The eurozone economy remained in a fragile state at the close of 2024, according to the latest HCOB PMI® survey.

The eurozone economy remained in a fragile state at the close of 2024, according to the latest HCOB PMI® survey. Economic activity contracted for the second consecutive month due to persistent declines in new business and employment, with inflationary pressures intensifying. Despite a slight improvement in business expectations, optimism for the next 12 months remained historically weak.

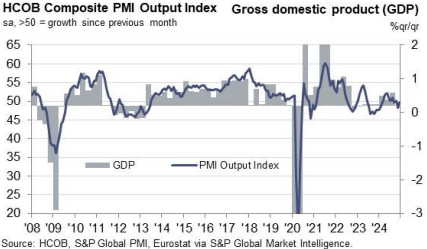

The seasonally adjusted HCOB Eurozone Composite PMI Output Index stood at 49.6 in December, up from November’s 48.3 but still below the neutral 50.0 mark. This indicates a continued decline in economic activity, albeit at a softer pace compared to the previous month.

Among the eurozone’s largest economies:

While firms reported a slight improvement in growth expectations compared to November’s 14-month low, optimism remained historically muted. The December data highlights ongoing economic fragility in the eurozone, driven by manufacturing struggles and subdued recovery in the services sector. Inflationary pressures and weak external demand continue to weigh on the region’s growth prospects.

Source: SP Global

استقر مؤشر الدولار بالقرب من 98.8 يوم الخميس، حيث أثارت أنباء غرق غواصة أمريكية لسفينة حربية إيرانية بالقرب من سريلانكا واليوم السادس من الحملة الأمريكية الإسرائيلية مخاوف من صراع طويل الأمد يؤدي إلى تضخم.

التفاصيل مخاطر الطاقة والحرب ترفع قيمة الدولار (03.04.2026)لا تزال الأسواق العالمية تحت سيطرة المخاطر الجيوسياسية، حيث أدى تصاعد الصراع بين الولايات المتحدة وإسرائيل وإيران إلى تحول قوي نحو الأصول الآمنة. وصل مؤشر الدولار إلى 99.3 يوم الأربعاء، مرتفعًا لليوم الثالث على التوالي، حيث أدت المخاوف من الصراع إلى تفاقم التضخم وتغيير توقعات خفض أسعار الفائدة من قبل بنك الاحتياطي الفيدرالي من يوليو إلى سبتمبر.

التفاصيل وضع تجنب المخاطر يهيمن على التجارة العالمية (03.03.2026)رفضت محكمة أمريكية تأجيل ترامب لرد الرسوم الجمركية، حيث حافظ الدولار (98.5) والعائد على سندات 10 سنوات (4.04٪) على مكاسبهما وسط تصاعد التوترات في الشرق الأوسط ومخاوف التضخم.

التفاصيلثم انضم إلى قناتنا على تيليجرام واشترك في النشرة الإخبارية لإشارات التداول مجانًا!

انضم إلينا على تيليجرام!