Markets ended the week focused on central bank policy and geopolitical developments as the ECB delivered its expected rate hike while investors assessed the outlook for further tightening.

The euro briefly rallied before giving back gains, while the dollar remained supported by safe-haven demand linked to ongoing Middle East tensions. Precious metals stabilized after recent volatility as hopes for a potential U.S.–Iran agreement improved sentiment, though elevated inflation and expectations for restrictive monetary policy continued to shape market direction. Attention now shifts to next week’s Bank of Japan meeting and developments in the Middle East.

| Time | Cur. | Event | Forecast | Previous |

| All Day | RUB | Russia – Russia Day | ||

| 09:00 | EUR | German CPI (MoM) (May) | -0.2% | 0.6% |

| 09:00 | GBP | GDP (MoM) (Apr) | -0.1% | 0.3% |

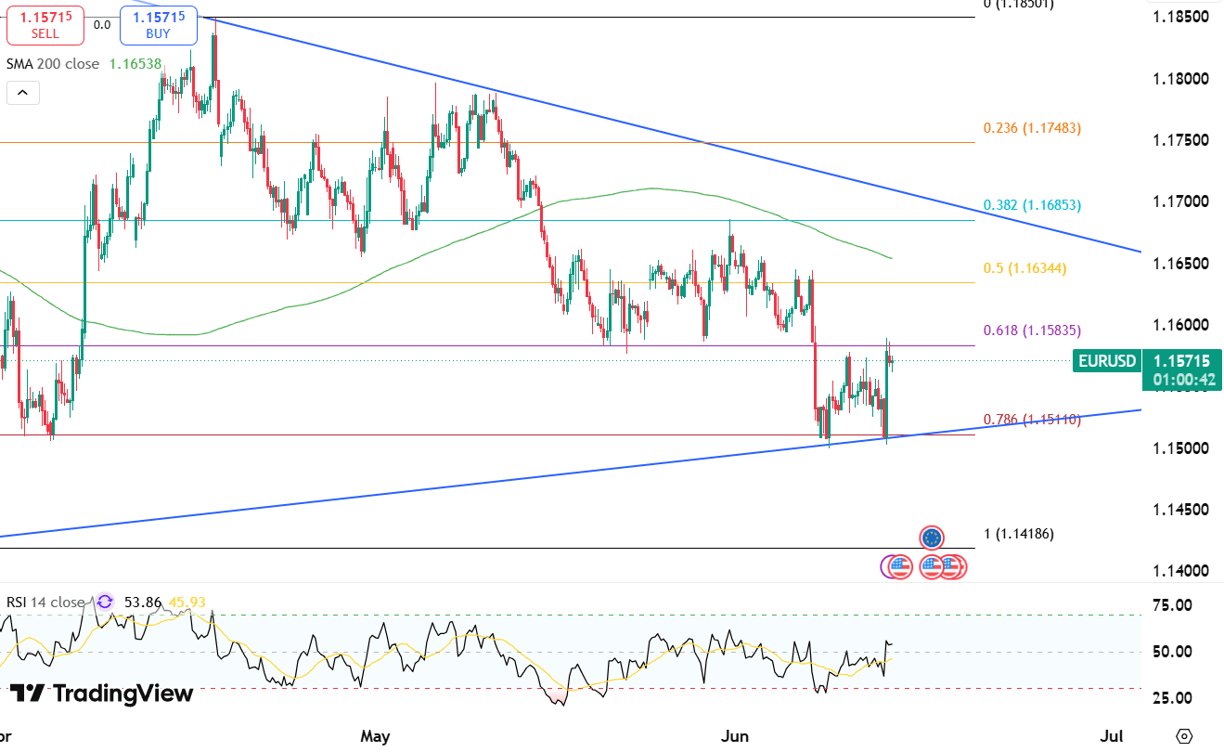

The euro spiked before retracing after the European Central Bank delivered an expected 25 basis point rate increase, hitting its lowest level since early April before stabilizing. Citing elevated energy costs and Iran-related geopolitical risks, policymakers raised inflation projections while modestly lowering growth outlooks. Also, the U.S. dollar retained firm backing, sustained by ongoing Middle East instability and persistent safe-haven capital flows.

