Global markets were mixed following the Fed's 25 basis point rate cut, shifting focus to major central bank decisions (ECB, BoE, BoJ) and US data. US 10-year Treasury yields rose near 4.2% as some Fed officials expressed caution regarding the pace of cuts, despite dovish counterarguments.

US stocks stabilized after a volatile week driven by a rotation away from expensive tech, with the Dow hitting a record. The dollar held steady as investors parsed mixed Fed signals and awaited delayed US reports.

| Time | Cur. | Event | Forecast | Previous |

| EUR | Average Hourly Earnings (MoM) (Nov) | 0.2% | ||

| USD | Core Retail Sales (MoM) (Oct) | 0.3% | 0.3% | |

| USD | Nonfarm Payrolls (Nov) | 119K | ||

| USD | Retail Sales (MoM) (Oct) | 0.2% | 0.2% | |

| USD | Unemployment Rate (Nov) | 4.4% | 4.4% | |

| USD | S&P Global Manufacturing PMI (Dec) | 52.2 | ||

| USD | S&P Global Services PMI (Dec) | 54.1 |

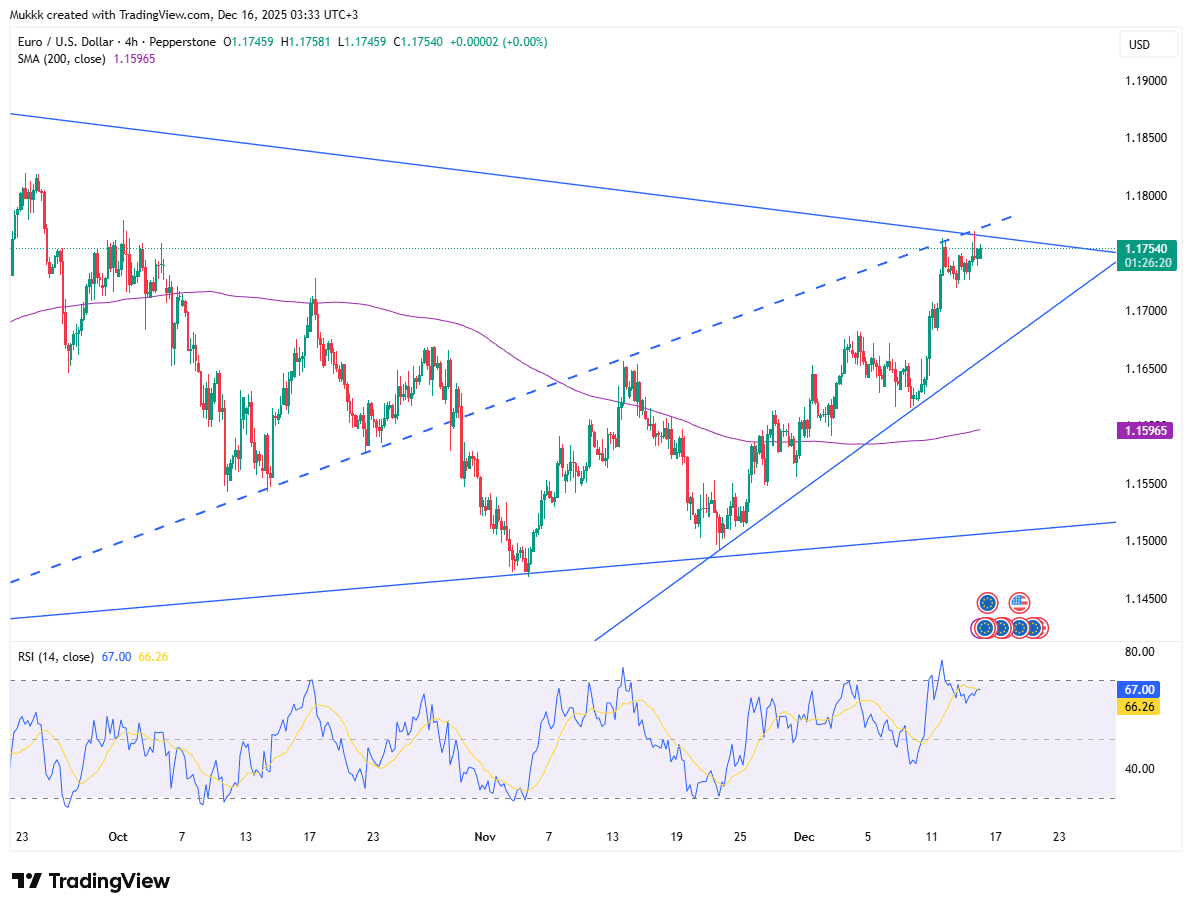

EUR/USD is holding steady near 1.1750 at the time of writing, with investors waiting for upcoming German and Eurozone PMI releases. From a technical perspective, the 20-day Exponential Moving Average, now at 1.1658, continues to trend higher and sits below spot levels. This setup supports a constructive short-term outlook and serves as the first support zone for the pair.

Technically, 1.1710 is the key support, while resistance is seen at 1.1810.

