The eurozone economy continued to expand in February, but the growth rate remained the same as January levels, leading to only slight overall progress.

According to HCOB PMI survey data, the recovery remained fragile due to weak demand conditions, with new business volumes continuing to decline. Business confidence also saw a slight dip, and workforce numbers fell for the seventh month.

Inflationary pressures intensified across the euro area, with input costs rising at the fastest pace in nearly two years. In response, companies raised their prices at the sharpest rate since April 2024.

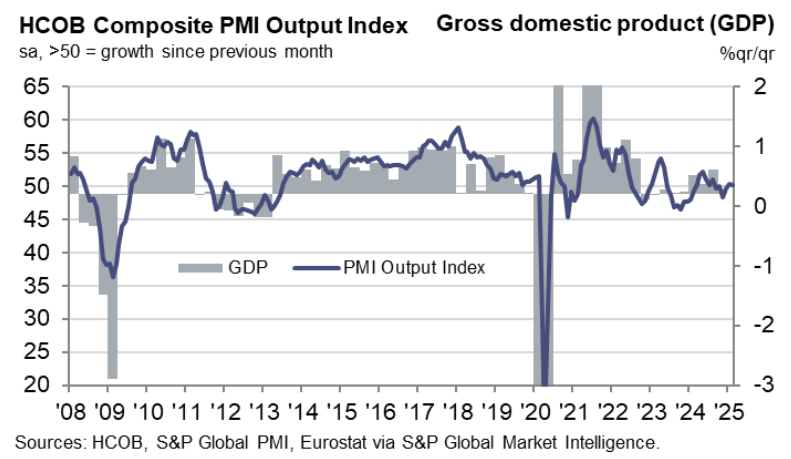

The HCOB Eurozone Composite PMI Output Index, which combines Manufacturing and Services PMI, remained steady at 50.2 in February, just above the neutral 50.0 mark. While this signaled economic growth, it remained marginal and significantly below the long-term average of 52.4.

Several eurozone economies contributed to this modest growth:

Despite the overall increase in output, new orders continued to decline, with demand for goods and services falling at a slightly faster rate than in January. Both manufacturers and service providers reported weaker inflows of new work, and export markets failed to provide support, as international business continued to shrink.

The eurozone has now seen nearly two years of backlog reductions, though the pace of decline slowed compared to the long-term trend. Businesses continued clearing outstanding orders at modest rates.

Workforce capacity was also further reduced in February, marking seven consecutive months of job cuts. While the decline in employment remained relatively mild, it was the fastest rate since December 2020. The job reductions were primarily seen in the manufacturing sector, while service businesses continued hiring.

Despite ongoing challenges, eurozone companies remained generally optimistic about their 12-month outlook. However, growth expectations slipped slightly compared to January and were below the long-term average. Business sentiment was also weaker compared to the 2024 trend.

Regarding pricing, input costs surged in early 2024, with inflation reaching its highest level since April 2023. Companies became more aggressive with their pricing strategies, with the service sector driving inflation across the eurozone.

Source: Hamburg Commercial Bank AG & SP Global

Global markets remained under pressure as growing expectations of additional Federal Reserve rate hikes supported the U.S. dollar and weighed on major currencies and precious metals.

Global markets remained under pressure on Tuesday as expectations for tighter Federal Reserve policy outweighed optimism surrounding progress in U.S.–Iran negotiations.

") Fed and Iran Uncertainty Keep Markets on Edge (22-26 June)

Fed and Iran Uncertainty Keep Markets on Edge (22-26 June)Global financial markets faced a turbulent cross-current this week as sharp shifts in the US–Iran diplomatic track collided with hawkish monetary policy signals.

DetailThen Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!