For EUR/USD, the initial resistance is seen at 1.1600, while the closest support is positioned at 1.1540.

| R1: 1.1600 | S1: 1.1540 |

| R2: 1.1635 | S2: 1.1500 |

| R3: 1.1685 | S3: 1.1470 |

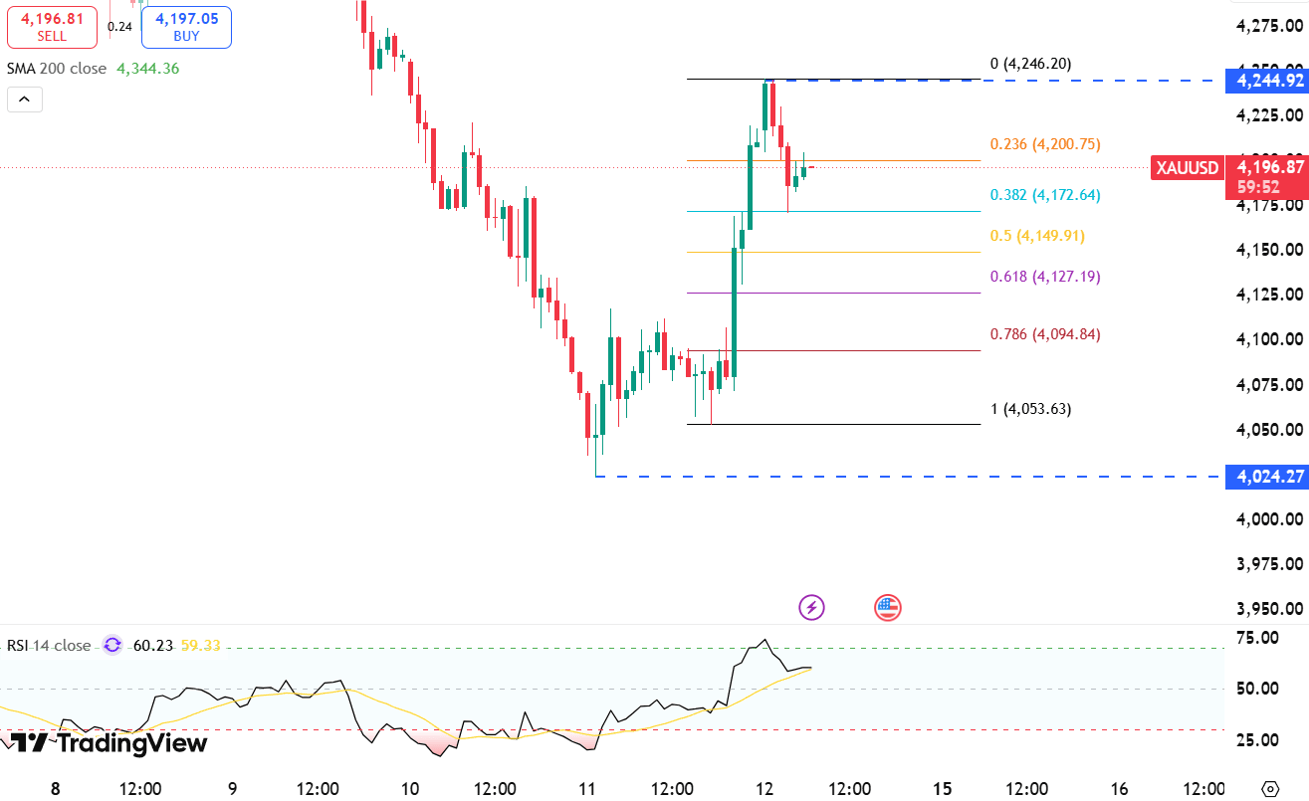

Gold stabilized near $4,200 on Friday following a 3% surge in the previous session, as easing geopolitical anxieties were driven by optimism surrounding a potential U.S.–Iran peace accord. President Trump indicated an agreement could be imminent, alongside reports suggesting Iranian willingness to comply. Recent ECB rate hikes and strong U.S. inflation figures continue to reinforce expectations that the Federal Reserve will maintain a restrictive monetary policy stance.

First resistance is seen at $4220, with initial support near $4150.