| R1: 1.1810 | S1: 1.1710 |

| R2: 1.1860 | S2: 1.1600 |

| R3: 1.1910 | S3: 1.1510 |

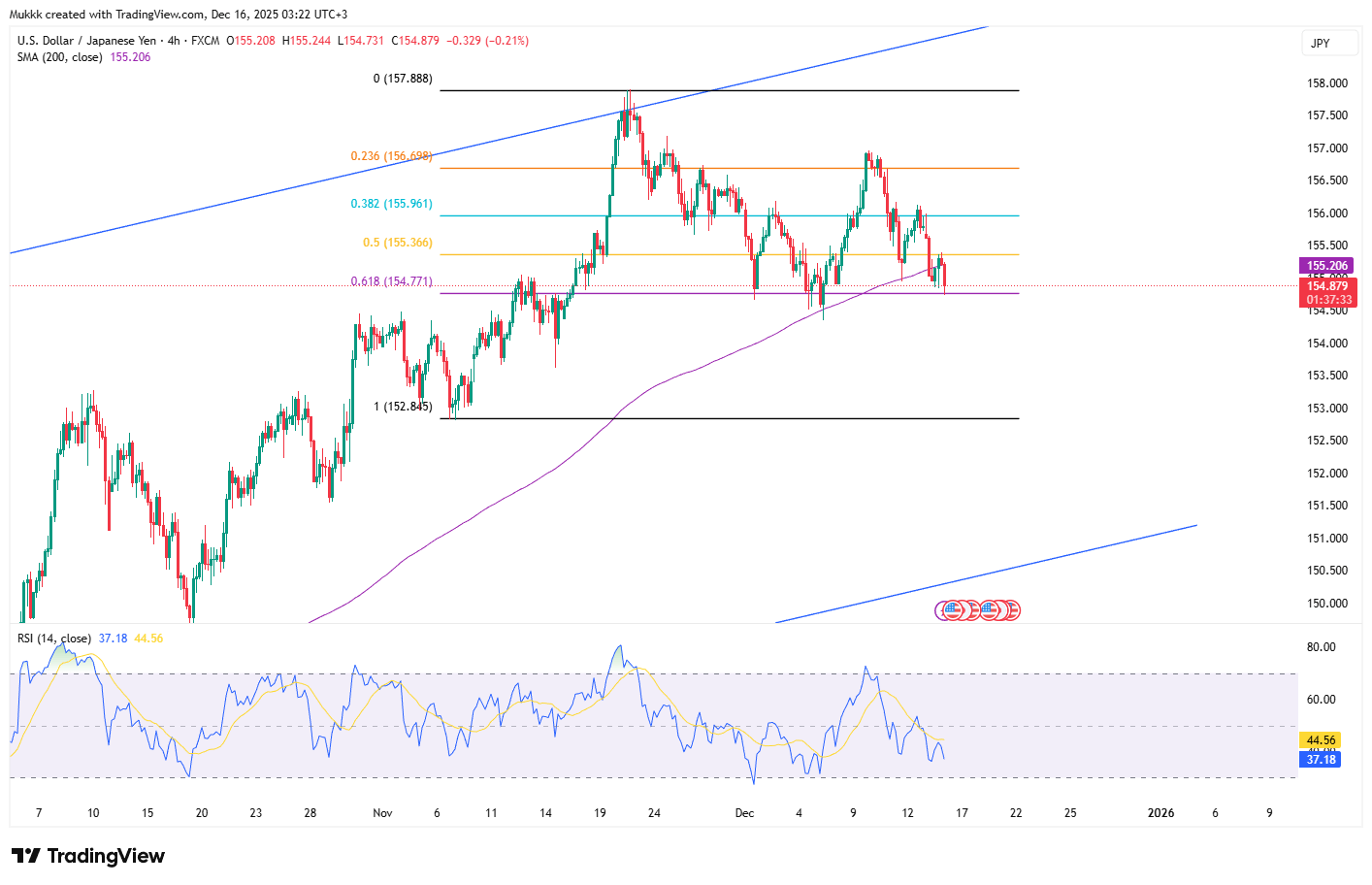

The Japanese yen rose above 155 per dollar on Tuesday, reaching closer to a one-month high as market participants adjusted positions ahead of the Bank of Japan's policy meeting this week. The central bank is broadly expected to implement a 25-basis-point increase, pushing its main policy rate to 0.75%. Investors will focus on Governor Kazuo Ueda’s post-meeting comments for indications about the policy direction for the coming year, with some experts predicting the rate could potentially reach 1% by July.

Technically, resistance stands near 155.70, while support is firm at 154.30.

