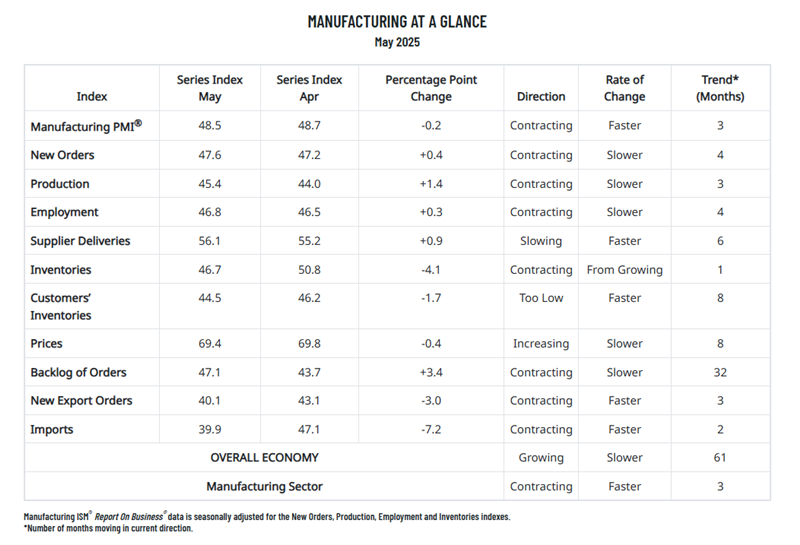

The Institute for Supply Management® (ISM®) reported that the Manufacturing PMI® for May 2025 declined slightly to 48.5%, compared to 48.7% in April.

This marks another month of contraction in U.S. manufacturing, although the broader economy continued to expand for the 61st consecutive month. A reading above 42.3% typically signals overall economic growth, suggesting that the current decline remains confined largely to the manufacturing sector.

Susan Spence noted that while demand remains weak, there are early signs of stabilization, especially in new orders and backlogs. However, export demand declined further, and customer inventories are still too low, which could encourage higher production in the near term.

Production continues to contract, but the decline has moderated compared to April. Employment remains soft, with layoffs persisting as companies avoid natural attrition. Inputs including inventories and imports softened further amid trade disruptions and post-tariff adjustments. Prices remain elevated, although the pace of increases has moderated.

Industries Reporting Expansion (7 total):

Industries Reporting Contraction (7 total):

The May 2025 ISM report reflects a broad but mixed picture for the U.S. manufacturing sector. While contraction persists, the pace has moderated in some areas, hinting that the worst of the downturn may be easing. Persistent challenges remain, particularly on the input side and in global trade, but modest improvements in orders and sector breadth offer some cautious optimism.

Source: ISM

Trump Signals Extended Military Campaign

Trump Signals Extended Military CampaignGeopolitical tensions in the Middle East have intensified following recent remarks from Donald Trump suggesting that the ongoing military campaign against Iran may last longer than anticipated. While Trump stated that early operational objectives were achieved ahead of schedule, he acknowledged that broader strategic goals could require additional time and sustained military pressure.

Detail US DST Change March 8 2026

US DST Change March 8 2026Daylight Saving Time will change in the United States on Sunday, March 8, 2026. The trading schedule for various financial instruments will be adjusted to align with U.S. exchange hours.

Detail Dollar Leads Risk-Off (03.06.2026)Global markets remained under pressure as escalating Middle East tensions and rising energy prices strengthened the US dollar and unsettled major currencies.

Then Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!