Fresh economic data from the Eurozone is fueling expectations that the European Central Bank (ECB) may have room to deliver another rate cut before year-end.

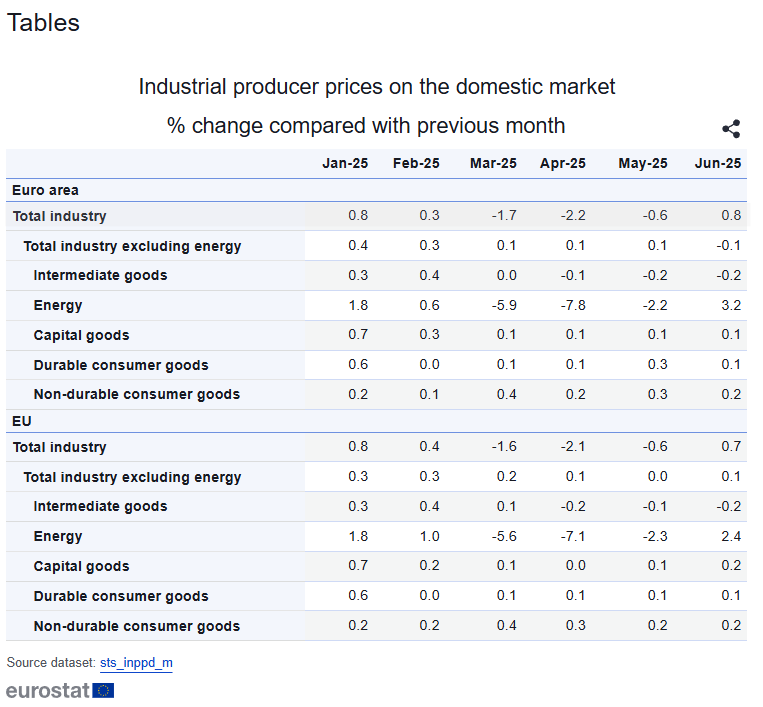

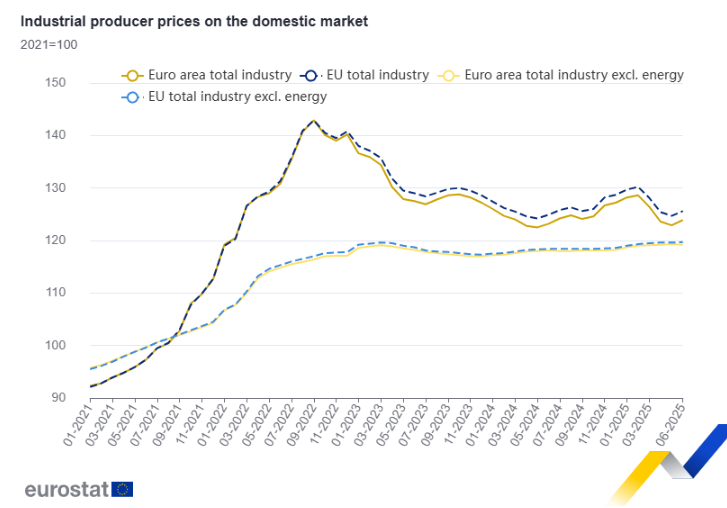

The Producer Price Index (PPI) for June rose by 0.8% month-on-month and 0.6% year-on-year. While the monthly increase came in slightly below market forecasts, the annual figure surprised to the upside, driven by a sharp 3.2% surge in energy prices. This rise helped offset declines in intermediate goods, signaling that disinflation in manufacturing inputs is still playing out.

The latest Purchasing Managers’ Index (PMI) readings painted a mixed picture across the Eurozone. The Services PMI finalized at 51.0 in July, up from 50.5 in June, pointing to a modest pickup in service sector activity. The Composite PMI also edged up to 50.9, suggesting a slight overall expansion.

Country-level breakdowns showed Spain leading the bloc with a Services PMI of 54.7, its highest level in five months, followed by Germany and Italy. However, France slipped to a three-month low of 48.6, highlighting uneven momentum across the region.

One encouraging sign was the continued easing of input cost inflation in the services sector, which cooled to a nine-month low, reflecting reduced wage pressures. This trend of softening cost inflation is seen as giving the ECB more flexibility for further policy easing in the months ahead.

Meanwhile, in the UK, PMI figures displayed a more cautious outlook. The Services PMI for July was revised down to 51.8 from an initial estimate of 52.8, while the Composite PMI dipped to 51.5. Although these figures suggest a slowing pace of expansion, business sentiment proved more resilient.

Easing fears over potential U.S. tariffs and rising expectations of a Bank of England rate cut helped underpin business confidence. Despite softer headline numbers, many firms remained optimistic about future demand and investment opportunities, suggesting that the underlying mood is firmer than the data alone might suggest.

Higher oil prices lifted inflation expectations, pushing the probability of a September Fed rate hike to 78%.

Detail Conflict Fuels Inflation Fears (07.23.2026)Middle East tensions lifted Brent crude above $95, a six-week high, on fears of supply disruptions.

Detail The Yen Adds to BOJ Pressure (07.22.2026)Japan's 10-year yield rose to 2.74%, a one-week high, as higher oil prices and a 40-year low in the yen reinforced expectations of further BOJ tightening.

DetailThen Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!