| R1: 155.70 | S1: 154.30 |

| R2: 156.50 | S2: 153.60 |

| R3: 157.00 | S3: 152.80 |

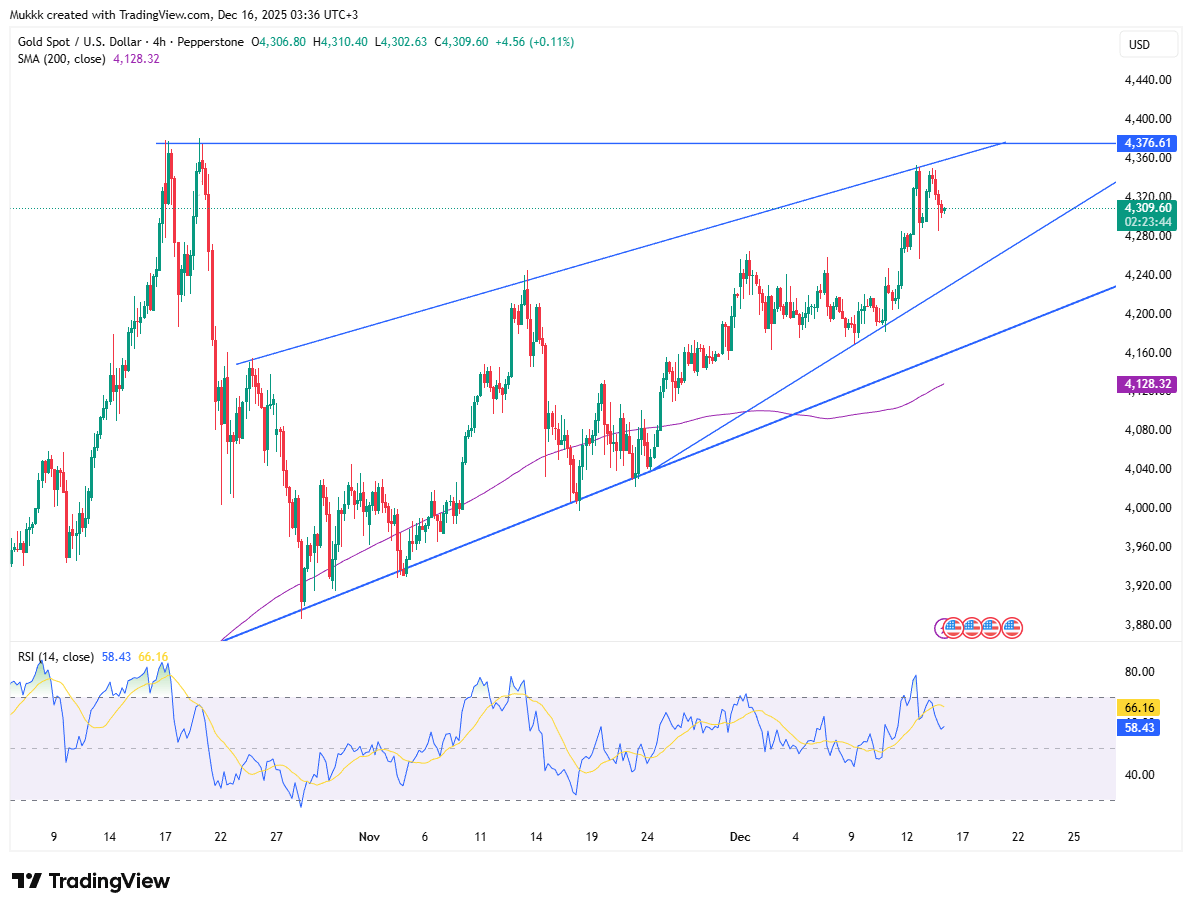

Gold (XAU/USD) dipped below $4,300 in early European trading, driven down by profit-taking and lower short-term futures activity. Reduced safe-haven demand, following optimism surrounding Ukraine peace talks, further pressured prices. However, losses may be capped by the Fed’s third rate cut this year and expected easing in 2026. Attention is now focused on delayed US data, including NFP, Retail Sales, and PMI, which could significantly influence rate-cut projections and subsequent gold movements.

Gold sees support near $4270, while resistance is around $4380.