| R1: 4220 | S1: 4150 |

| R2: 4300 | S2: 4060 |

| R3: 4370 | S3: 3950 |

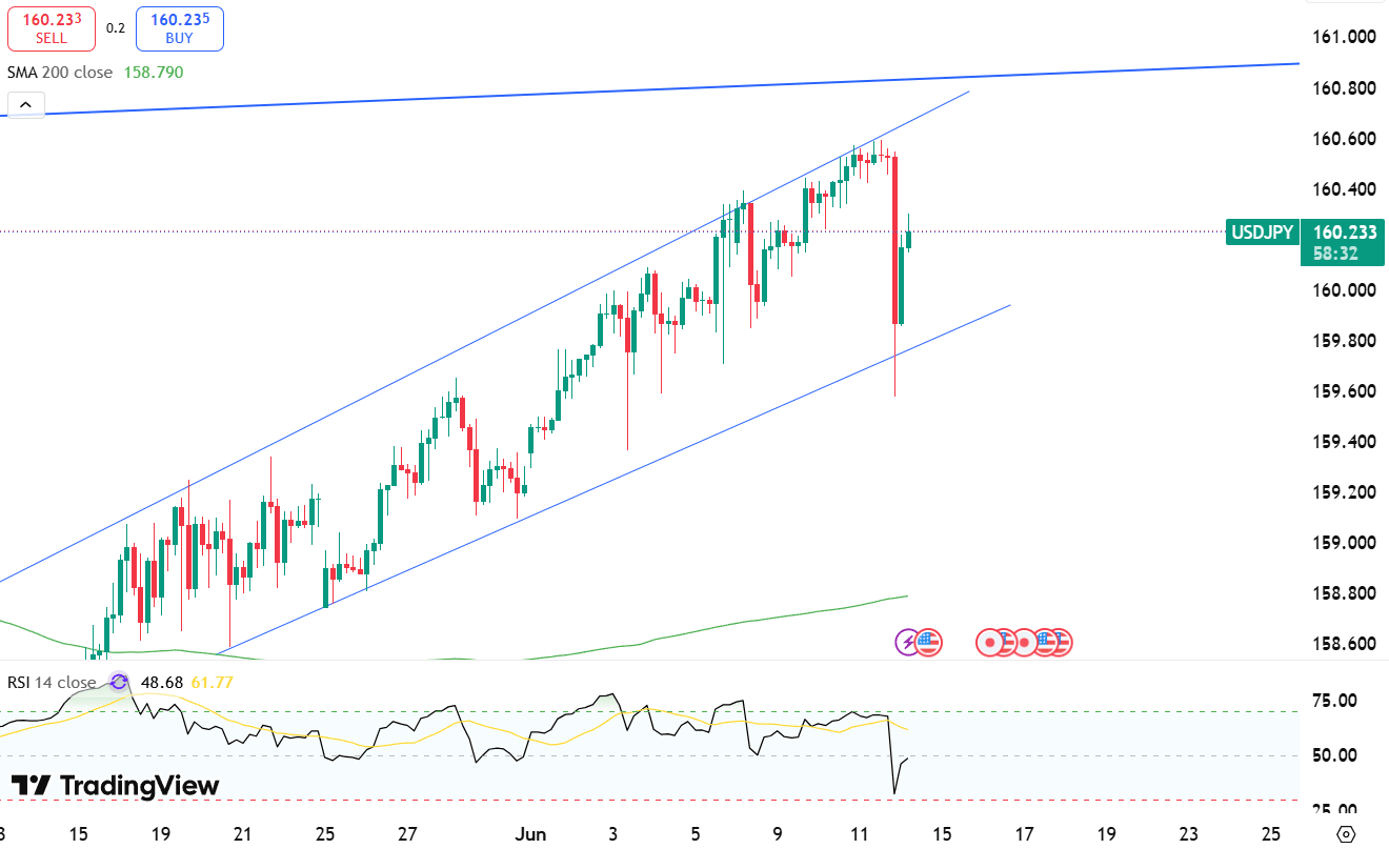

The Japanese yen softened toward 160.2 per dollar on Friday, paring earlier gains as investors positioned ahead of next week’s Bank of Japan policy decision. The BOJ is widely anticipated to lift interest rates by 25 basis points to 1%, marking its first hike since December and its highest policy level since 1995. However, Governor Kazuo Ueda will miss the proceedings due to hospitalization. While the yen previously found support from broad dollar weakness on hopes of a U.S.–Iran accord, Japan remains highly exposed to Middle East frictions due to its heavy reliance on imported energy.

