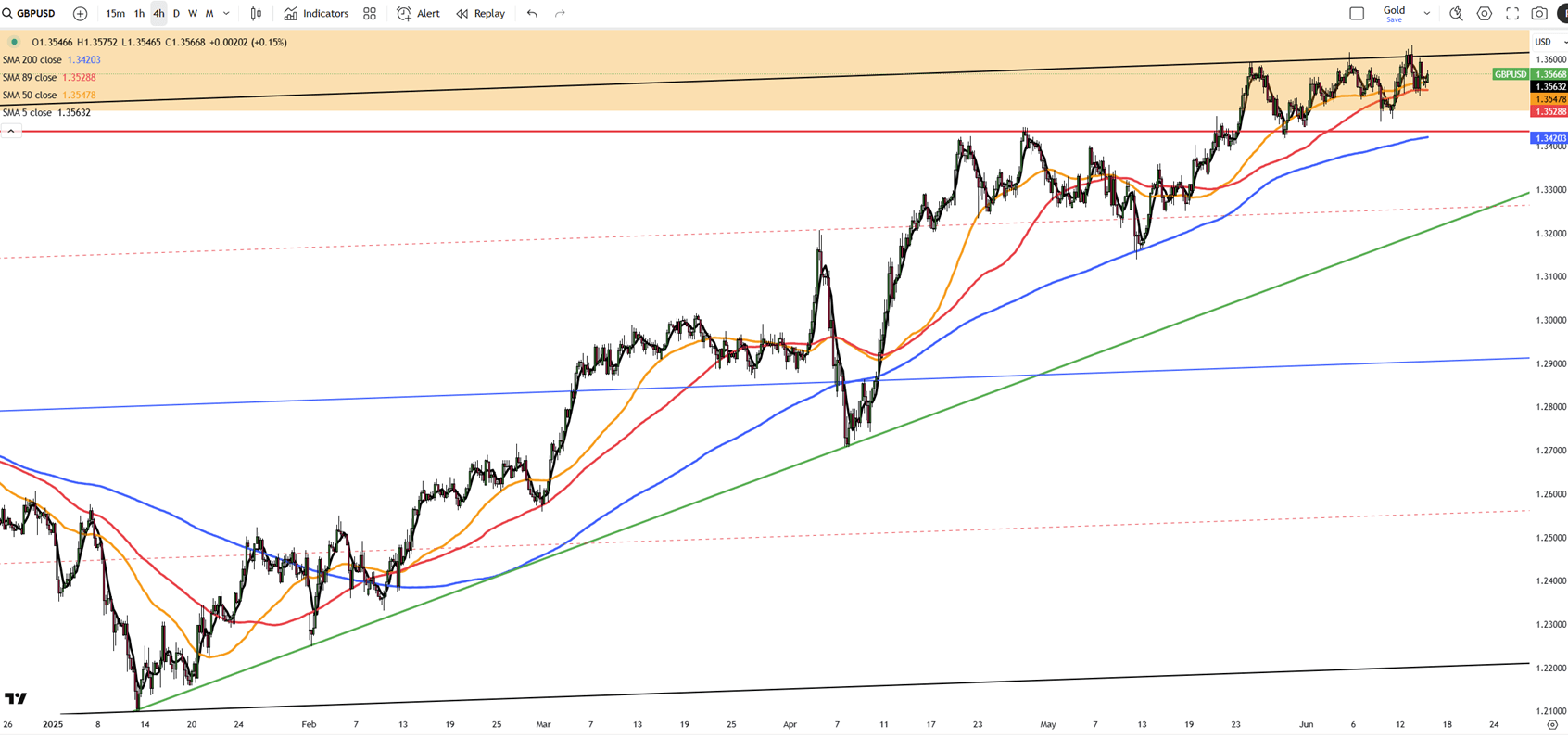

GBP/USD remains below Friday’s three-year high, trading around the mid-1.3500s in a narrow range during Monday’s Asian session. The pair shows limited downside as traders await a busy week of key data and central bank decisions.

Markets are watching the UK CPI on Wednesday and the Bank of England’s policy announcement on Thursday, both crucial for the Pound. The US Federal Reserve will also decide on rates Wednesday, likely guiding the dollar’s short-term path.

Friday’s UK GDP showed a 0.3% contraction in April, increasing bets on faster BoE rate cuts. The USD is supported by safe-haven flows due to Middle East tensions, though soft US inflation data has raised expectations for Fed cuts by September. A broadly positive global risk mood is offering some support to GBP/USD.

Resistance is at 1.3600, with support around 1.3425.

| R1: 1.3600 | S1: 1.3425 |

| R2: 1.3750 | S2: 1.3165 |

| R3: 1.3850 | S3: 1.2890 |

Friday’s strong U.S. data may support the dollar, as the University of Michigan’s Consumer Sentiment Index rose to 60.5 in June from 52.2, beating forecasts of 53.5 and marking the first gain in six months.

Geopolitical tensions continue to drive safe-haven demand, especially for silver. Israel struck Iranian nuclear and missile sites Friday, killing military officials. On Sunday, Iran began its fourth phase of response, warning of firm retaliation to further Israeli actions.

Markets now turn to Wednesday’s Fed meeting. While rates are expected to stay unchanged, futures still price in two cuts this year, possibly starting in September, supported by last week’s soft inflation data.

Resistance is set at 36.90, while support stands at 35.40.

| R1: 36.90 | S1: 35.40 |

| R2: 37.20 | S2: 34.85 |

| R3: 37.50 | S3: 33.80 |

Markets remained cautious as a stronger U.S. dollar pressured major currency pairs ahead of key central bank decisions.

") Strong USD and Surging Oil Amid Tensions (16–20 March)

Strong USD and Surging Oil Amid Tensions (16–20 March)Global markets faced significant upward pressure on yields and energy prices this week as the conflict in the Middle East entered its third week. The US Dollar Index surged above 100.3, its highest since May 2025, fueled by safe-haven flows and Defense Secretary Pete Hegseth's announcement of the largest planned strike wave against Iran to date. Brent crude breached the $105 threshold following strikes on Kharg Island and warnings that 90% of Iran’s export facilities could be targeted.

Detail Markets Brace for Central Bank Week (03.16.2026)Global markets remain dominated by geopolitical tensions and energy risks as the conflict in the Middle East continues to shape investor sentiment.

Then Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!