| R1: 4380 | S1: 4270 |

| R2: 4450 | S2: 4230 |

| R3: 4500 | S3: 4195 |

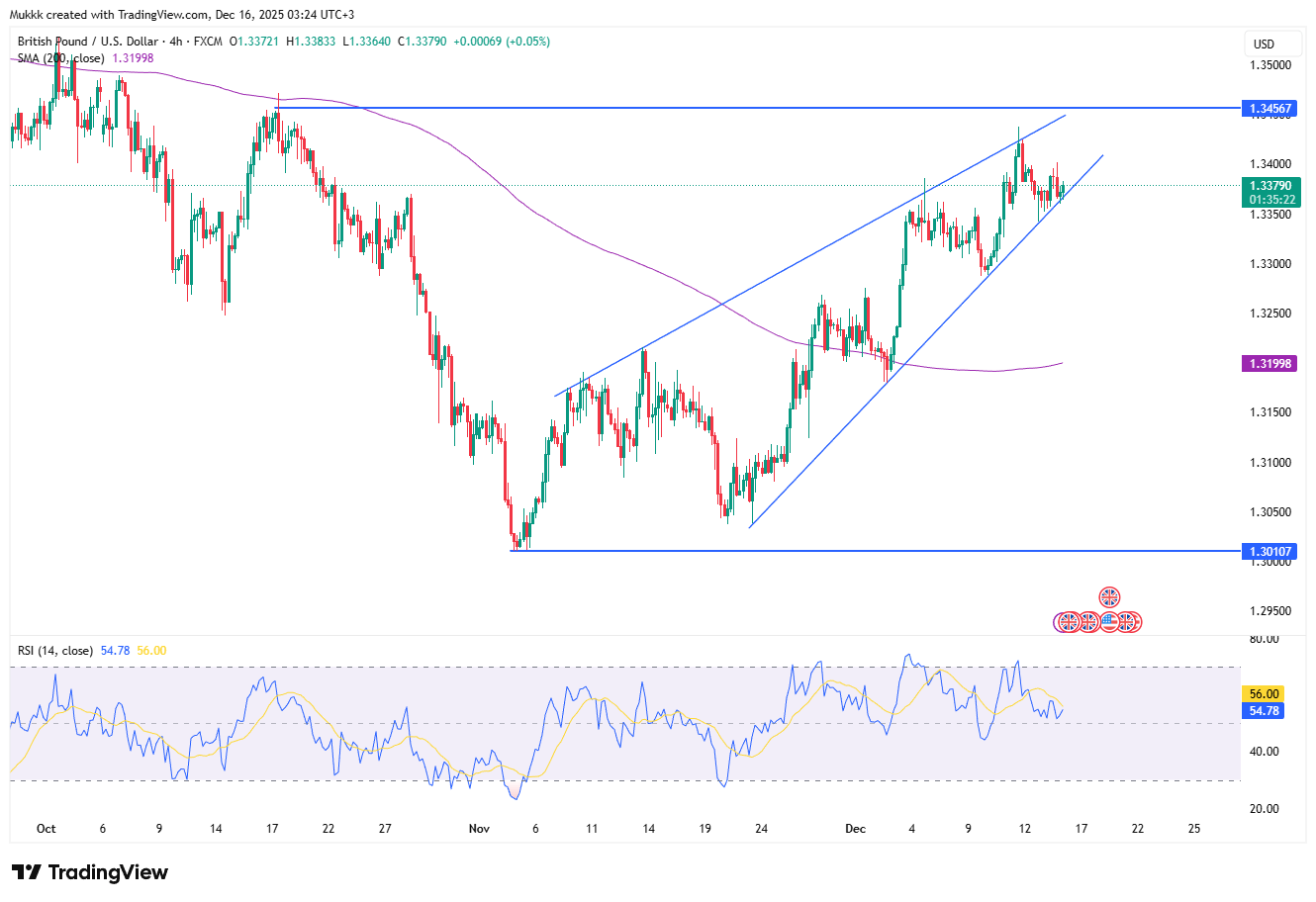

The GBP/USD pair is trading within a narrow range near 1.3370 in Asian trading, as markets anticipate a heavy week of central bank decisions and crucial data releases. This week features UK jobs, UK inflation, the BoE policy meeting, and US CPI. Sterling is currently held back by cautious risk sentiment and expectations of a BoE rate cut, while the USD's upside is limited by predicted Fed rate cuts. Crucially, the pair continues to hold above the key 200-day Simple Moving Average (SMA) near 1.3350, which provides immediate technical support.

From a technical view, support stands near 1.3320, with resistance around 1.3430.

