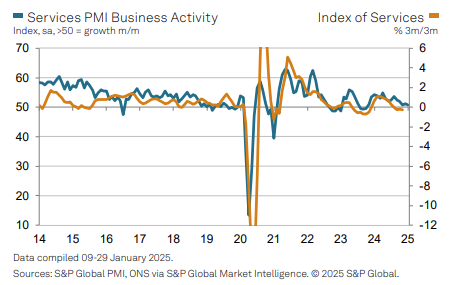

The S&P Global UK Services PMI® data for January signaled continued expansion in business activity, though at a marginal pace.

The seasonally adjusted Business Activity Index fell to 50.8, down from 51.1 in December, marking the joint-lowest level in 15 months. The latest reading remains well below pre-pandemic levels, highlighting sluggish growth in the services sector.

Service providers cited several factors weighing on business activity, including:

Total new work orders declined in January, ending a 14-month streak of continuous growth. Some businesses attributed the drop to higher interest rates and global economic uncertainty, while others pointed to reduced confidence following the Autumn Budget. However, technology services remained a bright spot, with strong demand supporting limited pockets of business expansion.

Staffing levels declined for the fourth straight month, with the pace of job losses accelerating to its highest level since January 2021. Rising payroll costs and shrinking margins led to hiring freezes and restructuring efforts.

Input price pressures surged, with cost inflation reaching a nine-month high due to increased salary payments and supplier price hikes.

Prices charged by service sector firms rose at the fastest rate in 13 months, although some businesses opted for price discounting to stimulate demand.

Export sales fell for the second consecutive month, though the decline was less severe than in December. While demand from the U.S. remained stable, spending in Europe weakened.

Backlogs of work declined significantly, reflecting excess capacity after months of subdued demand. The reduction in unfinished work was the steepest since August 2023.

Business confidence fell to its lowest level since December 2022, as firms expressed concerns over squeezed margins, weak demand, and disappointing UK economic growth prospects.

The January data paints a mixed picture for the UK services sector, with marginal growth overshadowed by mounting cost pressures and rising job losses. With inflationary pressures intensifying and business confidence weakening, the sector faces a challenging start to 2025.

Source: S&P Global

") Strong USD and Surging Oil Amid Tensions (16–20 March)

Strong USD and Surging Oil Amid Tensions (16–20 March)Global markets faced significant upward pressure on yields and energy prices this week as the conflict in the Middle East entered its third week. The US Dollar Index surged above 100.3, its highest since May 2025, fueled by safe-haven flows and Defense Secretary Pete Hegseth's announcement of the largest planned strike wave against Iran to date. Brent crude breached the $105 threshold following strikes on Kharg Island and warnings that 90% of Iran’s export facilities could be targeted.

Detail Markets Brace for Central Bank Week (03.16.2026)Global markets remain dominated by geopolitical tensions and energy risks as the conflict in the Middle East continues to shape investor sentiment.

Global markets remained dominated by dollar strength as geopolitical tensions and rising energy prices reshaped monetary expectations.

Then Join Our Telegram Channel and Subscribe Our Trading Signals Newsletter for Free!

Join Us On Telegram!