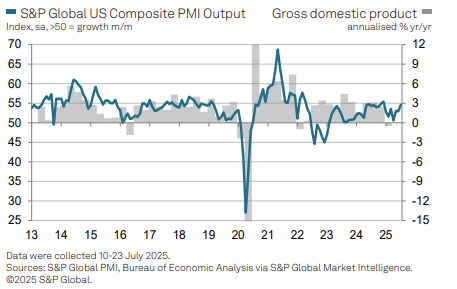

In July, the US economy maintained its expansion, signaling a solid start to the third quarter.

The S&P Global Flash US Composite PMI Output Index climbed to 54.6, the highest reading in seven months, driven mainly by a surge in services activity. The Services PMI rose to 55.2, reflecting strong domestic demand. In contrast, manufacturing momentum weakened, with the Manufacturing PMI falling to 49.5, also a seven-month low, as output growth slowed.

This widening divergence emphasizes the resilience of the services sector, while factories struggle with rising input costs and tariff-related disruptions.

Despite the headline expansion, input cost inflation accelerated once again, especially in manufacturing. Nearly two-thirds of producers cited tariffs as the primary driver of cost increases. Services providers also reported steep price hikes, making July one of the hottest inflation months in recent years. As a result, output prices rose across both sectors, compounding concerns over profit margins and consumer affordability.

Business optimism dipped for the second straight month, hitting its second-lowest level in over two years. Although firms remain mildly upbeat about future output, worries are growing over the impact of federal spending cuts and escalating tariffs. Many survey participants flagged policy instability as a major source of uncertainty, raising concerns about the sustainability of private sector momentum.

Employment increased overall, largely driven by the services sector, where backlogs of work hit their highest level since mid-2022. However, in manufacturing, companies began cutting payrolls as orders and backlogs declined. This contrast highlights how the labor market is starting to reflect the sectoral imbalance in growth.

Following two months of stockpiling ahead of expected tariff hikes, manufacturers scaled back inventories in July. This move helped ease pressure on supply chains and shorten delivery times, offering some relief after months of buildup.

While July brought continued economic growth, the underlying tone was more cautious. Tariffs and fiscal tightening appear to be weighing on confidence and forward planning. Unless these headwinds ease, businesses may remain hesitant to invest or expand, potentially slowing the momentum gained at the start of Q3.

Source: S&P Global

Russia-Ukraine peace efforts remain stalled.

Detail Trump Pressures Fed as Dollar Slips After Cut (12.11.2025)The Federal Reserve ended 2025 with a 25-bps cut to 3.50-3.75%, maintaining guidance for one cut in 2026.

Detail Fed Day Takes Shape, Chair Decision Nears (12.10.2025)Income strategies are under pressure as lower yields reduce the appeal of short-term Treasuries, pushing investors toward riskier segments such as high yield, emerging-market debt, private credit, and catastrophe bonds.

DetailThen Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!