| R1: 1.3430 | S1: 1.3320 |

| R2: 1.3500 | S2: 1.3250 |

| R3: 1.3560 | S3: 1.3170 |

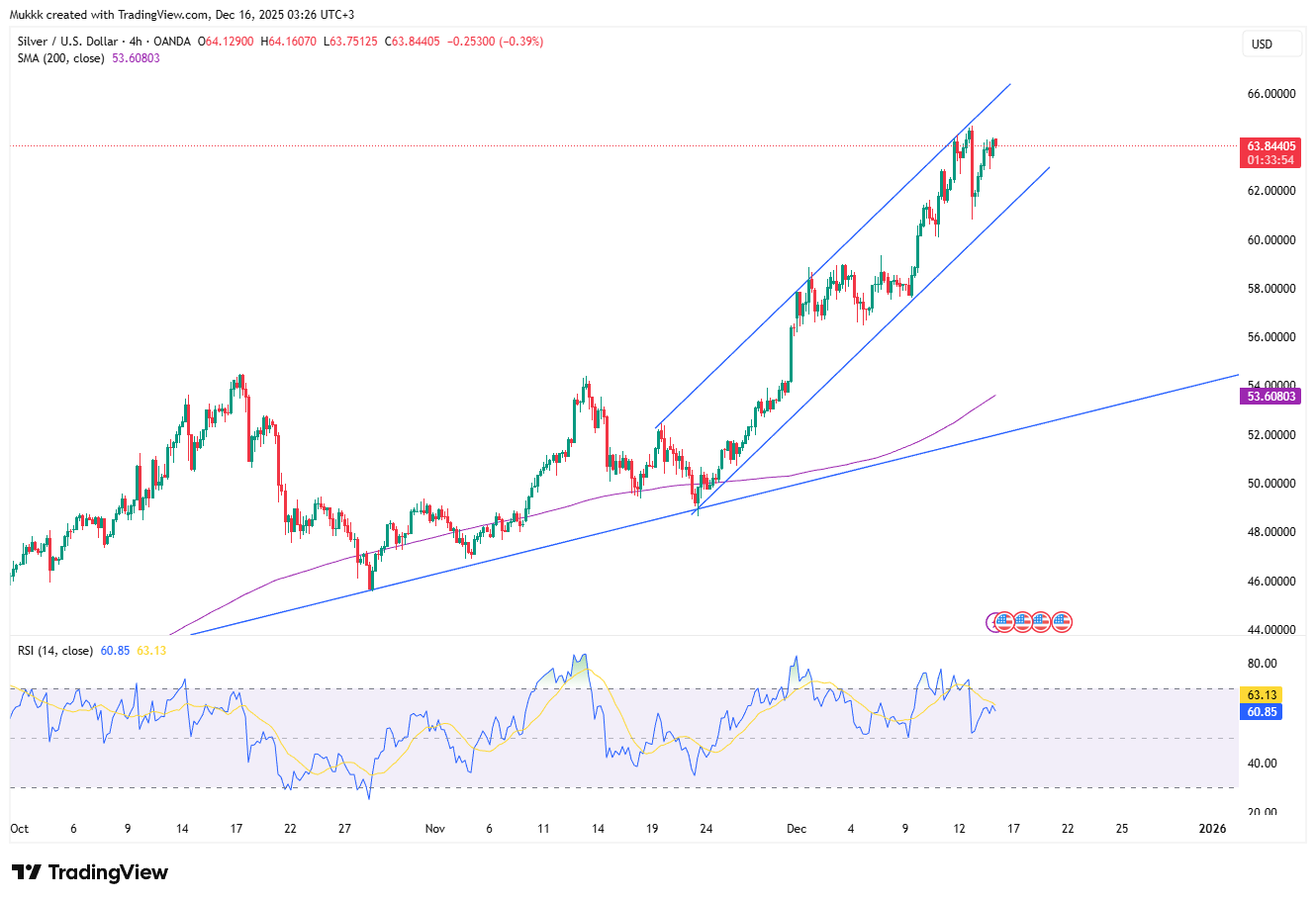

Silver dipped below the $63 per ounce mark on Tuesday, pulling back from record highs as investors secured profits following an extraordinary rally that has pushed prices up by approximately 120% this year. Analysts cautioned that silver is now overvalued compared to gold, citing potential risks from US tariff exemptions. The year-long powerful rally has been supported by tight inventories and strong demand from key industries, especially solar, electric vehicles (EVs), and data centers.

From a technical view, resistance stands near $64.50, while support is located around $62.00.

| R1: 64.50 | S1: 62.00 |

| R2: 65.70 | S2: 61.50 |

| R3: 66.50 | S3: 60.40 |

افزایش تورم منطقه یورو به ۲.۹ درصد