Initial resistance stands at 160.90, while the first support is located at 159.40.

| R1: 160.90 | S1: 159.40 |

| R2: 161.50 | S2: 158.30 |

| R3: 162.40 | S3: 157.50 |

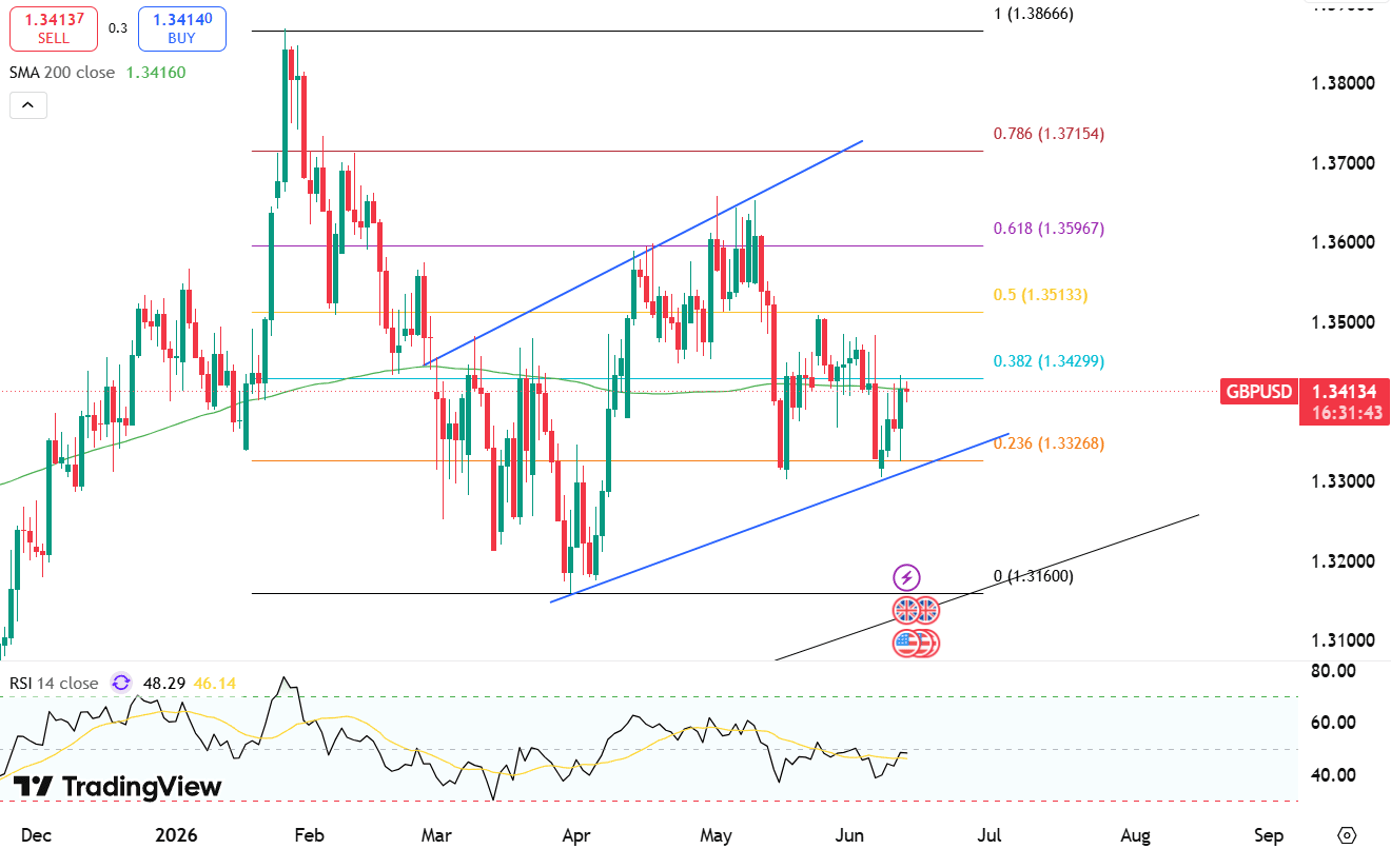

The British pound consolidated just under $1.34 as intensifying Middle East hostilities and expectations of further Bank of England tightening shaped market sentiment. Fresh U.S.–Iran military strikes drove geopolitical risks higher, while surging energy costs aggravated inflation anxieties. Investors now fully price in at least one BoE interest rate hike by September, despite internal policymaker debate regarding whether current monetary settings are already sufficiently restrictive.