افزایش تورم منطقه یورو به ۲.۹ درصدتورم منطقه یورو در ماه ژوئیه اندکی افزایش یافت. رشد بهای انرژی همچنان فشارهای قیمتی را بالاتر از هدف بانک مرکزی اروپا نگه داشت. نرخ تورم سالانه از ۲.۸ درصد در ژوئن به ۲.۹ درصد رسید. این رقم مطابق انتظار بازار بود اما همچنان بالاتر از هدف ۲ درصدی بانک مرکزی اروپا قرار دارد.

جزئیات مکث در توکیو؛ اما انقباض ادامه دارد

مکث در توکیو؛ اما انقباض ادامه داردبانک مرکزی ژاپن در نشست ماه ژوئیه، نرخ بهره را بدون تغییر و در سطح ۱.۰ درصد حفظ کرد. این تصمیم پس از افزایش ۰.۲۵ واحد درصدی نرخ بهره در ماه ژوئن اتخاذ شد و مطابق انتظار بازار بود.

جزئیات") بانکهای مرکزی در کانون توجه بازارها (۱۴۰۵/۰۵/۰۹)

بانکهای مرکزی در کانون توجه بازارها (۱۴۰۵/۰۵/۰۹)بازارهای جهانی در حال ارزیابی تصمیمهای اخیر بانکهای مرکزی هستند. سرمایهگذاران پس از تثبیت نرخ بهره توسط فدرال رزرو، مواضع انقباضی بانک مرکزی انگلستان و بانک مرکزی ژاپن را نیز بررسی میکنند.

جزئیاتهمین حالا به کانال تلگرام زفارکس بپیوندید و سیگنالهای معاملاتی رایگان را دریافت کنید!

به کانال تلگرام ما بپیوندید!