From a technical view, resistance stands near 1.3410, with support around 1.3320.

| R1: 1.3410 | S1: 1.3320 |

| R2: 1.3460 | S2: 1.3240 |

| R3: 1.3530 | S3: 1.3200 |

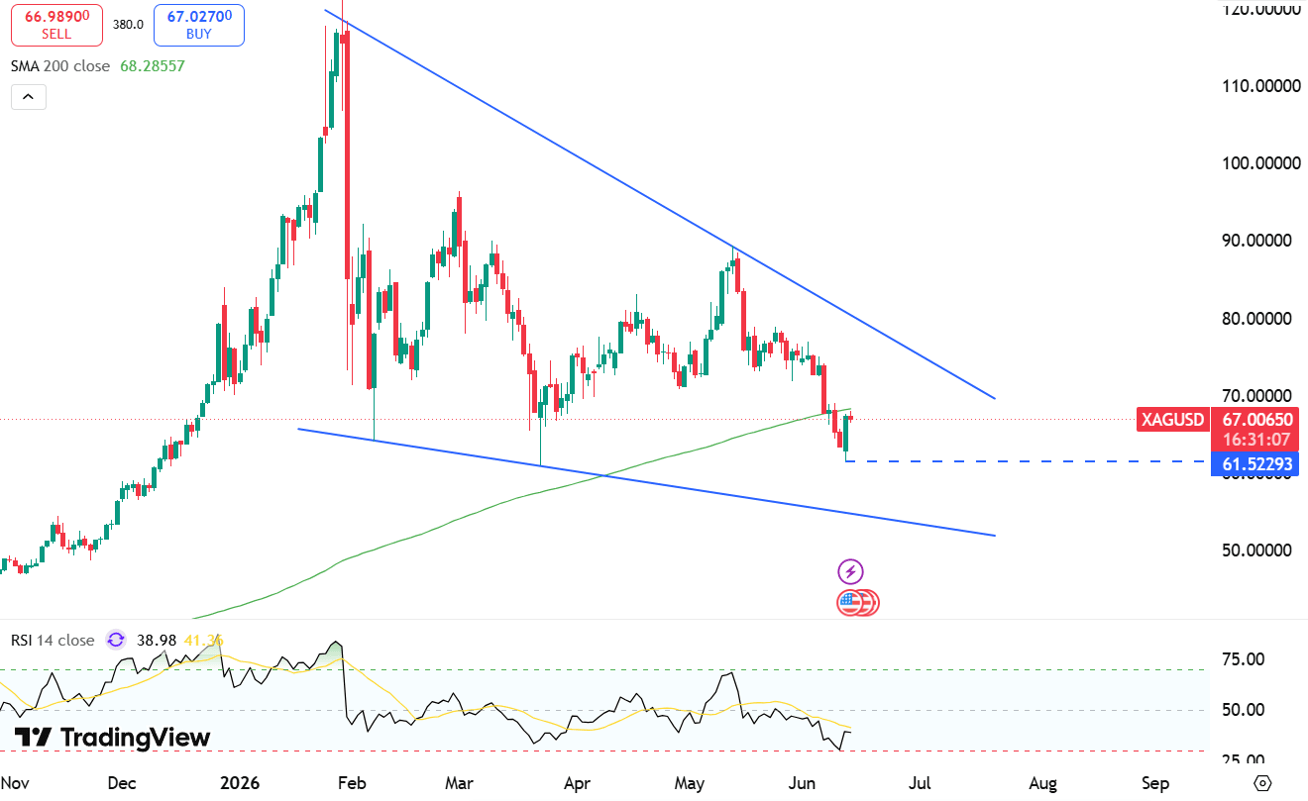

Silver stabilized near $67 after a prior 6% rebound, buoyed by weakening inflation fears and progress toward a U.S.–Iran peace agreement signaled by President Trump. Meanwhile, recent ECB interest rate hikes and hot U.S. producer price data reinforced expectations that the Federal Reserve will maintain a tightening cycle.

From a technical view, resistance stands near $68.50, while support is located around $65.00.

| R1: 68.50 | S1: 65.00 |

| R2: 70.00 | S2: 63.20 |

| R3: 72.00 | S3: 61.50 |

") Ceasefire Pause Eases Oil and Inflation Fears (27 – 31 July)

Ceasefire Pause Eases Oil and Inflation Fears (27 – 31 July)Global markets began the week on a more positive footing after a pause in US and Iranian military operations reduced immediate concerns over energy supplies and inflation. The United States quietly suspended its nearly two-week strike campaign against Iran late Friday, while Tehran halted retaliatory operations and entered discussions with Oman regarding the Strait of Hormuz. The developments pushed oil prices sharply lower, supporting precious metals and government bonds after weeks of pressure from rising energy costs.

Detail Fed in Focus Amid Easing Tensions (07.27.2026)Global markets began the week on a firmer footing as a pause in U.S.–Iran hostilities eased concerns over energy supplies and inflation.

Higher oil prices lifted inflation expectations, pushing the probability of a September Fed rate hike to 78%.

DetailThen Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!